Iran: The Beatings Will Continue, Until Oil Prices Improve

March 5, 2026

Iran . . .

Iran’s one of those topics where we have a lot of opinions about, but very few convictions in with the uncertainty so high.

As the US engages in “offensive operations” against the country, we’ve just started Day 6 of this conflict. Iran’s now effectively blocked the Strait of Hormuz, a small maritime chokepoint in which 20% of the world’s crude oil flows. It’s not only narrow, but fairly shallow in certain areas, so even in the best of times, it requires careful coordination when moving VLCC behemoths in/out of the Persian Gulf.

Lob a few drones at anything that transits there and you effectively plug it. Lest you’re a daring owner cut from the same cloth as Jack Sparrow and you run your tankers at night with your AIS turned off to break the blockade, most will stay away. Still that’s a lot of risk to take, and for most multinational shipping companies, one they’re unwilling to take even if you give them adequate insurance coverage. Sure the US can backstop shipping insurance all it wants, but will they also cover the lost income if an Iranian drone sinks a ship? Unlikely. Will it cover the replacement value or the ship, or the fair market value of the ship? Who knows.

So thus the strait likely stays closed unless international pressure forces Iran to reopen it, well really the IRGC. For now though, that pressure won't come from Iran’s largest customer, China, because guess who’s still allowed to transit the passageway? That’s right, good ‘ole Xi Jinping, and everyday this “operation” continues, Xi gains increasing clout. Besides China, no one else is willing to transact with Iran today, and later when the country needs to start rebuilding, guess who’s at the front of the line for those contracts. So yeah, the strait’s closed . . . but not to China.

Shutting-in Supplies

Oil prices have vaulted though due to all these shenanigans. Climbing from $73/barrel on Friday to today’s $84/barrel.

