In These Uncertain Times, Just Ask, What Would Buffett Do?

April 28, 2023

I get calls now. I figured I would. It’s human nature. We released our year-end letter a few months ago and yeah . . . we did okay. That’s after doing okay the year before, so two years of okay is . . . pretty okay. Investors see that and think it’s fascinating. Something interesting is going on there. They must have alpha.

Which is a funny word, alpha. In finance, it’s the outperformance over the market, or your benchmark, beta. In another context, it evokes the show Billions and for fund managers, the alpha males, the BSDs in Michael Lewis’ Liars Poker. Alas it’s mostly male still, but undoubtedly there’s women. Still regardless of sex, the notion’s the same. We came, we saw, we conquered. We will tame this market with our intellect, acumen, and algorithms.

Behold our alpha.

We are the captains of the industry.

So I sit here with “alpha,” but I know such things are a mirage. It’s fleeting, like my neighbor’s cat, here one minute, gone the next, especially if you’re measuring on a month-to-month basis, or heck even in some years. Do I think I can generate alpha over a long period of time? Of course . . . if you think otherwise, why are you here? More pointedly, doing otherwise means you’re adding zero value, or more likely negative value.

So yes, I’m confident, or humbly so, if there’s such a thing. Yet, I hedge these days. I find myself hedging my thoughts. Waffling permeates all that I say or do. This “should” happen, I “believe” this is will occur, and that’ll “likely” pan out. “Will you pick up the kids?” the wife asks?

I “may” . . . or may not.

None of it sounds like alpha, and none of it should. It’s unintentionally intentional because while I’m confident in the analysis, reality is REAL, and reality has a way of throwing curve balls at your head. If you haven’t been humbled by the market, you haven’t been in the market long enough.

Which is funny because other industries do it. Well dressed moderators invite analysts to share their thoughts. Whether its CNBC, Fox Business News, The 700 Club, or the Psychic Friends Network, uncertainty exists, and it must be/can be resolved.

Just think about the latest angst in the market. Are we, or are we not in a recession? Has it passed, is it now, or will it come? Nobody has a clue, and yet we debate with such conviction. I’m right because my tweets say that I am. I’m right because my charts say that I am. Nevermind that by nature we tend to see and seek out confirming evidence.

Which is why lately, after crafting our quarterly letter, I find myself regressing. I catch myself stepping-back a bit and asking that question I tend to ask myself when uncertainty is high and doubts fill the air.

I’ve been asking myself lately . . . WWBD?

What Would Buffett Do?

Buffett. Yeah you know him, the intellectually spry nonagenarian still allocating capital seven decades on and still grinding out returns higher than pretty much everyone else. He needs no introduction so we’ll waste no space doing it. I’ll admit, I’m not like the fanboys out there who’ve read everything ever written about Buffett, nor have I visited Omaha. Read a few biographies? Yes. All his letters? Yes. Seen a few interviews? Absolutely, but that’s about it . . . but I think that’s enough. It’s enough to appreciate a master at his craft.

You read a few of these things and you can get the gist of what he’s trying to do. How he’s trying to play the game. It’ll be hard for you to replicate his game because he is after all . . . Jordan. It’s impossible to replicate an investor who’s a genius, slightly autistic, and possessing a near eidetic memory along with preternatural patience and emotional control.

You ain’t Jordan, and we ain’t Buffett.

Despite our limitations though, we think asking “WWBD?” helps. Asking, “WWBD today?” helps. It helps because the Buffett of today has a broader perspective now, no doubt stemming from his burgeoning conglomerate. Gone are the days of “cigar butt” investing, and buying below book value. Replaced with competitive advantages and favorable terms. With vast sums of capital, and increasingly the lender of last resort, his empire today is a perpetual motion machine of M&A, carried along by float, and helmed by cold rationality. Having said that, Berkshire’s expansive reach (and his penchant for reviewing data daily from his various operating businesses) gives him a broader and simultaneously deeper understanding of what’s happening in the economy.

