Iran's Running Out the Clock

May 1, 2026

Week 9 done.

Onto Week 10.

12M bpd of disrupted Hormuz flow in April, and this will likely continue into May as diplomacy looks to be a ways away with uranium enrichment and the Strait of Hormuz (“SoH”) reopening intertwined. It’s difficult to sort out since one provides the leverage for another.

If the US relents and ends its Iranian blockade, that emboldens the Iranians. Similarly, if the Iranians end their SoH blockade that would also dramatically reduce their leverage at the negotiating table.

Uranium enrichment and nuclear development. Will the US be willing to separate this? The US, and the Trump administration specifically, needs a “tougher” deal than the JCPOA that he exited from. Otherwise, how could he paint this as a victory? In contrast, the Iranians smell weakness. The longer the SoH remains blocked, the more leverage it has to not only take control of the SoH long-term, but also retain its nuclear development program. The SoH becomes “the nuke” to be negotiated for, and the “actual nukes” take a secondary position.

Will the Iranians be willing to cede nuclear development for 10, 15, 20 years to allow Trump to declare victory? That’s doubtful as the current strategy is working well. Though the blockade has dropped Iranian exports to a measly 500K bpd, and the country is suffering economically, history has proven that they can weather an extended storm (i.e., see prior sanctions with Trump and COVID).

Ballistic missile development? No word on this of late. Too complicated given the core issues above, which means Iran gets to keep it.

So effectively we’re left with a stalemate on the panoply of issues, and that stalemate means we bleed.

Bleeding 12M bpd that is, that’s the deficit. That’s the amount of crude and products that’s not flowing because of the war.