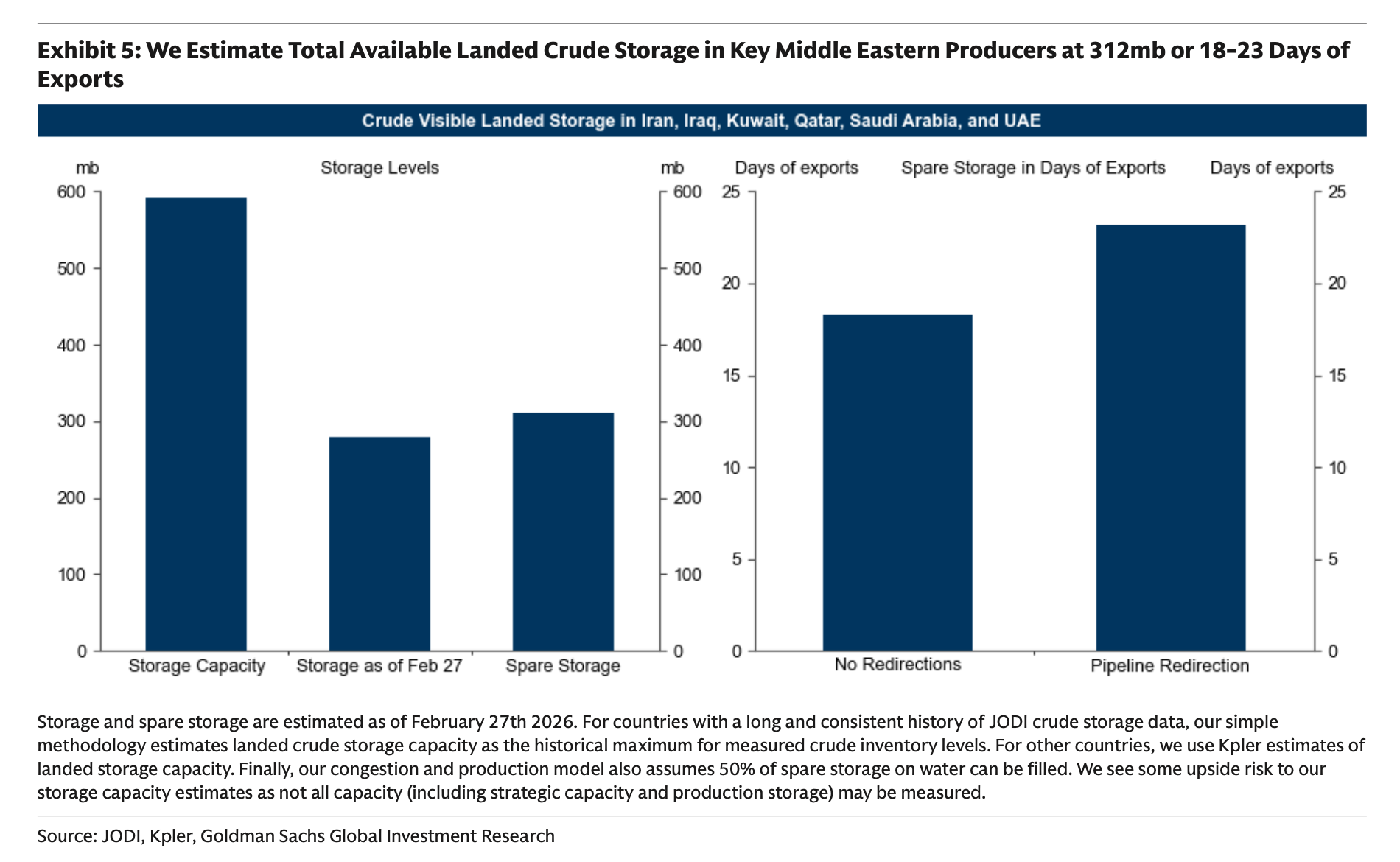

That’s 15%, give or take, and it’s just the beginning if the situation persists. How high really depends on how long this goes. The longer the strait is closed, the more storage facilities in Saudi Arabia, Iraq, Kuwait, and the UAE fill-up. Once those tanks are filled, then production shut-ins start to happen.

Iraq has already announced a cut to oil production of nearly 1.5m bpd. If that doesn’t sound like much, Iraq produces 4M bpd, so yeah, that’s plenty. It’s inevitable though because spare storage is finite at ~300M barrels in the region. So by 2-3 weeks time, we’ll fill those puppies to the brim, and then force the fields to idle.