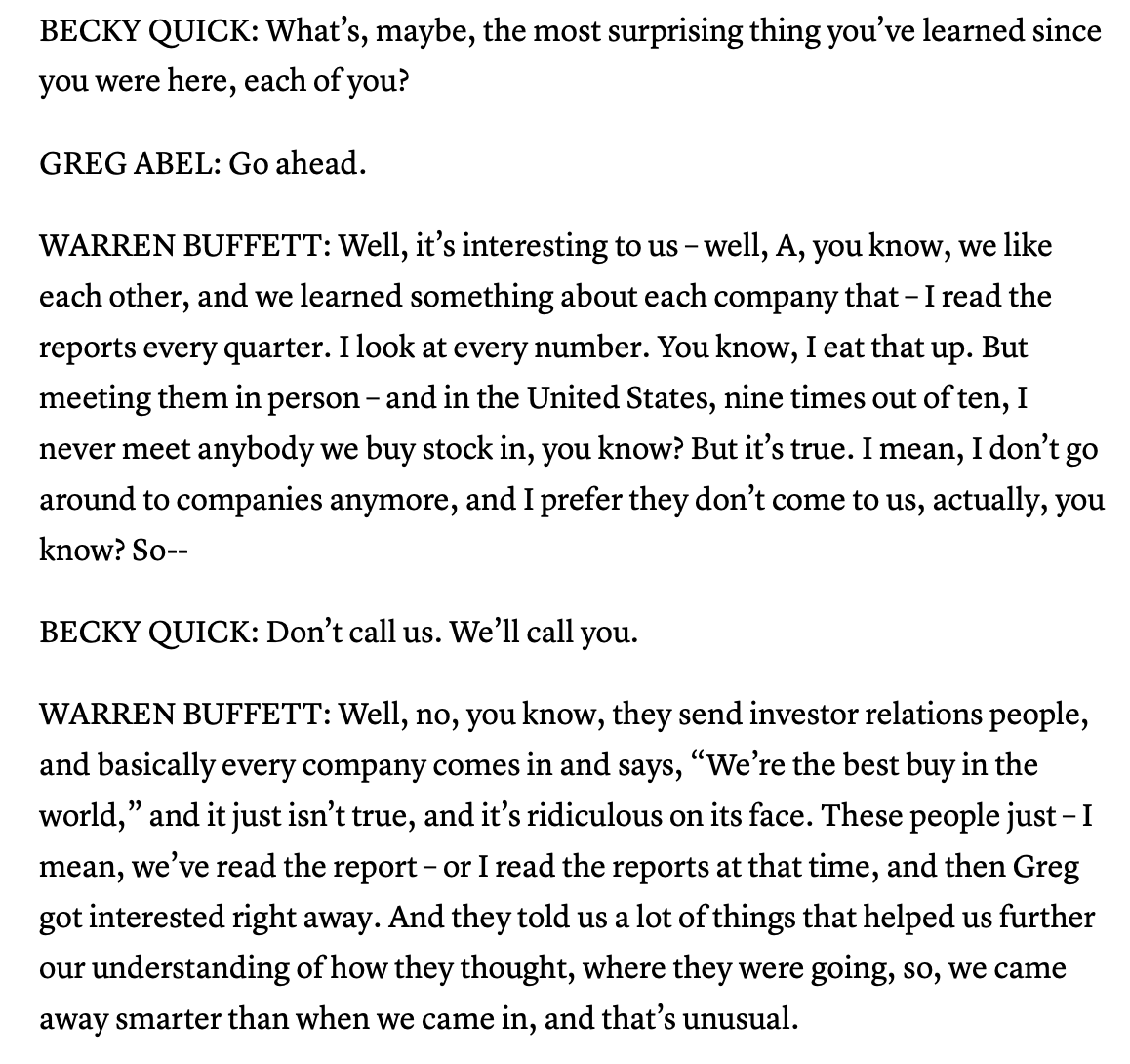

So as we stepped back a bit this week and caught-up on our reading, we came across something interesting, an interview Buffett did with CNBC.