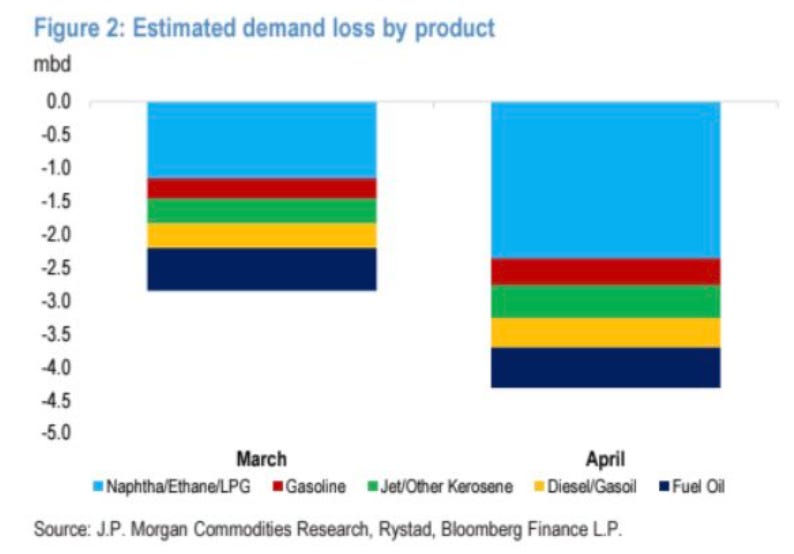

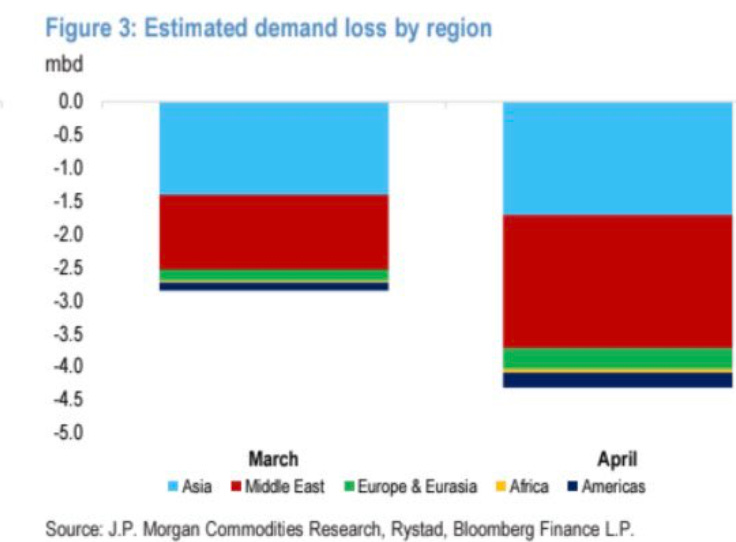

Right off the bat we’re already starting to see demand destruction. Prices at $100/bbl oil aren’t so high that they should already kill demand, but it’s happening because of the actual absence of molecules. There just isn’t any supply for some frontier Asian countries. Hence demand is down. Middle East demand is also obviously down, and not hard to see why when missiles and drones fly.

So reduce that 12M bpd by 3M bpd of demand loss, and we should see somewhere in the neighborhood of 9-10M bpd of inventory draws. Well are we?

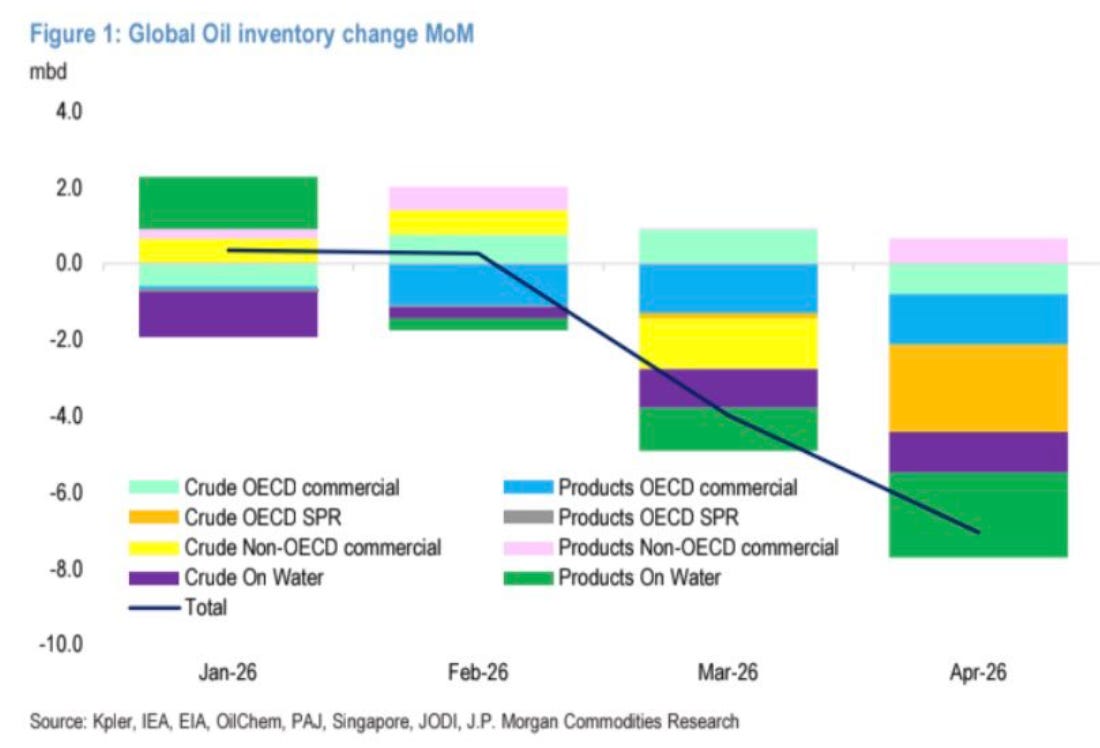

Thus far, we’re only seeing around 7M bpd.

In total, visible inventories appear to be falling about 6-7M bpd. This includes about 3M bpd of SPR release.

