E.T. . . . Elliott . . . Etsy

September 3, 2024

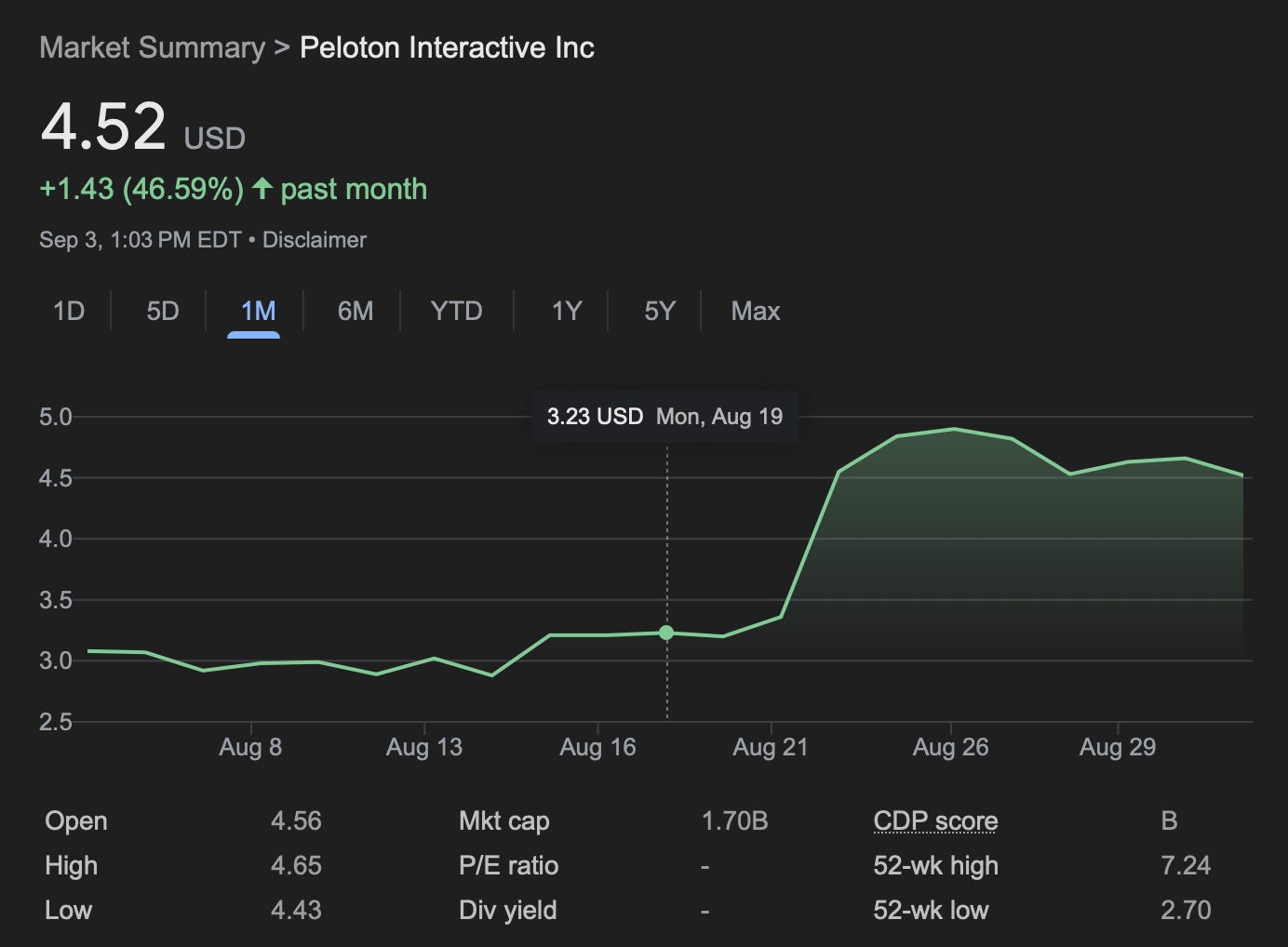

Well that was an interesting week. A few days after publishing our Peloton article, the stock certainly had a good week as the new management reiterated its strategy for revamping the company towards profitability, largely on the backs of cost cuts, which truth be told, needed to happen.