Perfect.

Let’s ask . . . WWBD?

Recently, Warren Buffett and Greg Abel (his designated successor to lead Berkshire Hathaway), flew to Tokyo to visit some of the Japanese trading companies he had invested in in 2020 (Itochu, Marubeni, Mitsubishi, Matsui, Sumitomo). These companies are essentially Japanese Berkshires, conglomerates involved in insurance, commodities, industrial production, trading, chemicals, etc., and Berkshire recently increased its stake to ~7.5% in each entity, and has promised its ownership will stay below 10%. Doing still effectively gives him a toe-hold into expanding Berkshire’s influence/operations and capital allocation into Asia in the coming years.

To us, this wasn’t just about Japan, and a few undervalued Japanese stocks. It’s especially not just about these investments if you’re willing to fly a 92 year old person halfway around the world to meet the management teams of these companies. It’s about paying respects in a deeply respectful culture, building relationships, and using Buffett’s personal brand to open-up windows of opportunities in Asia. Buffett’s ownership and deep pockets means the trading houses can essentially become a consigliere to Berkshire into Asia in the coming decades. So our first takeaway on WWBD?

Go East Young Man. Go East.

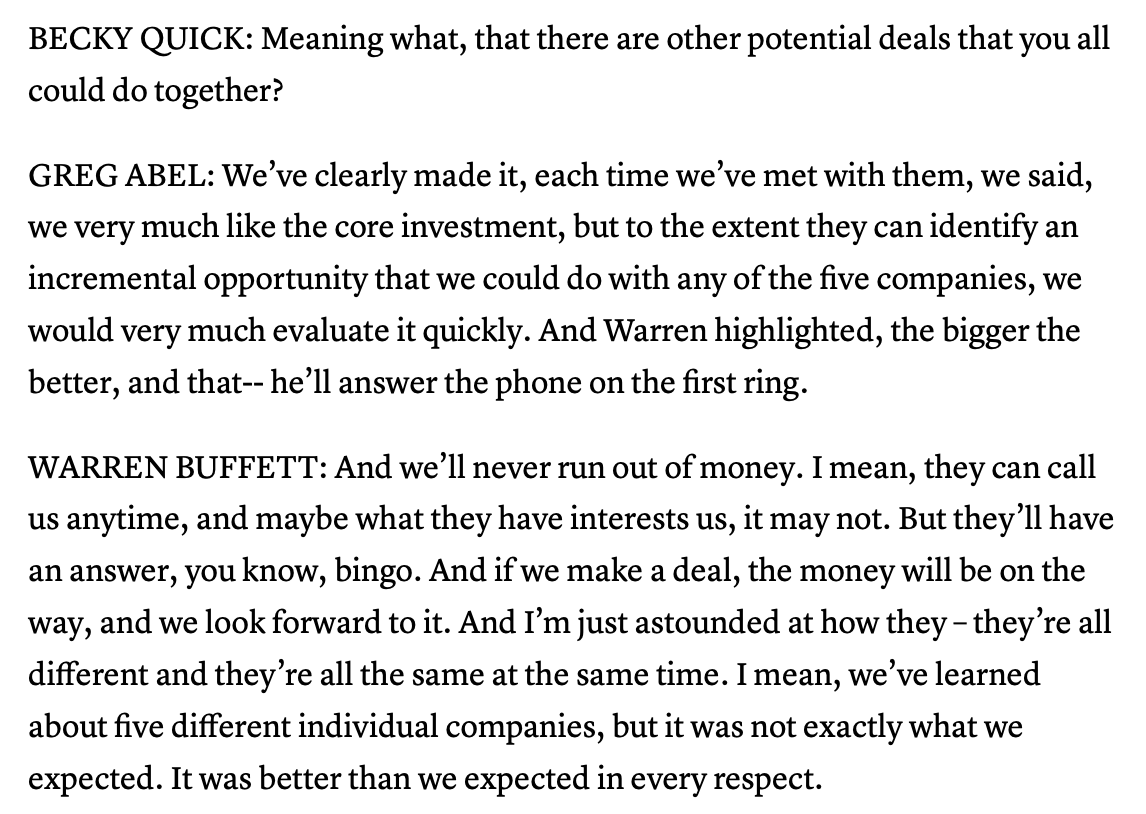

The other thing that struck us (or perhaps reinforced), is that great companies, truly great management teams are hard to find.

Social media has democratized opinions, and particularly so in finance. More information can often lead to more insights, so that’s not necessarily a bad thing. It is a problem, however, when the loudest voices (i.e., those with the most “followers”) are the ones that cut through the noise. We’re inundated with information and opinions, and essentially everyone’s touting something they own as the next “buy” or “must own.” The reality though is much much harsher. Most likely the Pareto principle (i.e., 80/20 rule) applies. There are actually very few “good” companies, and even fewer “great” companies. Invert that logic and it means . . . almost every company and every investment is a mediocre/bad one. So be discerning to save capital and time. In our echo chamber of cacophony, sound judgment is critical to sound capital allocation. So the second takeaway?

Not Everything is a Buy, in Fact, Few Are.