To reiterate, the above is “visible” inventories. What’s tougher to track though is non-visible, non-OECD products inventory and we think that’s the difference. Once that bleeds down, then visible inventories should draw slightly higher, or further demand destruction in non-OECD countries will occur. Non-OECD countries include China, India, Brazil, Argentina and Russia, so these are material in every sense.

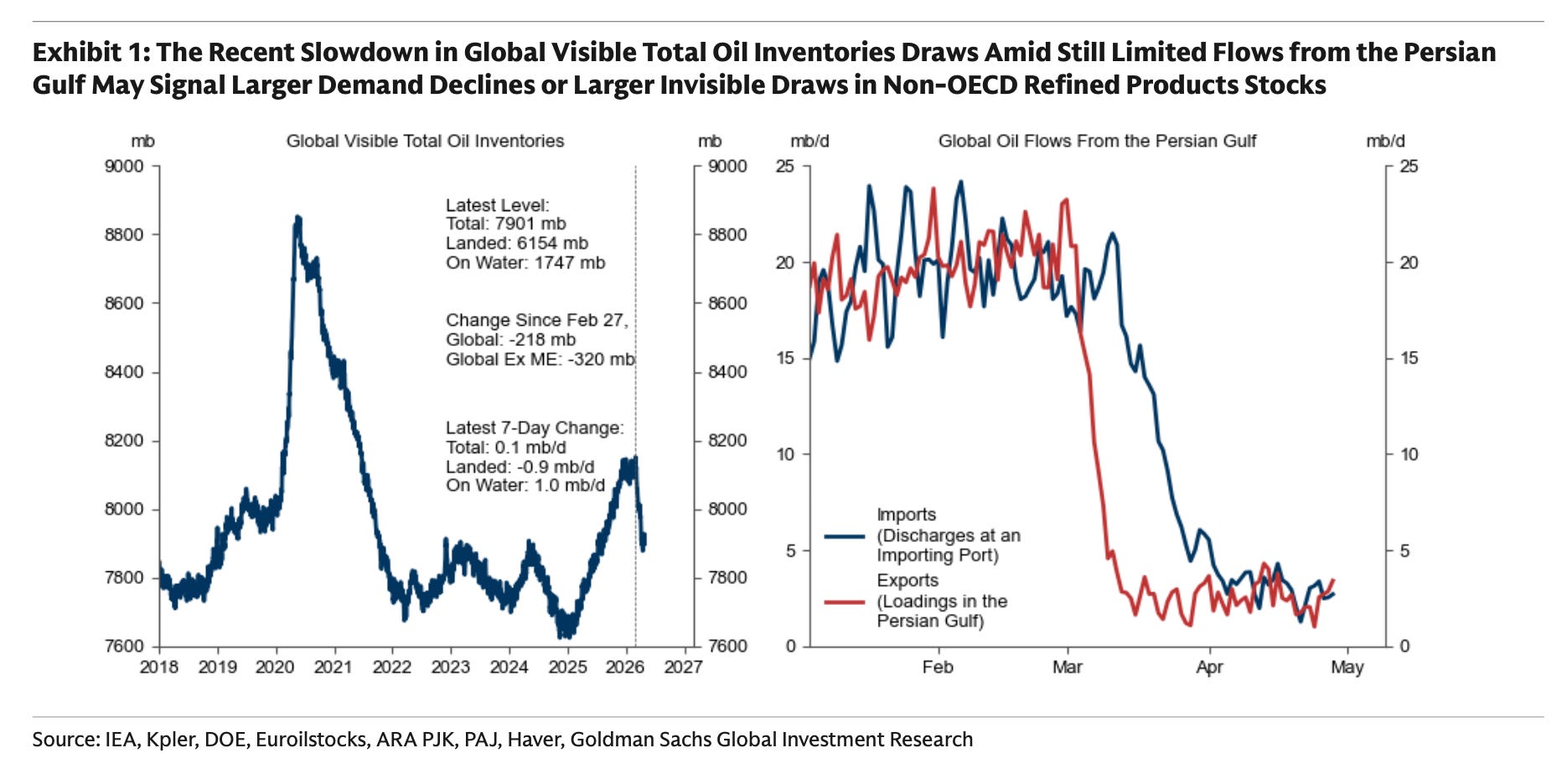

