Bubbles and Bailouts . . . Everyone Gets One

September 30, 2022

Breathe.

Deep breaths.

Close your eyes and just breathe.

Inhale.

Exhale.

Paper bag in hand, that’s what most investors are doing. Staring at screens like this all day can send anyone into a panic.

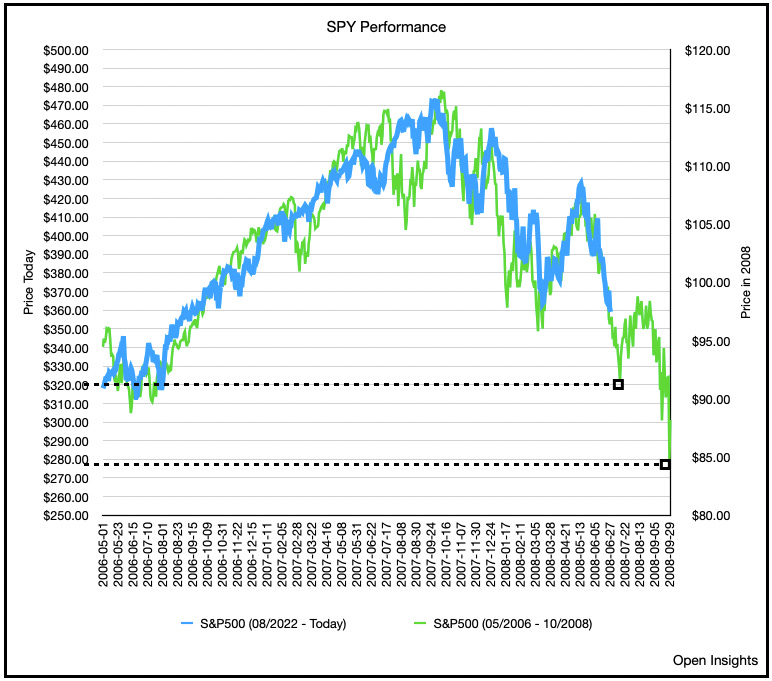

Asking the same question repeatedly. Where in God’s name is the bottom? We are close to 3,600 right? 18x a recession impacted $200/share, sounds reasonable right? You wrote that right? You said that. Sure, but as we also wrote . . . this is fear. Fear is contagious, and fear makes people do whacky things. Like stare at things like this and continue to marvel at the symmetry.

Yeah we know, it’s a silly analog, but we can’t help but look either. Could we fall to 3,200? 2,800? Sure because fear is twice as powerful as greed, so what goes up as fast, will come down even faster. In panics, you run when you see others run. Hence when bad news dominates, it’s all we look for; it’s all we can see, or want to see everyday.

Thus, we’re in the midst of a global repricing event. We’re witnessing everything fall as gravity reasserts itself as investors demand greater compensation for higher, stickier, more structural inflation.

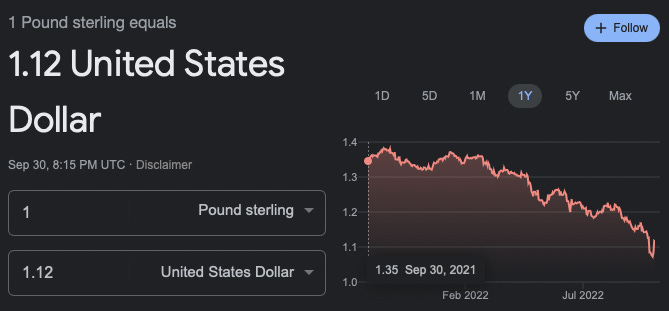

That’s scary as rates keep rising, but this is even scarier though . . .

Now that’s scary. That’s the UK’s version of the US 10-year Treasury bonds, which are called GILTS because they used to have gilded edges (when the bonds were issued in paper form). Those gilded edges have faded though as investors shunned the bonds after the newly installed Prime Minister Liz Truss released her budget calling for further stimulus.

Let’s just say the market was not pleased with the government’s largesse as interest rates suddenly shot up by 50% in a few days and the value of the British Pound crumbled.

What’s pernicious about inflation is that it pits the instinctual reaction of politicians (i.e., print money to subsidize pained electorates) against the market’s desire for austerity, demand destruction and eventual stability. Go against that and not only will the market call for higher rates on the money they’ll lend to you, they’ll even question the value of your money.

This is happening all over the world, and as the Fed continues to ratchet interest rates higher, the relative strength of the US Dollar is bludgeoning all other foreign currencies (at least the ones that matter). Japanese Yen, Korean Won, Euro, Chinese Yuan. Take your pick and every chart looks like the one above.