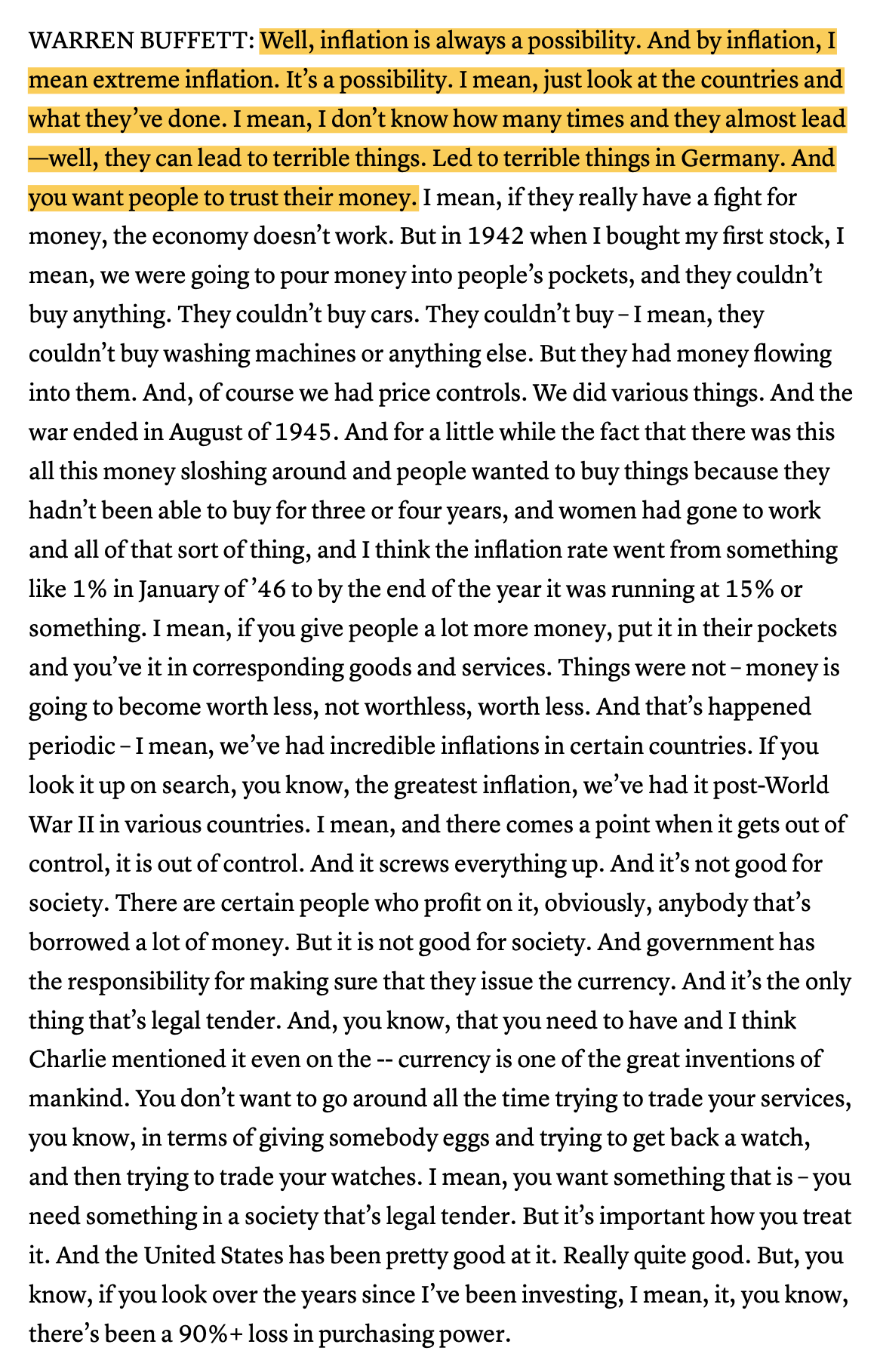

Onto a third insight. Here’s what Buffett said . . .

