All You Can Eat . . . Inflationary Assets

August 31, 2020

As the legendary Stanley Druckenmiller says

“Earnings don’t move the overall market; it’s the Federal Reserve Board… focus on the central banks and focus on the movement of liquidity… most people in the market are looking for earnings and conventional measures. It’s liquidity that moves markets.”

Akin to the oil market where understanding what Saudi Arabia, that central bank of oil, ultimately wants, understanding the US Federal Reserve’s (“Fed”) policies has to be a foundational part of any investment thesis. The Fed has the ability to drive shifts in asset trends, and as a result, investors who are properly positioned can ride the impending liquidity wave for years to come.

Sure you say, we’ve heard this song before. As the Fed engaged in quantitative easing (“QE”) after the 2008/2009 Great Financial Crisis, many have argued that these monetary actions will drive inflation. Initially gold and other hard assets benefited, but as we know, the following years instead brought massive deflationary pressures as technological enhancements, globalization and cheap oil prices handicapped inflation. As each of those deflationary pillars weaken, however, whether by political will or economic/operational shifts, this time appears different. It’s something we wrote about in our last newsletter (“Inflation? Buckle-up”).

If there was any doubt about the scale, intensity and collective desire to force inflation upon the US, let those be laid to rest. Last week was a game-changer. Following much speculation, the Federal Reserve announced a major policy shift on Thursday at its annual Jackson Hole, Wyoming symposium (held virtually this year). Federal Reserve Chairman Jerome Powell confirmed that the central bank is updating its policy on inflation, and will begin to target an “average” inflation rate of 2% to support the economy and the labor market. Read that closely because the key word there? Average.

Targeting an “average” inflation rate of 2% means going forward the central bank will tolerate inflation rates above 2% “for some time” to compensate for the periods where inflation had fallen below the 2% level. In practice, this signals to the market that the Federal Reserve will delay interest rate hikes, its preferred method for taming inflation.

Can you say wow?

Since the 1970s, the Federal Reserve has operated under the dual mandate from Congress to promote maximum employment and price stability, but with the announcement, the bank has just mule-kicked the latter. As the Wall Street Journal recently put it:

“That increases the economic risk that the Fed might end up looking through inflation until it’s too late. Having effectively admitted it no longer fully understands the relationship between economic growth, employment and inflation, the Fed still promises to decide in real time when its healthy above-target inflation has become dangerous. If the central bank gets this wrong, it could be forced to raise rates much higher, much faster than it would want.”

Just think about this for a second here. What in essence happened to the Fed’s long-term policy goals this week was the effective abandonment of price stability. Setting an objective 2% inflation rate gave the Fed and market participants a hard target to take aim for. It heightens stability and predictability because as we approached the mark, the market and consumers can begin to react as they know what to expect from the monetary authorities. Now the guardrails are off. We’ve stopped bumper bowling.

Allowing the benchmark to overheat, places even greater pressure on the Fed’s subjective judgement on “how much” is too much and “how long” is too long. It also turns the Fed into an increasingly reactive body, as opposed to a proactive one, given the data lag, the impetus to overshoot going forward, and the market participants’ penchant to drive things (early and often) to the extremes. All of this suggests to us that once inflation really starts to get going, much higher inflation could be a self-fulfilling prophecy.

What people often forget about inflation or deflation is that much of what happens in those economic backdrops are influenced by psychology and human behavior. Similar to how financial assets go through periods of manias, panics and crashes (heck there’s an entire book about them by Kindleberger and Aliber), inflationary and deflationary pressures are subject to the same psychological fear and greed dilemmas, which can impact everyday goods/services.

The reason central banks fear deflation so much is that if consumers expect prices to keep falling in a deflationary environment, then they will pull-back on spending. In turn, the decrease in near-term demand places further downward pressure on prices.

In contrast, inflationary pressures can push consumers to pre-purchase goods and assets because they expect prices to rise shortly. In essence, inflationary forces can lead to hoarding, spiking near-term demand and putting further upward pressure on prices.

