Countdown to Bedlam

June 19, 2026

Oooh that was a doozy wasn’t it?

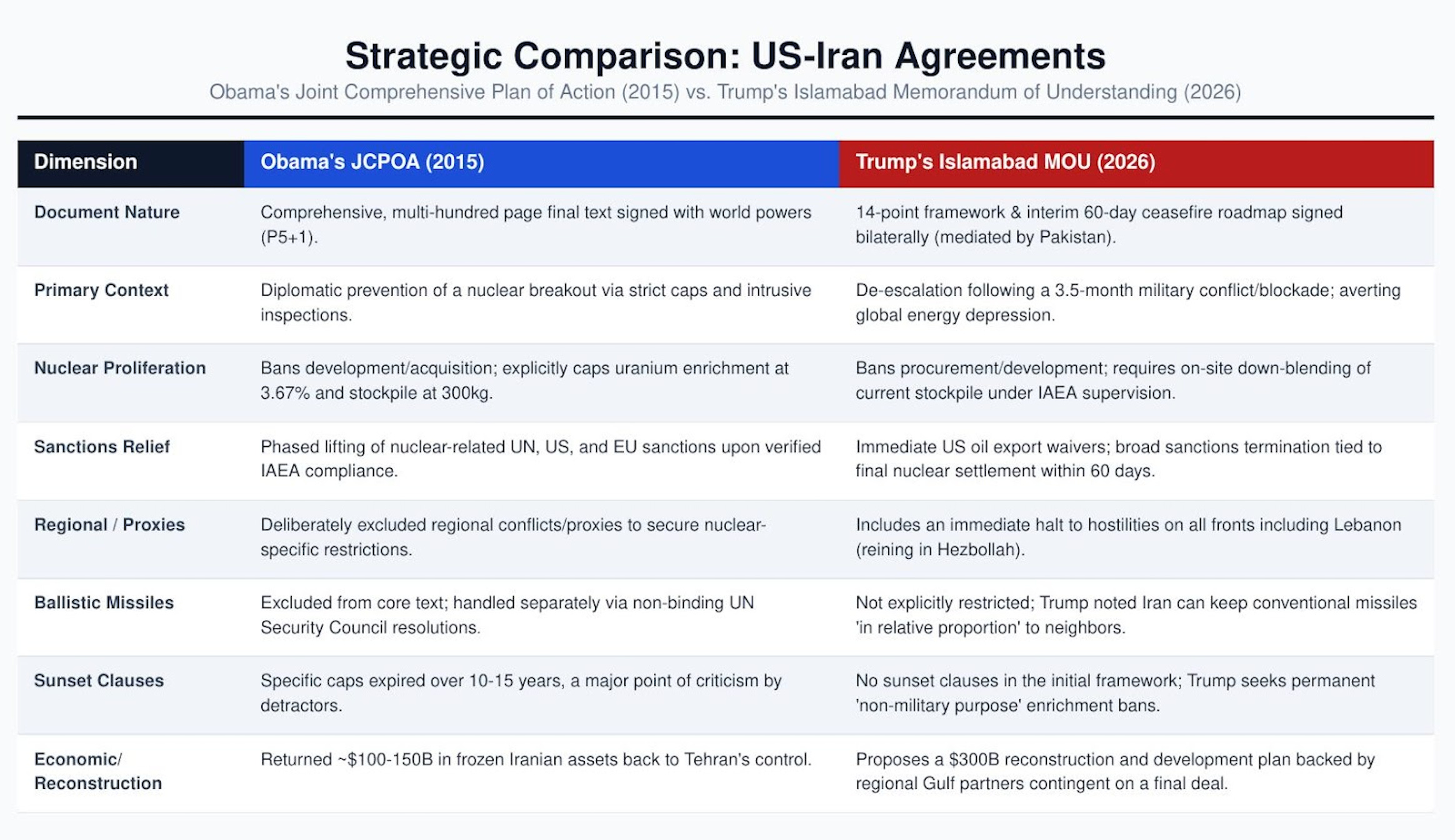

14 points.

14 points, each one a gut punch.

You knew it was bad.