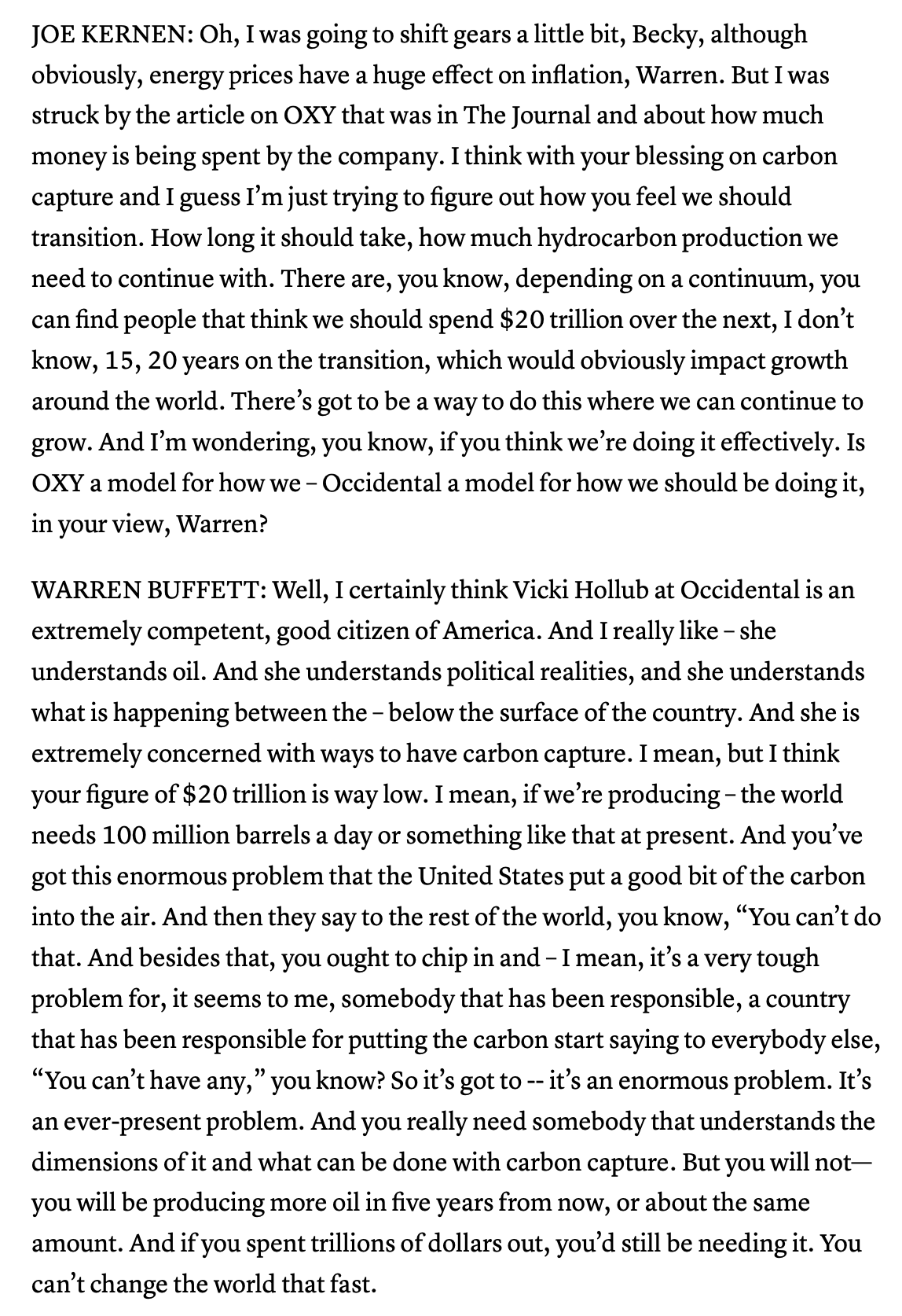

This view isn’t surprising, nor particularly insightful if you brush up on history. What makes it more interesting is if you then tie it back to his investments in the trading houses. Japanese trading houses are heavily involved in the trading of physical commodities (i.e., real stuff). Real stuff tends to appreciate in an inflationary environment. Ponder further his recent purchases of two oil companies, Occidental (~30% ownership) and Chevron (~8.5% ownership). Oil companies certainly aren’t Apple or insurance.

All of these companies aren’t typically great businesses. They’re far from the toll takers, competitively advantageous, and float-y type of companies preferred by Berkshire. Logically, these actions could be an effort to buttress the Berkshire conglomerate from higher commodity prices. It’s not a leap of logic to surmise that Vicki Hollub, CEO of Occidental, has already shared her thoughts on the future of oil.

We’ve underinvested in the physical world, and have been for awhile. Eventually, our appetites will deplete our inventories to the point of concern. Just as some bank execs played fast and loose with their balance sheets, political leaders have done the same with our reserves and the viability of our energy industry. For oil, we can devalue and deemphasize energy security to pander to constituents and environmentalists, but that neglect will have increasing repercussions as underinvestment follows. Just as Buffett plays off of people’s irrationality in business, he’s realistic about reality, and he’s seeing the risk. While not historically great businesses, these commodity purveyors, purchased cheap enough and into a rising inflationary environment can be priceless. At worst they’re a hedge, and at best, they’re an appreciating asset.

So the third insight?

Think inflation? Time to get real . . . assets.

Last, but not least. Let’s talk energy further.

Hang on, no analysis needed . . . just re-read some of these thoughts . . .

“$20 Trillion is way too low.”

“You will be producing more oil in five years from now, or about the same amount.”

“If you spent trillions of dollars out, you’d still be needing it.”

“You can’t change the world that fast.”

Yup.

So the fourth insight?

Energy transition? It may never happen.

There’s many more insights to be gleamed from Buffett and Greg Abel’s interview on CNBC with Becky Quick, and we’d encourage readers to peruse the transcript. For us, it was a great way to reset after finishing up our quarterly letter. The perspective is exceedingly helpful in an uncertain world.

So when in doubt? Just ask . . . WWBD?

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.