The US today is standing in stark contrast to the world. Blessed with abundant resources (i.e., energy and arable land), we’re an island of strength compared to everyone else. Despite our historic levels of public indebtedness, we still have three things going for us: 1. many other countries are arguably worse off, 2. we have an abundance of hard assets (i.e., again energy, food, land) that better insulates us against inflation, and 3. the US Dollar is still the reserve currency of the world. The latter reason will be particularly important going forward as commodities reprice higher given they’re mostly traded in US Dollars. The benefits conferred by a strong dollar are obvious to the Fed, especially as it continues its crusade against inflation. The dirty open secret is that the stronger the dollar gets, the lower the cost for imported goods. In turn, are we “exporting” inflation by forcing non-US consumers to pay more with their weakened currencies? ABSO-LUTELY. Sure, it hurts our allies, but what can you do when everyone’s fighting inflation. Better you experience the pain than me . . . just don’t say it too loud.

Let’s not, however, extrapolate ad infinitum that today’s conditions will remain in place. The strength of a country’s currency fluctuates with the strength of its economy. What’s the real appetite for the Japanese Yen, Korean Won, or Euro when its largest trade partner (China), or third largest in the case of the EU, is shuttered? Obviously lower, but will it stay that way if China finally reopens? We don't think so. This is not to say that we believe the US Dollar will weaken considerably (i.e., the factors that are bolstering its strength continues for the time being), but can/will the strengthening slow and even cease? We think so, and there’s more than a likely chance at that. Are we certain? No, then again what can you be certain of these days. What we’re certain of though is things don’t continue on forever in the markets. The market eventually reverts somehow, someway.

For the time being, this is a global repricing of all risk assets. It’s not a full-bore credit crisis because these are over indebted sovereign countries we’re talking about. They all have digital printing presses. So instead of massive cascading defaults, we think we’ll see (or are already seeing) large currency devaluations, higher interest rates and increasing commodity prices instead. Either way the cost of capital and the cost of things are climbing as structural inflation becomes increasingly imbedded.

Things could get dislocated though. The market may continue lower because of momentum, and may do so until the government (the lender of last resort) steps-in. Momentum, whether computerized or human nature, could drive us to such an eventuality as the fear of the “unknown” settles-in. Just as the UK pension funds unexpectedly needed bailing out on Tuesday, there may be other shoes to fall as markets trend lower, the cost of capital rises, reflexivity (i.e., lower prices causing lower prices) ensues, and margin calls begin. That’s the risk everyone’s wary of . . . financial cascade.

Still, how likely will the Fed repeat the “Lehman moment?” If the takeaway from the Great Financial Crisis in 2008 was to bailout our financial institutions and COVID was to bailout individuals and businesses, and the UK just bailed-out pension funds (i.e., investors) the day GILTS went “no-bid,” how cavalier will our Fed be about re-introducing “moral hazard” back into our financial markets if there’s an issue?

Think about that for a second. A Fed so worried about its reputation for treading too lightly on slaying inflation will willingly let financial institutions and key market participants fail without stepping-in? We highly doubt that. Things can get squirrelly, but the path of least resistance is to bail-everything-and-everyone-everywhere-out if it gets ugly. Well, even better though would be to pivot before such bailouts are needed; quickly and away from their current aggressive rate raising/quantitative tightening posture.

Do either of these scenarios equate to higher inflation? Again, ABSO-LUTELY, because every central bank can print money, but they can’t print commodities. More money, same amount of “stuff” = more inflation. So we’re stuck in this vicious cycle until we solve the supply issues, and that takes much longer than a digital printer. For now, we’re all searching for a bottom, a place where we can collectively agree that we have fully priced in the higher costs/risks of a more expensive world. Sadly, we’ve yet to find it.

For our oil investments, we know they’ll fluctuate, but we also know that financial crises tend to have little impact on real-world global demand. The inelasticity of global demand is very much a real thing, and depending on your timeframe, the dips are temporary. Here’s an illustration of what we’re talking about for the past 30 years.

Even if demand falls short this year (not even assuming growth), supplies are still woefully short, which is why even in today’s moribund economic state, crude inventories are still declining. While the global economy and financial markets can lurch down, eventually they’ll crawl back up. We don't think this time will be any different. We also don’t think China’s reopening, US SPR releases tapering, OPEC+ reducing supply, US production growth stalling, Russian sanctions, and Russian production likely falling has even been priced in yet, but sure keep selling oil off on demand concerns. You do you.

Again perspective. Own hard assets during these times when currencies are devaluing and inflation is rising. Own hard assets during these times of scarcity and supplies could be further falling. Own hard assets.

Or not.

Just breathe.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.