You knew IT HAD TO BE BAD, since the US wouldn’t release the text until “the signing.” It’s like a report card gone wrong, and the kid’s hiding it.

What could begotten, was get. The Ayatollah’s channeling Inigo Montoya in the Princess Bride, and Trump’s saying . . . as you wish.

Man that’s painful.

$300B reconstruction fund, immediate lifting of oil sanctions, control of the Strait of Hormuz (“SoH”), no ballistic missile discussions, and uranium enrichment discussion to begin and last for 60 days until a “final agreement” is made . . . yeah good luck with that.

What about those Iranian frozen funds?

Yeah for sure, they gave that up. Under the table of course, but no doubt they gave on that.

For all the bluster and bellicose, this was capitulation born out of weakness. After months of fighting, blockades, and tightening sanctions, the US found itself in a completely untenable position. The Iranians warmed up for the World Cup by scoring on every shifting US goal post: regime change (still here), uranium enrichment (we’ll talk later), and reopening the SoH (how much should we charge after 60 days).

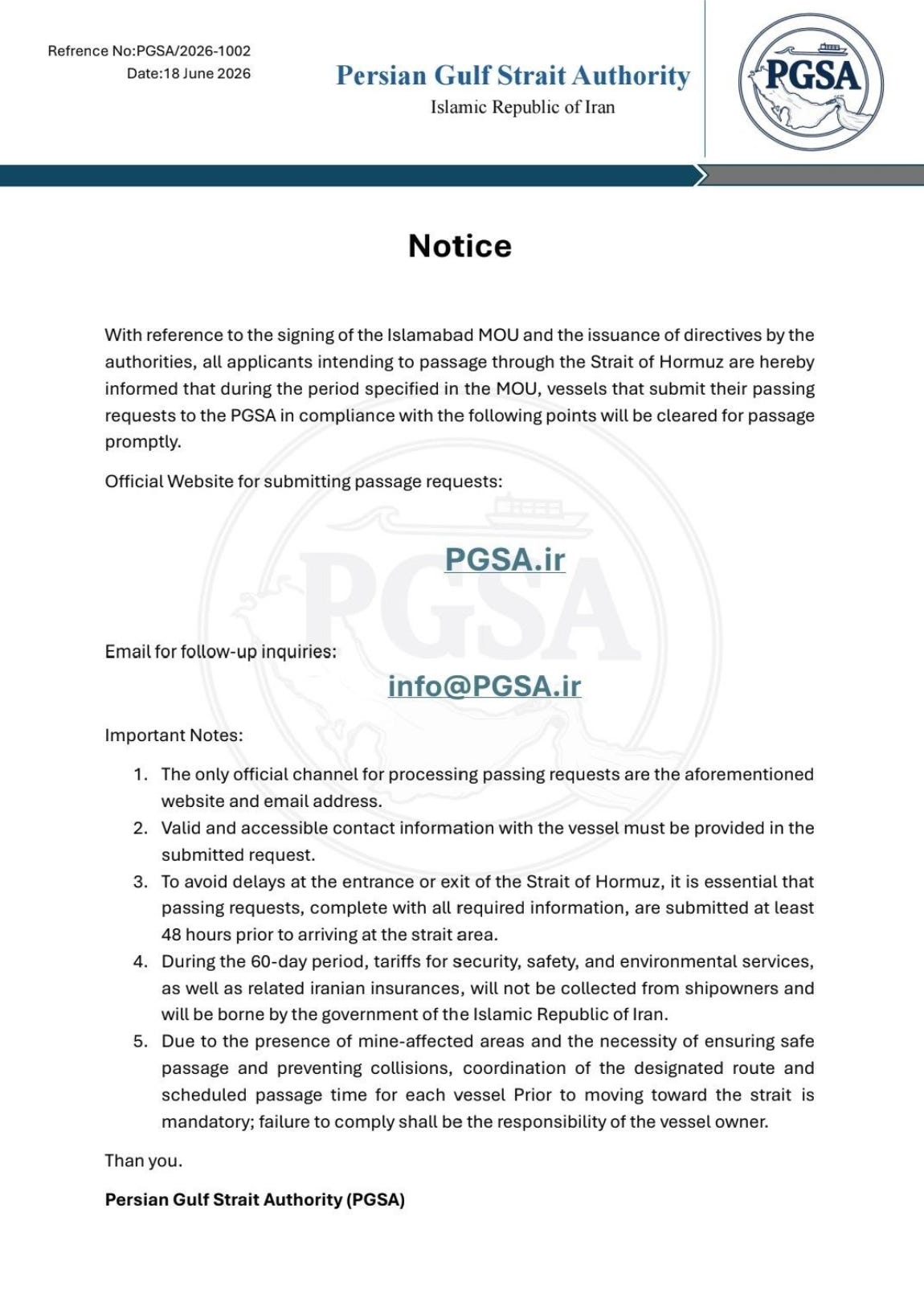

Ultimately, IR walks away now with de facto control over the SoH. Sure they’ve agreed “not to toll” during the 60 day negotiation period, but realistically why wouldn’t they after? It’s an added moat they’ve never had before, but open for a free trial period. Securing a nuclear weapon was always the golden ticket to insuring the regime’s permanence, and the IRGC worked hard to preserve that right. Tack on control of the SoH now, and they effectively control Iranian, Iraqi, and Kuwaiti exports. It also impacts Saudi Arabia and the UAE’s oil exports, but they’re already working on workaround pipelines, which