Pair steady recurring revenue with much lower operating expenses and eventually profit and free cash flow will find its way to the bottom line. Imagine that.

Well fortunately we didn’t have to wait long to see it. Now onto the next phase, which is CEO selection. Though to be fair, since the board fired Barry McCarthy, a “spend it and they will come” type of CEO after only 2 years at the helm probably means they’ll select a different sort of cat to bat the ball around this time. Good.

It’s about time. You don’t need a hero for this company, just a smooth operator for a company with a stock that’s been given up for dead. Overall we’re in a wait and see mode for the stock. It doesn’t always work out, but it’s sure more fun when it does . . . and quicker than you expect.

What’s also been fun is our jaunt through “anything else but energy.” As investors, we can get myopic, and we’ve certainly been that as we’ve poured over an energy thesis that’s partly worked, and mostly not. The volatility has been brutal these years, but we stick with it because we do think (eventually) that lower investment in the space will bring about higher prices . . . it . . . just . . . takes . . . so . . . long.

So while we wait, we may as well explore a bit and see what else is out there. Sometimes though what others see, we don’t quite see. Case in point? Etsy.

Yes, our curiosity was piqued after Elliott Management took a position in the company.

Previously we noted that they’d taken an interest in Pinterest in 2022, but looks like they’ve turned their gaze towards Etsy in Q1. 13% later, voila . . . a board seat and a say in how they run the company.

The stock certainly needs it, after melting down nearly a third this year . . .

. . . and down 80% from it’s all time higher of $294/share a few years ago after COVID accelerated/pulled-through growth. It’s been rough, and a case of another company (like Peloton) that rode the pandemic wave, and then crashed out when consumer behavior reverted back.

Since we’re always in the market to learn, and pick through things others have discarded, let’s take a look.

On first glance, this business isn’t that complicated. Sure it’s tech and tech is “complicated,” but the business itself isn’t “complicated complicated.”

Deep, we know.

So Etsy in its own words does the following. It create marketplaces where buyers connect with sellers that make “unique and creative goods” for consumers “looking for items that are a joyful expression of their taste and values.” Niiice. So basically a virtual swap meet so you can get your very own hand carved charcuterie board made in walnut (not that we’ve looked or anything). Unfortunately for Etsy, not as many consumers are looking for a joyful expression of their tastes and values of late. This virtual swap meet just hasn’t grown much post-COVID.