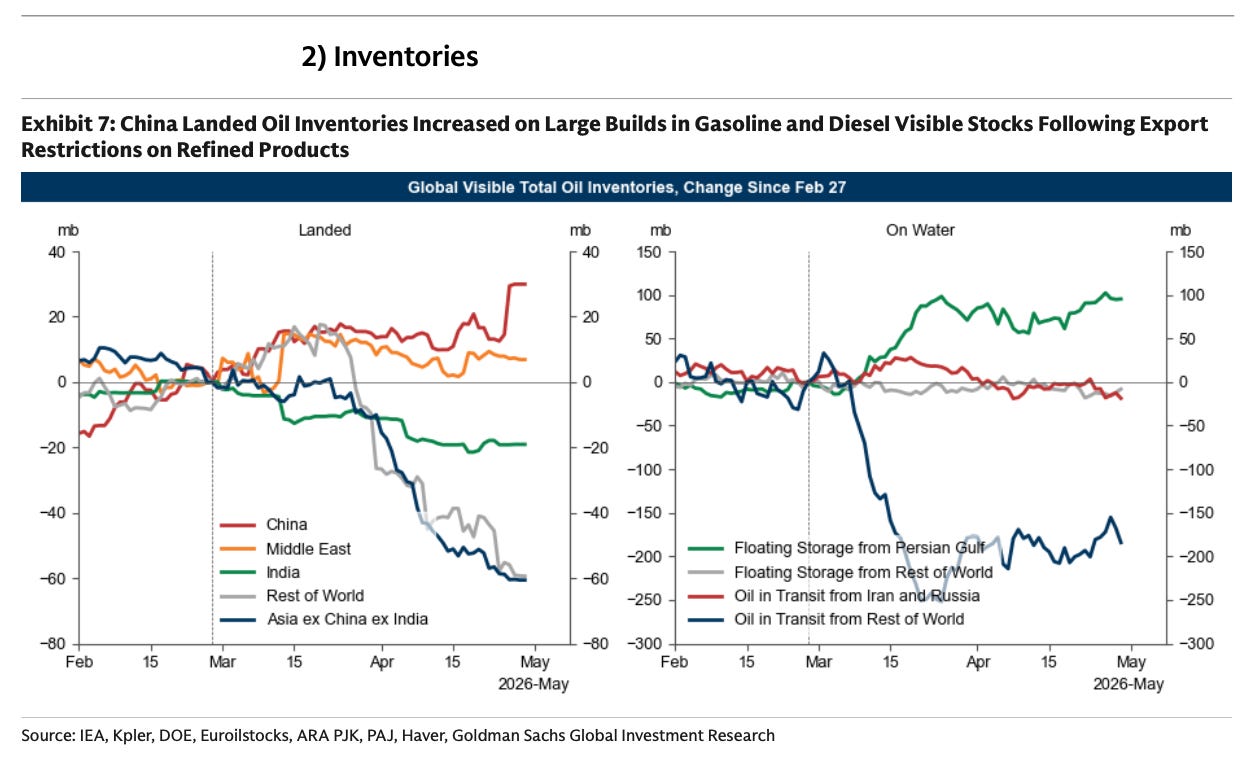

Though the charts above are from JP Morgan, if we take a peek at Goldman Sachs’ chart, we can see similar findings.

Goldman though pegs demand destruction at 2.5M bpd vs. JP Morgan’s 3.5M bpd, so split the difference at around 3M bpd, but whatever the demand destruction we settle on for now, the thrust of the argument is about the same. We’re currently drawing around 6-7M bpd of visible stock, and some other portion that we can’t see.