means in a year, they’ll have repiped. Nonetheless if anything, the US/Iran War showed that energy infrastructure is highly vulnerable to asymmetric warfare. Drones, ballistic missiles, sabotage. These soft targets are simply too numerous and difficult to defend (cost effectively). Especially when it only takes one hit to disrupt operations. Pipelines help, but again, pumping stations are also numerous and vulnerable, so the threat remains.

Really though, all of this adds up to “friction.” The costs to defend, reroute, and redirect what was a VLCC dominated trade through one strait. The market invariably optimizes for economic efficiency, and anything other than a short pipe to the water’s edge means higher costs. Now it’s choosing between filling long pipelines flowing to different waterways, or subjecting yourself to tolls that previously didn’t exist. That’s your added cost.

What about geopolitical premium? Well let’s be honest, the market won’t give that to oil investors. China’s frankly done a fantastic job anesthetizing the world by flexing its strategic petroleum reserves (“SPR”). By slamming imports lower, and drawing on its stores (crude/petroleum), our Chinese brethren has bought the world some time, and arguably, the SPRs did their job. As did the US’ SPR. Sure, it’s been depleted severely and needs to be refilled (as the releases w\ere structured as loans), but for now, their release has prevented a stockout.

Tick, tick tick . . .

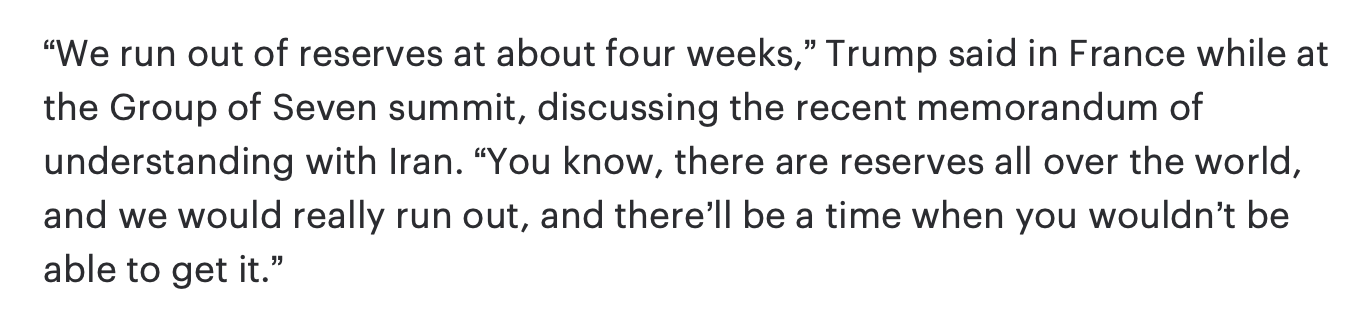

All of this had a clock though. The market couldn’t hear it, but oil analysts knew. The ticking kept getting louder and louder as the weeks passed. We had thought it was 6-8 weeks before bad things happen, but it turns out, those who knew . . . knew.