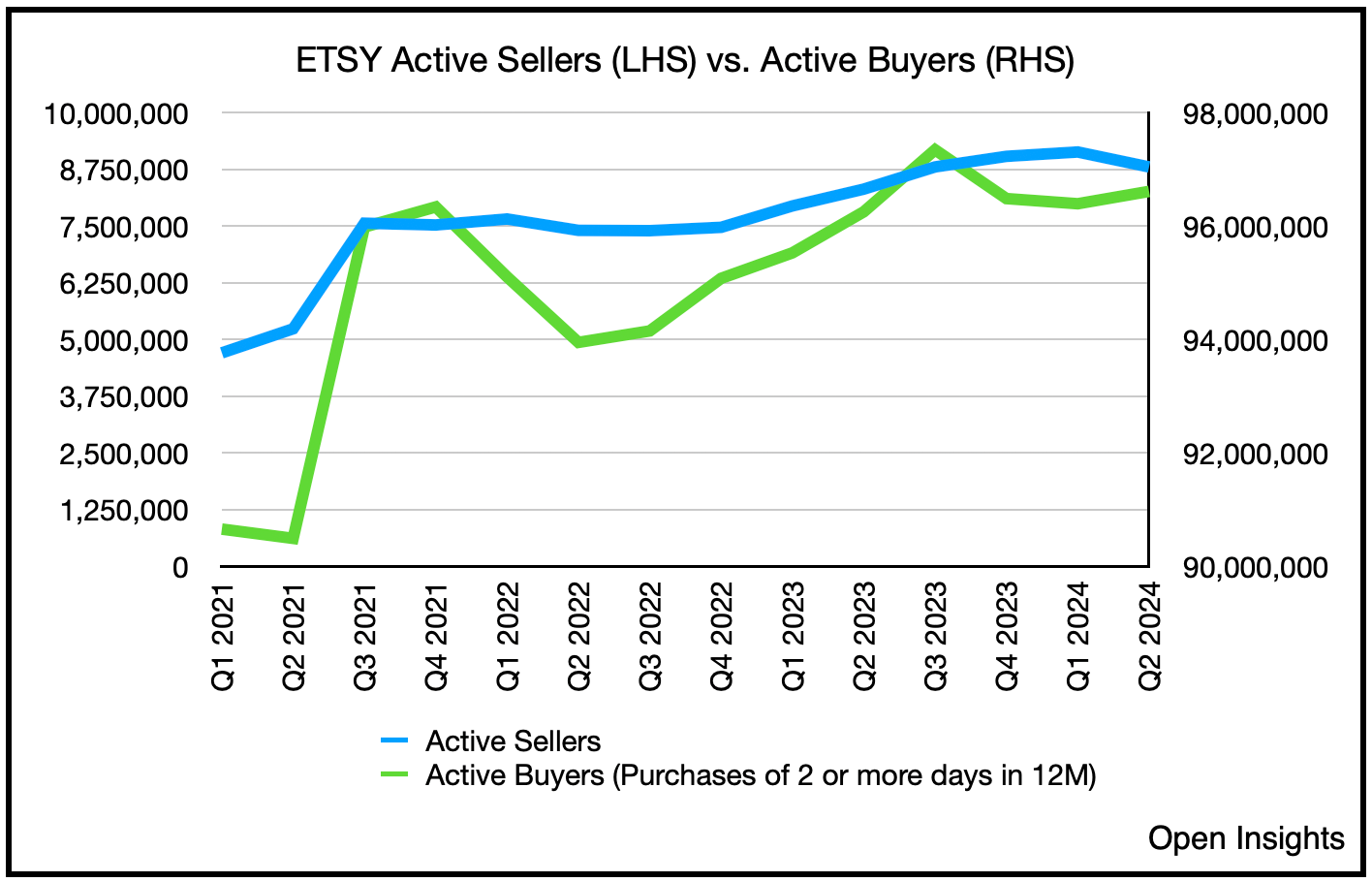

From a high-level perspective, the growth in the number of active sellers and buyer (i.e., those who buy 2x or more a year) has been climbing, but only by low-single digits year-over-year.

