A Prince and a Powell

August 27, 2022

Waiting . . . waiting.

Waiting on Jackson Hole.

That was pretty much our week.

For the most part, we (i.e., the market) were all waiting for Jackson Hole, the Federal Reserve’s conference in that picturesque Wyoming setting.

No we’ve never been, but how could this place not be a hoot.

Like the Old West, Powell and his coterie come annually, like a cowboy pilgrimage of sorts, and this year he came guns a’blazing. Remember, before Jackson Hole the narrative had shifted. The Fed will raise rates aggressively and sharply . . . but for only a short period of time . . . then it will pivot gloriously, tapering/easing rates again as inflation subsides and the economy slows. So higher rates sure, but it’ll drop off soon and we’ll all be good. Since the market fancies itself as Wayne Gretzky, always “skating to where the puck will be,” it began pricing in those lower rates. In turn, growth stocks and meme stocks that only a month ago floated like lead balloons rediscovered their buoyancy and rose. Apparently all will be well, and we’re back to YOLO-ing.

In came Powell and his 10 minute speech. He was scheduled for 30 minutes, but he needed just 10.

“Today, my remarks will be shorter, my focus narrower, and my message more direct.”

It was one of the quickest draws you never saw coming. POW POW POWELL was all you heard. (Oh no you didn’t! Oh yes we did . . . we onomatopoeia’d his name).

“Restoring price stability will take some time and requires using our tools forcefully to bring demand and supply into better balance. Reducing inflation is likely to require a sustained period of below-trend growth. Moreover, there will very likely be some softening of labor market conditions. While higher interest rates, slower growth, and softer labor market conditions will bring down inflation, they will also bring some pain to households and businesses. These are the unfortunate costs of reducing inflation. But a failure to restore price stability would mean far greater pain.” (emphasis added)

When the smoke cleared, the balloons deflated.

Well maybe not deflated . . . more like slaughtered because remember the market narrative? The Fed rides with us . . . We CHARGE!

What was previously in a firm uptrend was in full retreat by Friday. The directness and forcefulness of the Fed Chair’s speech caught many market participants by surprise, as money managers had begun positioning for a Fed pivot (a softening of their hawkish stance). As you can see above, the Fed remains undeterred. The continuing strength in the labor market will allow them to sacrifice that mandate (maximum employment) for their second mandate (price stability).

Given the persistent inflation, interest rates must go up, and they must go up for period of time. Unlike the tepid Fed of the 1970s, whereby they raised and then lowered rates as the economy tumbled (multiple times), Chair Powell has a different plan.

“Restoring price stability will likely require maintaining a restrictive policy stance for some time. The historical record cautions strongly against prematurely loosening policy.”

Because if the end goal is this . . .

“We are moving our policy stance purposefully to a level that will be sufficiently restrictive to return inflation to 2 percent.”

. . . we are a long way there when inflation is reading 8.5% now.

“If the public expects that inflation will remain low and stable over time, then, absent major shocks, it likely will. Unfortunately, the same is true of expectations of high and volatile inflation. During the 1970s, as inflation climbed, the anticipation of high inflation became entrenched in the economic decisionmaking of households and businesses. The more inflation rose, the more people came to expect it to remain high, and they built that belief into wage and pricing decisions. As former Chairman Paul Volcker put it at the height of the Great Inflation in 1979, "Inflation feeds in part on itself, so part of the job of returning to a more stable and more productive economy must be to break the grip of inflationary expectations.”

So raise rates, lower demand now, lest inflation festers and permeates people’s thoughts, driving further inflation. As noted before, interest rates are gravity and the higher the gravity, the lower the prices. (Unless you’re Buffett of course who can buy “moaty” gravity defying companies that are able to pass along these costs because of some inherent competitive advantage). Other mere mortals need not apply.

So high $30s to $50s for ARKK, and quickly back to low $40s. Do we think the riskiest of the risk assets are in trouble? Do we think the market trends lower from here? Yes and yes.

Yes . . . because we’ve written before, we’re all waiting to cross. All these cross-currents, all these narratives, they will take turns influencing and roiling the market, but the underlying issues remain, inflation will be stubbornly persistent because we are structurally short commodities, we are on-shoring/near-shoring production post-COVID, and labor/wages are increasing due to retirements and low immigration. Those fundamental issues will continue to persist, as will higher inflation. We may not eclipse the 9.1% we recently saw, or even the 8.5% CPI print we saw last month, but could 4-5% be in the cards in the coming years? Yes, and whatever it will be, we’re quite confident that it’ll be above the 2% inflation that we’ve been blessed with this past decade.

Globalization, loose monetary policy, offshoring, and resource abundance, those factors are all reversing. Prices for stuff will keep rising and people have already begun paying attention.

“. . . inflation has just about everyone’s attention right now, which highlights a particular risk today. The longer the current bout of high inflation continues, the greater the chance that expectations of higher inflation will become entrenched.”