Unsurprisingly, the White House “declined to elaborate.” Um . . . yeah. Even in the palace of truth, that is a stunning admission. Sure, oil analysts suspected it, but to publicly divulge that data point means he effectively eroded the US’ negotiating leverage over the uranium issue. Notice also that the 60 day negotiating period is on the uranium issue, and not the SoH reopening. So once we cede control of the SoH (okay sure, shared between IR and Oman), the threat of stockout and bedlam will continue to exist. At any given point between now, the 60 days, and really . . . until we refill our tanks . . . we’re about 4 weeks away from “bedlam.”

Fantastic.

For all the uncertainty above, oil prices cratered to $75/barrel from $80/barrel last week. We think if Charlie Munger were here, he’d look at that and say . . . that’s just stupid.

It’s pricing in a full return to pre-war levels and normality, which my friends is EXTREMELY OPTIMISTIC. It presupposes that the winner, the Iranians, are thinking that way. It presupposes that they will negotiate in good faith and won’t intentionally leverage any advantages it has with the fact that they control a strait and the US/world is weeks away from a stockout. It presupposes that they will do so knowing that the US president has absolutely no desire to engage militarily. So no, none of that will happen.

So 60 days. 60 days while IR rearms and refills its financial coffers. 60 days of constrained tanker flows, and IR’s “management” of the SoH.

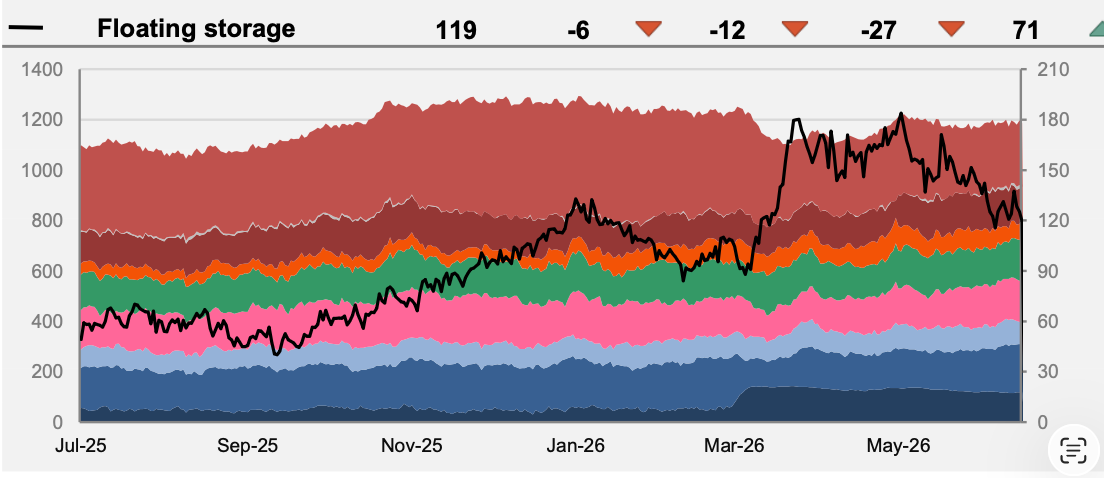

Sure we’ll shift barrels sitting in floating storage (i.e., trapped) in the Persian Gulf, from our left pocket to our right (outside of the Persian Gulf), but those barrels will forestall just a few days of consumption. While total floating storage is still elevated, much of it has already leaked out. We’re nearly back to levels seen in January.

Interestingly, we’re willing to bet that the recent decline in oil prices will spur increased demand in the coming weeks. It’s a sugar boost, but that’ll fade. The headaches of a vastly strengthened IRGC negotiating with a belligerent and weakened US are just getting started.