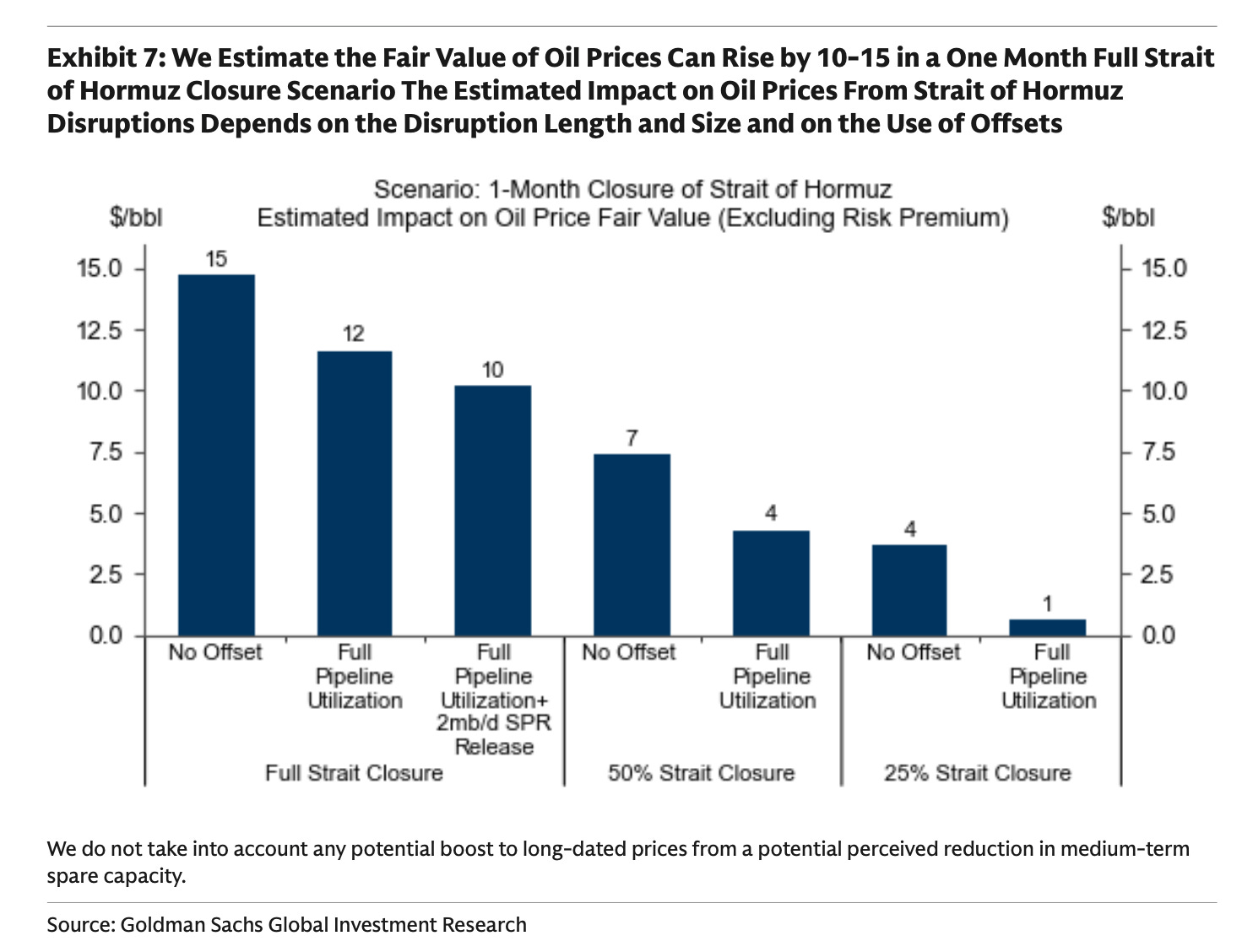

In turn, that shut-in translates to an increase to oil prices by $10 to $15/barrel for the month, so think $85-90/barrel for Brent. In the short-run, it’ll almost certainly exceed that if we cross longer than 10 days . . . and we’re nearly halfway there.

The market though (as represented by the S&P 500) has been fairly nonchalant.

It’s barely down in the past 5 days, and it’s almost certainly looking at a TACO scenario whereby Trump Always Chickens Out. It’s willing to overlook the near-term rise in oil prices (we are after all “glutted with oil”), and the temporary bump will not only prove fleeting, but even more encouraging is that once the Iranian populace revolts against the IRGC, we could see oil prices decline even more as the vast production potential of that country is unleashed.

Never mind the political uncertainty a toppled IRGC will lead to, or the sectarian issues that’s deeply embedded in that region. No doubt 100K former radicalized IRGC members will blend quietly back into a new cosmopolitan Tehranian life, and all will be well.

Call us doubtful.

Still, this is the path we’re on. Despite the rhetoric of the administration, this endeavor doesn’t appear to be fully thought through. The administration is likely counting on a quick capitulation. Flush off the success of Venezuela, the surprise surgical strikes in Iran should bring about a regime change as protesters reappear. Our good deed in Venezuela worked, so no doubt it’ll work in Iran. Moreover, oil prices shouldn’t rise too much right? We have nearly 4M bpd of spare capacity AND a super-glut of inventories, so the oil market will stay calm. We firmly believe that’s what they believe, and as you know, we firmly believe that it’s wrong.

So based on these faulty assumptions, and limited past success, we’re off to the races in wiping out the IRGC leadership. It’s regime change we’re after, so it’s existential for the IRGC. So surely, they’ll go quietly into the night.