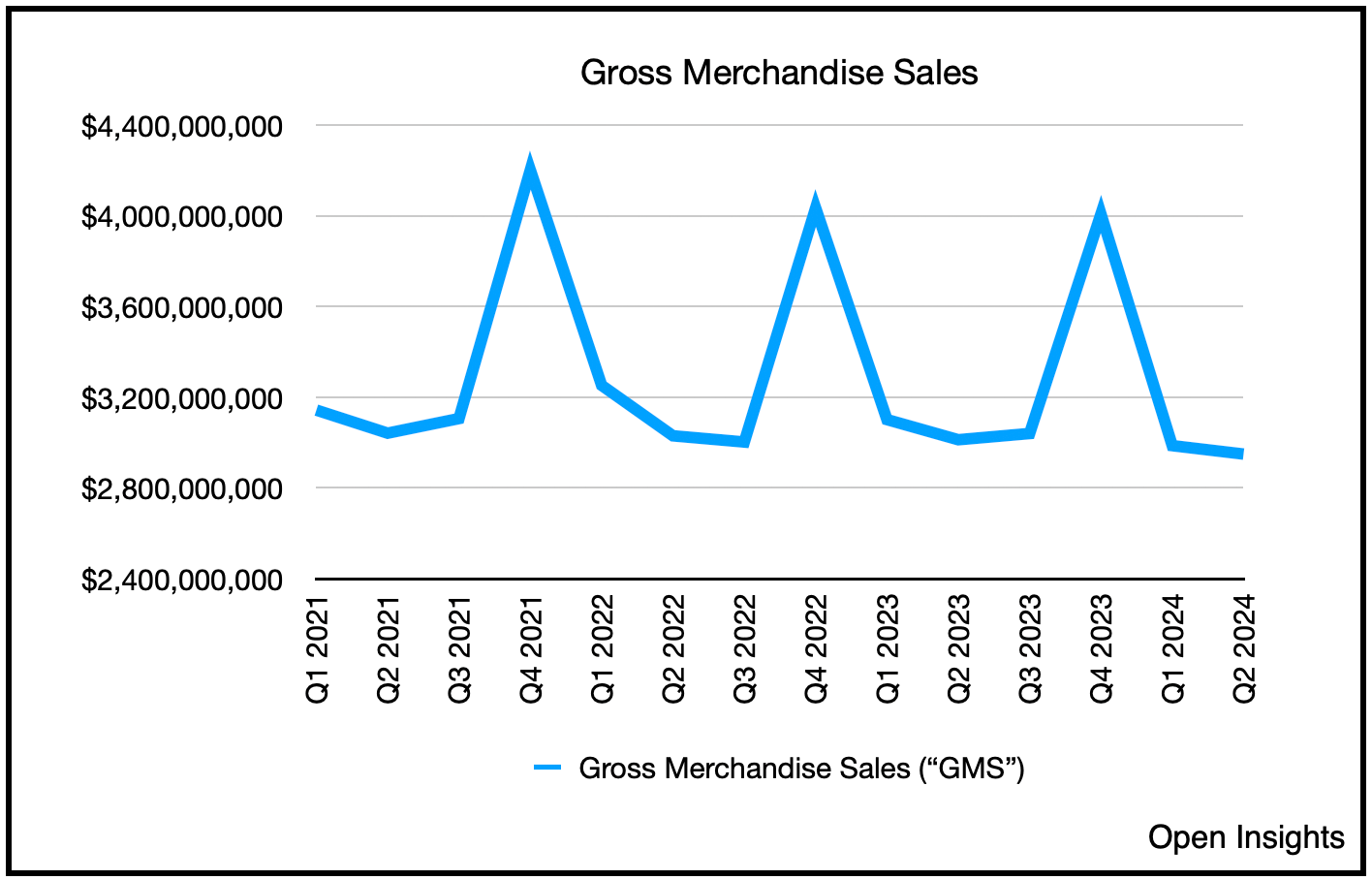

A lack of material growth in the sheer number of participants, means that the value of goods sold in the marketplaces have similarly stagnated.

Them’s not a great trend. Sure there are spikes, but that’s explainable by seasonality (think Christmas and holiday sales). Even then, the spikes are lower, which means the busy seasons just aren’t as busy.

So that’s your market . . . or “marketplace.” It’s a large one, but it’s stagnant.