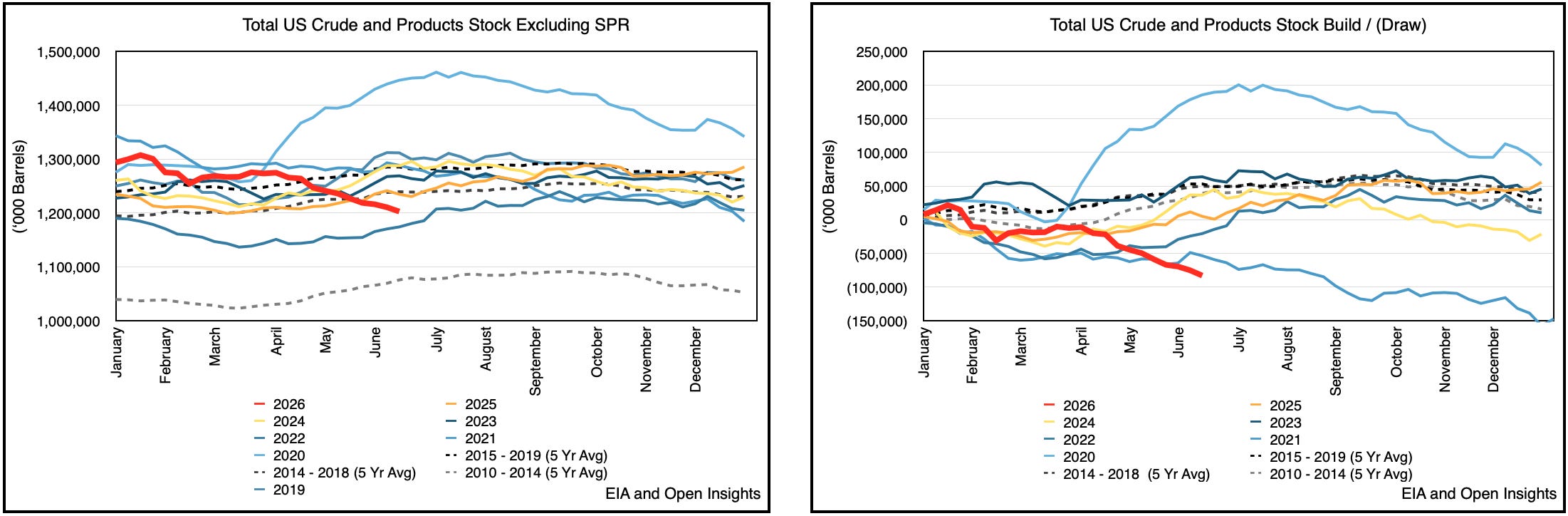

US oil inventories, the last bastion of reserves, will continue to draw for another 3-4 weeks.

We think European and Asian refiners will grab at the new flows coming out of the Persian Gulf and the US to refill coffers. They’ll need to buttress their stocks in case things go awry in the next 60 days. We’d be surprised if the buying shifts completely from the West (US) to the Middle East.

It’s why we think the oil market and oil prices are completely oversold. As the paper market fully unwinds, what’s left is the physical to discipline. In the short-run, with all the volatility, there’s going to be very few paper buyers. So the selling pressure intensifies and will peak. Eventually, we’ll find a floor as shorts unwind, and we think that’s in the $80s to 90s. Inventories would certainly indicate that $90s is the right figure, and nothing’s changed that unless the expectation is that dramatically large builds are coming even as the SoH stays impinged. We’re also entering the heart of the high demand season for the year. Tack on the recent fall in prices and the additional cargoes being released from the Gulf, and we’re likely to see demand pick-up.

Will prices run-away? Doubtful because again, China. It can and will likely continue to flex its SPR, which still contains over 1B barrels, and that can keep things in check globally. For June, imports appear to be at about the same levels as May, so the strategy carries on.