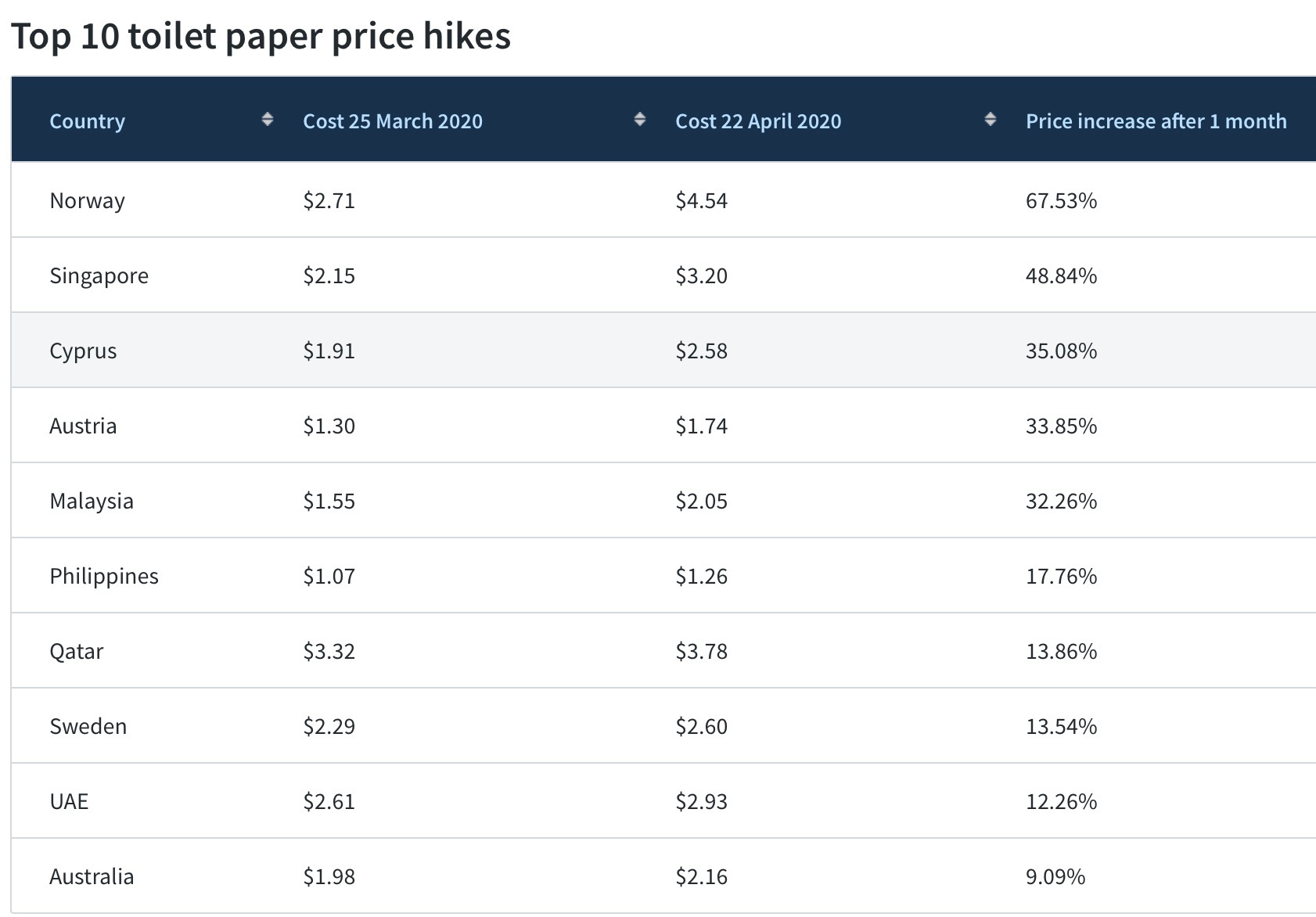

It needn’t be wide scale hoarding either. If your neighbor simply buys a bit more, you will too, despite no evidence of a supply shortage. Just think about the Great Toilet Paper Panic of 2020. In the US, the prices of paper products increased by 9% between March and April because of COVID. As of August, they are still higher by around 8% (WSJ) despite stocked shelves and sufficient supplies. It happened not only here, but globally as well (finder.com):