Yeah right. There’s no way. Iran will continue to lash out at its neighbors and ratchet the pressure on the global economy. It certainly knows that the longer it can last, the better it will survive. The US can only continue its operational tempo for so long. Given the sheer distance and the vast size of Iran (i.e., larger than Alaska, and more than twice the size of Texas), the ability to project air power is finite as men and machines invariably wear down. There’s also a plethora of hiding places in the mountains for Iran’s weapons, and they’ve no doubt become adept at shooting and scooting.

So bear down and survive. Iran knows there’s two things that can end this conflict . . . the market and munitions.

Munitions & Markets

The market’s patience, and dare we say complacency, is limited. Continue to block the strait and eventually oil prices will leap so high that demand destruction (i.e., a recession) must follow. It also isn’t just the Strait of Hormuz that’s the issue, Iran’s attacks on lightly defended refinery complexes in the region also shuts in production. Saudi’s Ras Tuna’s refinery (550K bpd of processing), Kuwait’s Ahmadi refinery, Qatar’s Ras Laffan LNG complex, and Bahrain Petroleum Company’s Ma’ameer refinery (400K bpd) have all been targeted. Attacks and repairs halt production, which increases the need to reroute or store the incoming crude. Damage enough infrastructure and you’ll force producers to shut-in production. Translation - everything and anything is up for grabs, my pain is your pain.

The cumulative impact is real. The longer the conflict goes, the more the pressure grows. If energy prices vault as a % of GDP (as it did in 2022), it will cascade the market.

Trump ties his personal and presidential success to the stock market, and if the real time report card starts to slide, then the odds of a TACO Tuesday ramps higher. What isn’t clear though is what happens after. Can he TACO if the IRGC remains intact. Can he even TACO at all?

He can certainly declare “Mission Accomplished,” but like the ill-fated Bush declaration, the knock-on effects of an even more dangerous and now betrayed Iran grows. Good luck negotiating with that, and we all better tighten our borders.

Munitions is the second issue. Eventually, the US will run low on stocks (both offensive and defensive weapons). In fact it already is.

It’s started shifting missiles from Asia to the Middle East, which tells you what inventories are really like for the US and its allies. Missile stocks are quickly dwindling given the sheer number of threats. Just today Bahrain intercepted 75 missiles and 123 drones in a refinery attack, but can it do the same the next time? Even after downing so many weapon systems, the refinery was still struck. What of its other neighbors, or even more lightly defended targets? As inventories fall, drones and ballistic missiles will start getting through with increasing frequency despite Iran’s lower launch rates. So it’s a race between finding and destroying the launchers vs. the rate at which defensive missiles deplete.

Tick Tock

Regardless of what happens, there’s a ticking clock here. The longer this goes on, the more pressure the US will face to cease hostilities and look for an offramp. Product prices (i.e., diesel, gas, jet fuel, etc.) are already roofing as refineries are taken offline (either because of lack of crude supplies or refinery attacks), and as prices climb at the pump, political support will degrade further. Inflation was already one of the largest issues in the upcoming midterm elections, and that was before energy prices climbed higher.

For Iran? The calculus is much simpler. Just-in-time refinery operations worldwide provide little to no resilience for our global energy market. As their attacks persist, as they continue their oil blockade in the strait, even for a short while, the market shock will force the US’s hand. Sure OECD countries and non-OECD countries will likely release supplies from their Strategic Petroleum Reserves (“SPR”) in short order, but if Iran is disrupting even half of the flows in the Strait of Hormuz, the 10M bpd loss will still be quickly felt worldwide.

We’re on Day 6, and thus far this is an energy shock, and one the world is unprepared for if it crystallizes and far too complacent about. So said another way? We think this has to go higher for the economic pain to be real. We have to go risk off before we can dial the risk back. Markets are like people in that they only really change when the cost of something becomes far too great to bear.

$84/barrel today just isn’t there yet, so the beatings will continue . . . until morale and oil prices improve . . . and they likely will.