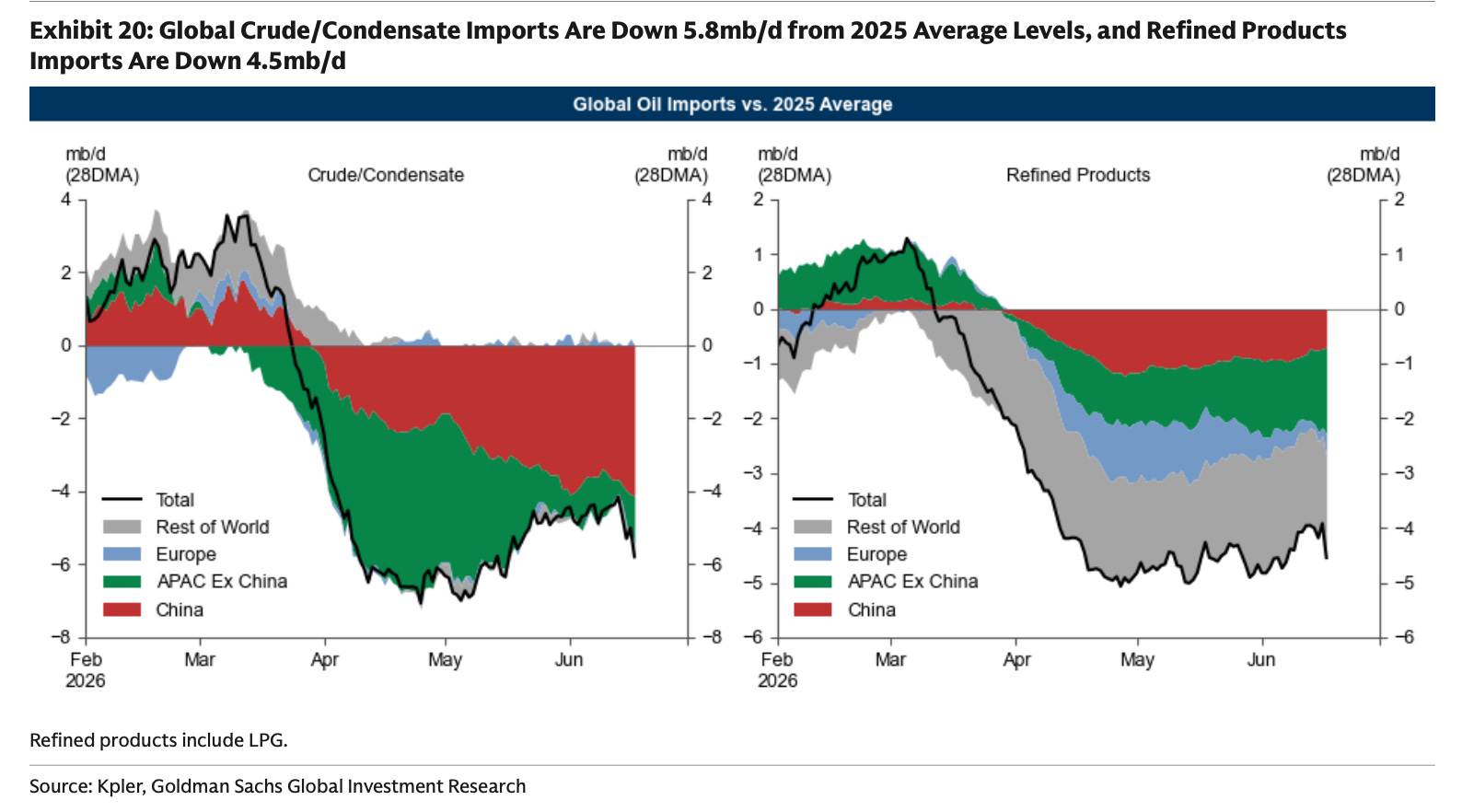

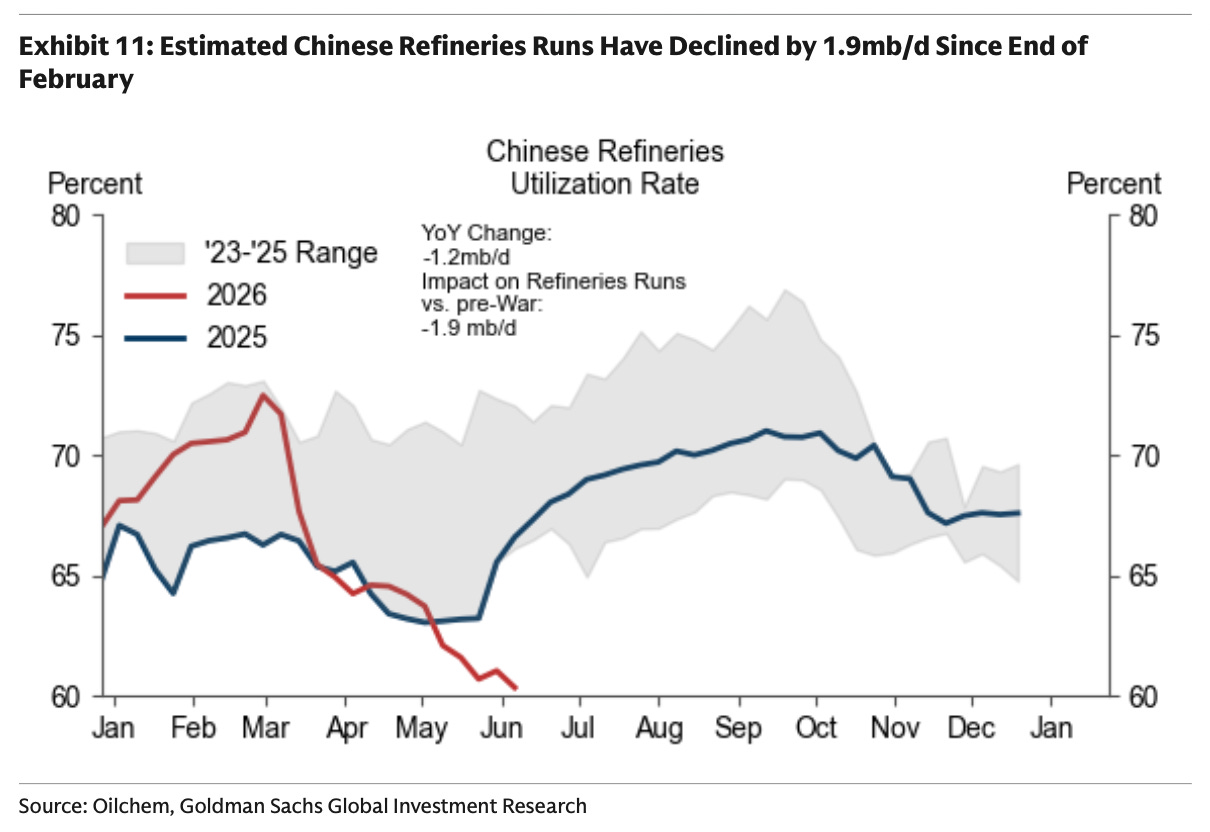

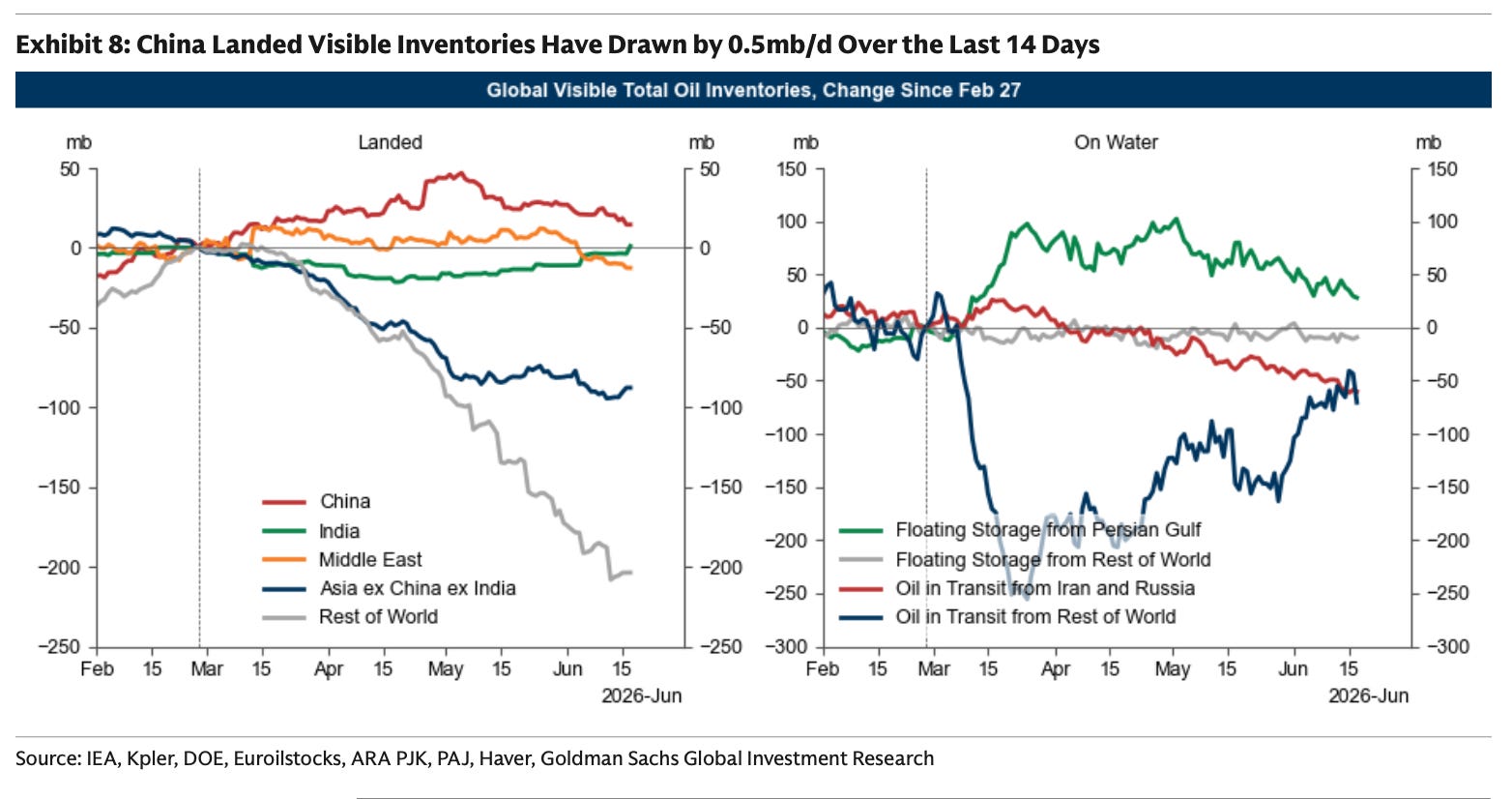

Look at the red section on the left. That’s China, slamming imports down by 4M bpd. About 1M bpd of that was “extra” to fill its SPR, and by turning it off, it’s really a 3M bpd delta. China then slammed refinery utilization down by 1.5M bpd, which likely means products drew.

The remaining 1.5M bpd? Crude draws. Only 0.5M bpd of that is visible, but they have caverns and the draws are likely coming from there.

If there’s one thing we’ve learned being an investor in the oil patch is that things aren’t always what they appear. Why aren’t draws higher, why aren’t prices higher, etc.? Much of the frustration coming from those bullish oil prices is that prices haven’t reflected