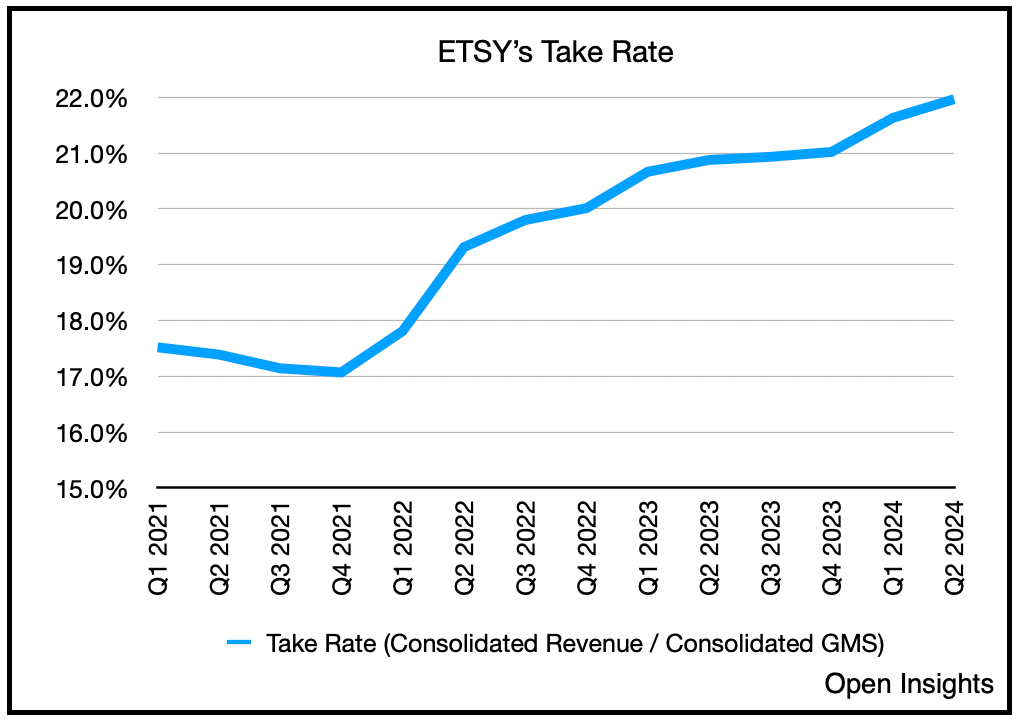

What’s Etsy’s cut for playing matchmaker? 22%. Unironically, it’s called the “take rate,” in their corporate parlance, but it follows the 80/20 rule we all know and love in life, and for Etsy that take rate has been about ~20%.

Note the trend though. Their cut’s been steadily rising as the quarters have gone by, but be wary. If you squeeze people too hard they’ll start to feel it. Especially if the growth in sellers outpaces the growth in buyers. Sure the growth may be in different categories, but overall if sellers in the pond outgrow the buyers, eventually what gives is price. Eventually if you don’t make enough, or competition is too stiff, you stop competing. Note the number of “active sellers” (i.e., the people who actually bear such costs) in the blue line below? Declining.