The psychological implications of inflation/deflation will also impact financial assets. If investors believe that a country has lost control over its ability to tame inflation, then money flows will reverse as investors sell assets denominated in the depreciating currency. This selling pressure can drive the currency value lower, increase the country’s cost of imports, and reinforce the upward inflationary pressures on prices. Inversely, if an investor believes your currency is the only safe haven left (relative to other currencies that are devaluing), then they will pile into it (or buy assets denominated in the currency). By driving the value higher, this can push import price lower, which increases deflationary pressures.

With the Fed’s policy pivot, there’s now a triumvirate of forces pushing in the same direction. Massive fiscal spend, institutionalized monetary debasement and fading deflationary headwinds are creating a fertile landscape for inflation to sprout upwards. Seeded in such soil, prices should rise, but so too will the number of bubbles, panics and manias. The market does what it does, and human nature is what it is. It will always push to the extremes given enough time. Don’t look to the Fed for stability though because the farmer’s just posted his new policy and he’s now taking a long nap.

So as the Fed embarks on this new journey of allowing inflation to run rampant for a period of time, it’s taking an extraordinary risk in trusting its ability to course correct faster than human psychology reacts. Again, we suspect that once inflation really does get started, it will be very hard to control.

We can attest to that at least in the energy market, which is a major driver of inflation. The abundance of shale capital has all but vanished and US oil producers are going to be in a declining/flattening production trend from here on out. This means that the only growth engine for oil supplies since 2010 has all but disappeared. Once the market realizes this, oil prices will have to shoot-up to appropriate levels to incentive the return of the marginal producer (i.e., offshore producers), which is north of $70/barrel oil. We have a hard time seeing how oil prices don’t overshoot in the coming years. US shale oil production is likely to remain below 12M bpd until 2023. Thus, if global oil demand grows at 2M bpd between now and 2023, the global oil market will experience a market deficit of 3M bpd (even if Iranian production returns), a scenario not many have factored in.

Asset Allocation Implications

The shift is already beginning as investors pre-position for the transition to a higher inflationary environment. We’re seeing prices for hard assets and metals begin to rally. Certainly some of these assets (e.g., gold, silver, bitcoin) are speculative, but so are insurance policies. The above three are going to be key beneficiaries of this psychological shift, which means investors will want to be positioned in them to participate. We will have a list of gold producers people can look at in a separate piece later. Since energy is going to be a key driver to this inflationary thesis, we recommend staying long energy producers as well. Ignore the short-term performance as we think the market is only realizing how game-changing the shift in monetary and fiscal policy is.

For now, all we see is the further bifurcation of the market; the growth in tech as momentum and indexing take the lion share of inflows. On the other extreme? Commodities, which are beginning to rise. As the transition continues, and as monetary and fiscal stimulus increases, we believe investors will still deploy new capital to growth stocks because . . . well greed/momo. As the tech shares top out, they will rotate further downstream because the narrative will shift from a “TINA tech + stimulus” to a “COVID recovery economy + stimulus”, particularly once a vaccine is approved (before year-end). We believe the broader market names will then see a rise as investors rotate into stocks representing the broader economy.

Nonetheless, for commodities and hard assets? Those will begin to enjoy a multi-year tailwind as we systematically debase our currency. Debt to GDP ratios will climb for the foreseeable future, so we’ve little choice than to reset the cycle and inflate our way out. Be prepared to gorge on those inflationary assets as the Fed just gave you a free pass to that buffet. Perhaps explaining why you’re seeing Warren Buffett as the first in-line.

Join the Distribution List

So that concludes this letter. We’ll endeavor to send these out weekly, so if you would like to be added to our distribution list click on the subscribe button above. This is our start and it’s our invitation to you to join us and share your thoughts. Welcome to Open Insights and let the conversation begin.