the reality of what’s happened. You would think drawing over 1B barrels of inventory would usher in higher oil prices than the $75/barrel we’re seeing today, only $10/barrel above pre-war levels. You would think draining reserves, and being 4 weeks away from “bedlam” would mean prices rise to incentive all-out production to prevent such a possibility.

You’d think.

It isn’t, which means economically, what’s supposed to happen isn’t happening, and inevitably that will result in much higher prices later. Price inflation is always the byproduct of elevated demand and low supplies. That’s econ 101, and unless we can print molecules, the market will need to deal with that reality in the coming days. How long? Give it 60 . . . because even if the inventory data is murky, and the prices unreflective of the environment, we have little doubt the Iranians know where the pressure points are, and we have little doubt they’ll start pressing all our pain points.

14 of them.

We’ve made our bedlam, and now we’ll lie in it.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

Great article

I follow analysts that say the market is pricing oil correctly and therefore there is plenty of oil to go around. Up until the beginning of the year, the market was fairly balanced at a little over 100 million bbl/day production and consuption, give or take. Oil prices were set by the marginal barrel. A million bbl/day up or down could have a real price impact. All of a sudden, we are supposed to believe that a 10 milllion bbl/day deficit for several weeks is meaningless? I dont think so.

Nice article, Nelson.