Yup.

“We are taking forceful and rapid steps to moderate demand so that it comes into better alignment with supply, and to keep inflation expectations anchored. We will keep at it until we are confident the job is done.”

Well you’ve definitely got the market’s attention now. So witness the quick draw, pay rapt attention to the assuredness of the Fed’s comments today. There be varmints in them Jackson Hole hills and the Fed reckons its gonna go get them. Inflation varmints to be sure, and the Fed’s gonna round up a posse to lower demand and quell rising prices.

We think they’ll be hard pressed, but like the townspeople of old, when the gunslingers come to play, best duck and cover.

The Artist Currently Known as Prince AbS

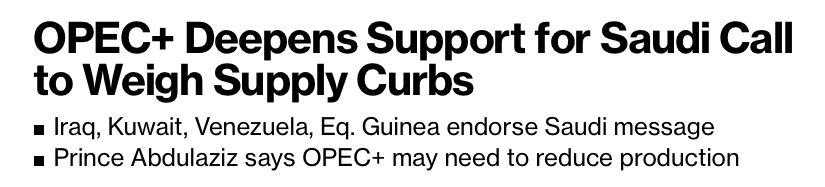

The other notable quotable this week were comments made by Prince Abdulaziz bin Salman (“AbS”), Saudi Arabia’s energy minister and de facto leader of OPEC+. In a written Bloomberg interview, on Monday, the energy minister wrote the following:

In addition, he wrote:

The comments immediately prompted a market response as oil began to climb. In the past few weeks we’ve been canvassing oil traders with the question “if the SPR releases (i.e., 1M bpd) will slow after October, why aren’t oil prices after October rising?” To a man (and yes they are all men) cited Iran’s return to the market, macro-uncertainty and volatility/higher margin requirements. No wonder open interest has fallen to levels we haven’t seen in years (Goldman Sachs).

If fewer people are trading it, then fewer people are conducting price discovery. The likelihood of oil being mispriced in this increasingly illiquid market rises, so when the physical side actually runs short (or shorter), prices can snap-upwards violently. This isn’t a high-class problem for OPEC+, it’s actually a problem. When energy prices rise too quickly demand destruction can set-in, taking the global economy with it. Persistently high oil prices will also feed into inflationary pressures, sapping consumer spending and slowing the economy. It’s all bad, so hence, the interview. Shortly thereafter, as if by some magical osmosis, many other OPEC+ members chimed in with their support.

Surely a coincidence right? Don’t call me Shirley.

Oil prices reacted and Brent advanced nearly 5% for the week to $100/barrel. WTI similarly clawed its way higher as OPEC+ effectively set a floor (i.e., a “put”).

Undoubtedly, some of these comments were to mitigate the other uncertainty (i.e., the recent market chatter that Iran could rekindle it’s relationship with the world and agree with the West on rejoining the JCPOA). We’ve long believed that it would be difficult for the two sides to agree, but even we have to admit, it’s recently become more likely. The world needs those Iranian barrels and are increasingly desperate for an agreement. The fact that the agreement will be nearly toothless at this stage? Matters not.

Iran’s return means 1-1.5M bpd of extra exports and an initial ~50M barrels in floating storage being released to the world, all just in time to supplant the SPR releases when they stop. So in the end it mitigates the gaping supply whole, and prevents prices from spiking uncontrollably (-1M bpd from SPR offset by +1.0 to 1.5M bpd from Iran = all’s well). So yes, we think the West wants it, and we think they’ll push hard enough to get it at this stage.

So long as it doesn’t crater oil prices though . . . says OPEC+. So we’ll set a floor and accommodate Iran’s return to the market. Will they really? Doubtful. They’ll produce what they’ve always produced. We don’t think they’ll actually cut “real” production. Sure they may play with their “quotas,” but they’re already underproducing those self-imposed quotas to begin with by a large margin.

Remember, OPEC+’s quotas were originally put in place at the start of COVID, when oil prices cratered. To give the appearance of a larger cut than reality, OPEC+ agreed to cut from a “reference level”, which were largely fantastical (42M bpd of production vs. what they were really then producing (~39.5M bpd in Q1 2020)). So as they’re getting back to “full production” they’re marching towards 42M bpd, and now we’re saying they’re “underproducing” their quotas . . . well truth be told they were never really producing at the high level anyways. In the end, if OPEC+ wants to accommodate Iran, they’ll likely just cut production from that fictional reference level, and not actually produce any less, which is fine since again Iran replaces the SPR draws.

Still, it’s all about perception right? Set a floor on oil prices and declare to the market . . . thou shalt not pass.

So whether it’s inflation for the Fed or low oil prices for OPEC+, two guys have changed the market’s narratives this week, and that will ripple for a bit. A Powell and a Prince, or a Prince and a Powell, whatever . . . just pay attention though because they sure have a tale to tell.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

Will energy get killed with rate hikes? Maybe just going short is safer