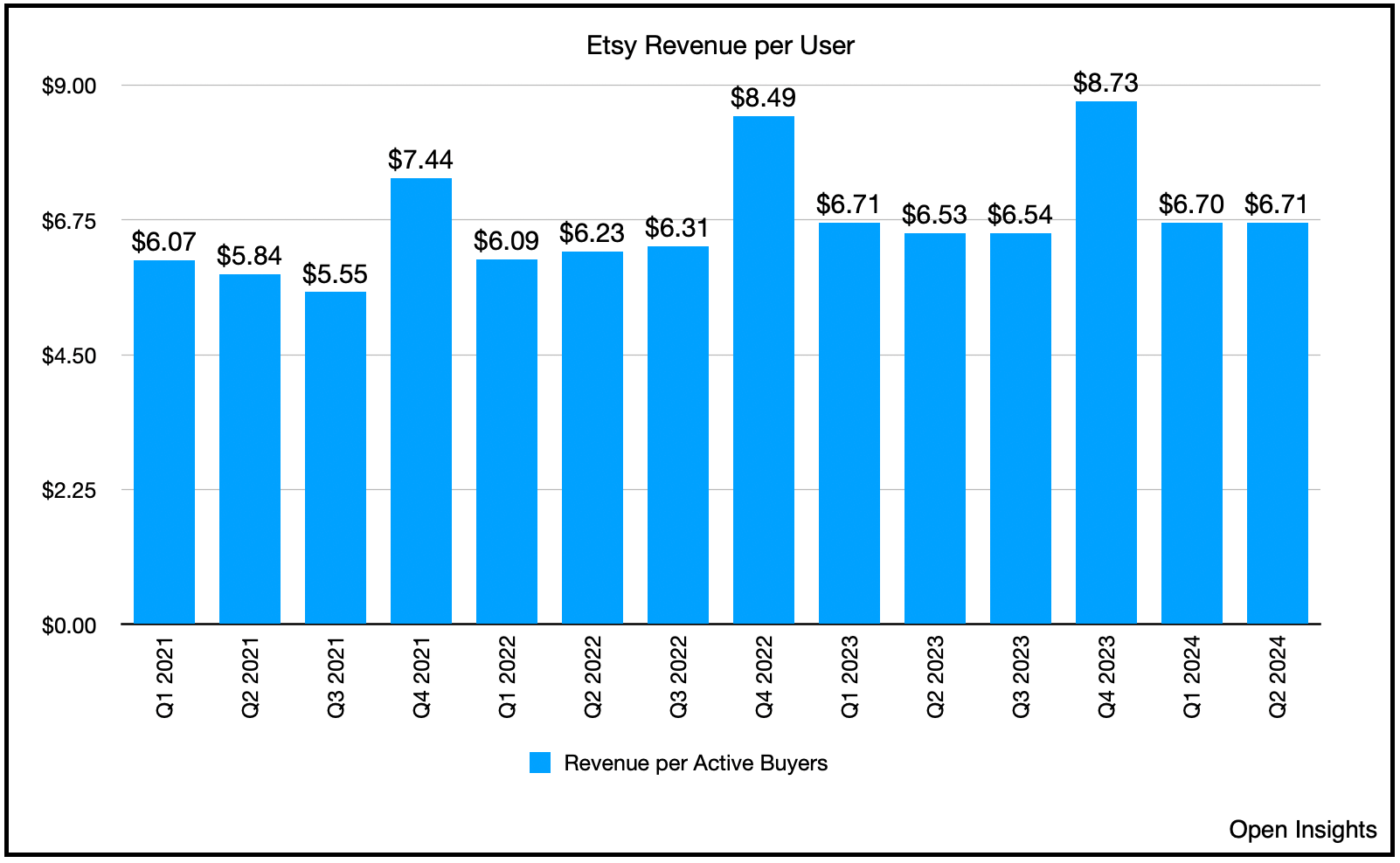

For now though, you can see what’s happening. Small growth in number of Etsy users coupled with small increases in the take rate, and you get rising Revenue per User.

Seems okay, but what you’d prefer is the ecosystem/marketplace growing, and your take rate growing with it, as opposed to you squeezing the marketplace.

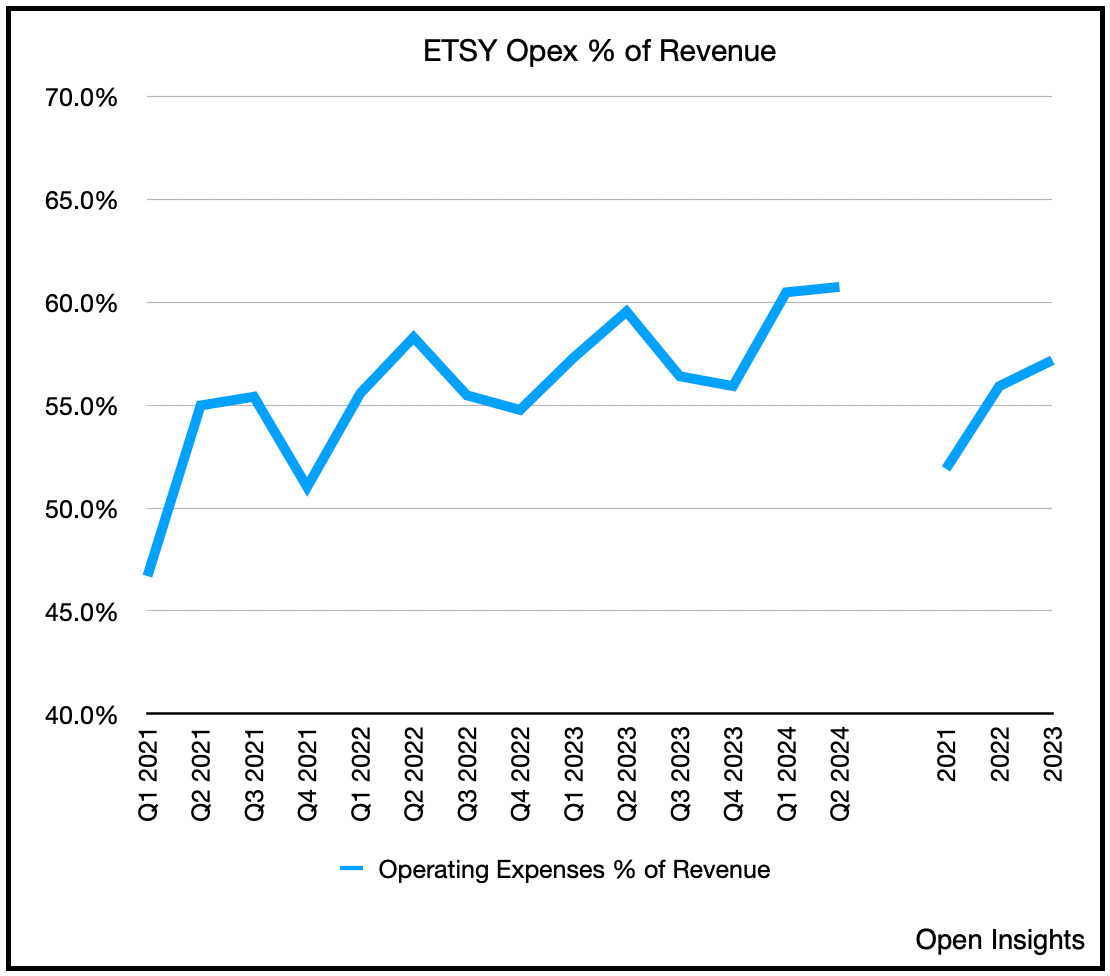

So that’s top line. How’s the rest look? Operating expenses typically soak up about half of that revenue, and it’s been creeping up, though not materially. Just enough to absorb the higher revenue we’re seeing from the growth.

Maintenance capex is pretty negligible except when they try to buy marketplaces at sky-high tech valuations. Inorganic growth is growth, but it’s pricey when they don’t pan out. Two acquisitions in 2021 were particularly costly. Elo7 (a Brazilian online marketplace acquired in July 2021 for $217M)) was recently sold for negligible amounts, and Depop (a second hand clothing marketplace purchased for $1.625B in July 2021) was recently written down by $897.9M. Think about that for a second, especially for Depop. Purchased for $1.625B, goodwill (i.e., “plug” for money you paid because you really want that asset) was recorded at $1.1B. So $500M of “real stuff” and $1.125B of “I really wanted it so I paid up for it.” That $1.125B? Written down by ~$897.9M. Talk about buyer’s remorse.

Okay, we’re being a bit harsh because at the time of acquisition, Etsy was a nearly $20B market cap company, but incinerating $1B in capital is still pretty costly, especially when debt was around $2.2B. Other than those flubs, capex spend falls around $40M per year.

So sum it all up, we basically have a stagnant $7.3B market cap company generating about $650M of free cash flow (“FCF”) a year, for a 11x, or ~9% FCF to market cap company, post-pandemic.

So really it’s not entirely bad. It’s just not growing.

For a tech company.

Okay that’s bad . . . well maybe not bad, but certainly “meh.”

So we don’t get it. What’re they seeing with Etsy? Well certainly if they can increase the number and value of transactions in the marketplace, you’ll get significant operating leverage. If you hold operating expenses flat, and there’s immaterial long-term capex costs, everything falls to the bottom line. It just seems difficult given that they’ve been trying for nearly 3 years with little progress. Still, it certainly is trying as they attempt to launch Etsy Insider, a new loyalty program in mid-September. It’s a beta phase launch, so think of it as a soft launch. We’ll see if this paid subscription program (e.g., Amazon Prime) that provides free shipping and discounts/first access to its members will take off. Best Buy pulled it off, so maybe Etsy?

Interestingly, perhaps, the playbook they’ll borrow will be one from Pinterest. In 2022, Elliott took a position in Pinterest, and by year end, a board seat. Elliott’s PR statement read:

“Pinterest is a highly strategic business with significant potential for growth, and our conviction in the value-creation opportunity at Pinterest today has led us to become the Company's largest investor. As the market-leading platform at the intersection of social media, search and commerce, Pinterest occupies a unique position in the advertising and shopping ecosystems, and CEO Bill Ready is the right leader to oversee Pinterest's next phase of growth. We commend Ben Silbermann and the Board on the leadership transition, and we look forward to continuing our collaborative work with Ben, Bill and the Board as they drive toward realizing Pinterest's full potential.”

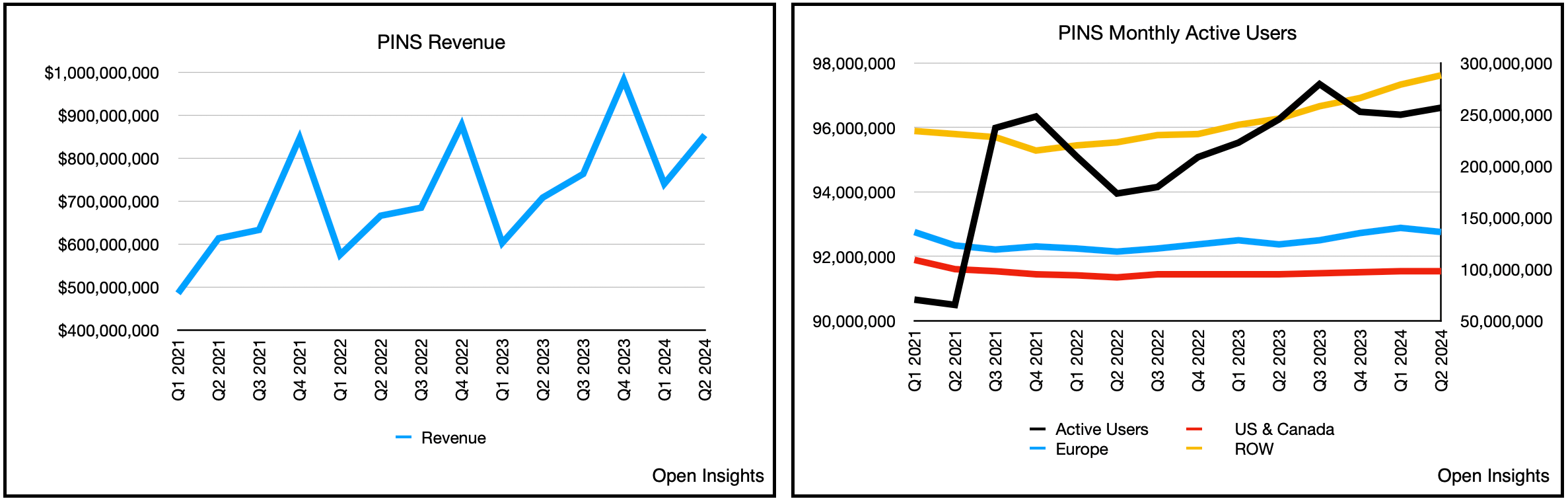

Marc Steinberg, a portfolio manager at Elliott, ended up filling that board seat. Since then? A new CEO, revised strategy and cost discipline has seen revenues increase globally by 21% and monthly active users by 12%.

The revised strategy has helped, and the stock had almost doubled in the past 2.5 years since Elliott took the position.

A recent quarterly flub, however, tanked the stock back to the low $30s, but diving through those numbers, the market’s reaction may not have been warranted. Execution appears to be strong. Nonetheless, you can see, if your marketplace/ecosystem can grow, then your sales can grow. Pinterest sells advertising to advertisers, and your Pinterest boards are lead generators. Grow the number of users, and you’ll grow the number of potential customers. Etsy is pretty similar, grow that marketplace, and you’ll grow the number of transactions, the value of those transactions, and your take rate. The common denominator? Grow.

We think it’s early days in Etsy’s turnaround. Elliott’s jumped in, and likely offering the same Pinterest-pitch. Grow the market, control operating expenses, be smart when allocating capital, and watch-out for capital dilution (from share based compensation). It’s a pitch we can get behind. It’s just a bit early though for us, so we’re not swinging at it yet. We may take a starter position just to see how it develops, but we’d like to see a bit more as to how Etsy will articulate that process. More importantly, let’s see if Etsy Insider even works . . . before we phone this one home.

Eeellliiiooottt.

(That’s an E.T. reference for you younglings out there).

Please hit the “like” button and subscribe if you enjoyed reading the article, thank you.