Unlike COVID, this energy crisis will have a delayed impact. Whereas COVID saw immediate demand destruction, supplies didn’t immediately stop, so inventories ballooned. The Iranian conflict has the opposite impact as oil-on-water still flowed for a few weeks as the last ships arrived at their destination. Those supplies have finally tapered off, so the air pocket has firmly arrived at the far flung ports.

For the foreseeable future, we’ll see visible inventories fall further as consumers/refiners pull on all available stores. In turn, prices will rise to further curtail demand as the bidding war progresses and the stalemate continues.

Oil analysts had predicted the sequence to move from East to West. So has the first to draw was Asian inventories? Yup.

Next up, Europe, and finally, the farthest barrels in the West (US) will bear the final brunt . . . or so we thought.

Well guess what?

Brunt? Meet backside.

It’s just getting started, and we’ll see the visible side fully reflect this crisis.

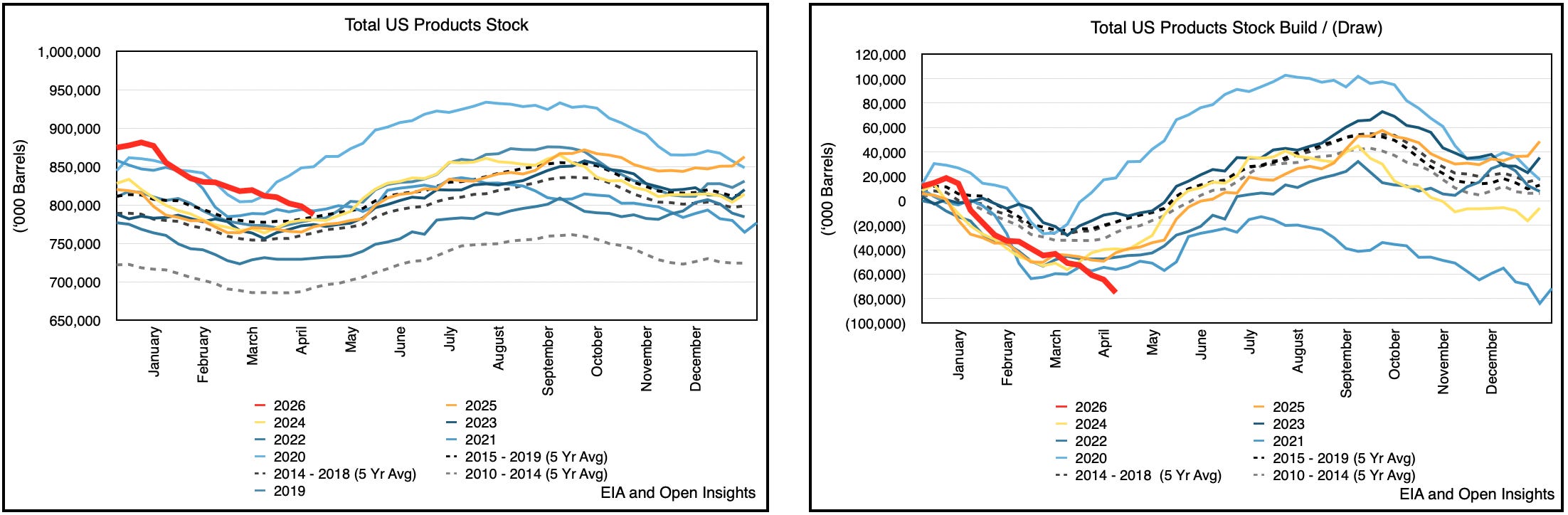

US crude/product stocks are the most visible inventories to track. The Energy Information Administration (“EIA”) provides timely and comprehensive data, and for the week of April 24th, it reported a nearly 23M draw on inventories. If you’ve any doubt, this is a precipitous fall during the “slow season,” one where we typically try to build inventories for the summer high demand season. Products (i.e., gasoline, diesel, jet fuel) are drawing the fastest.

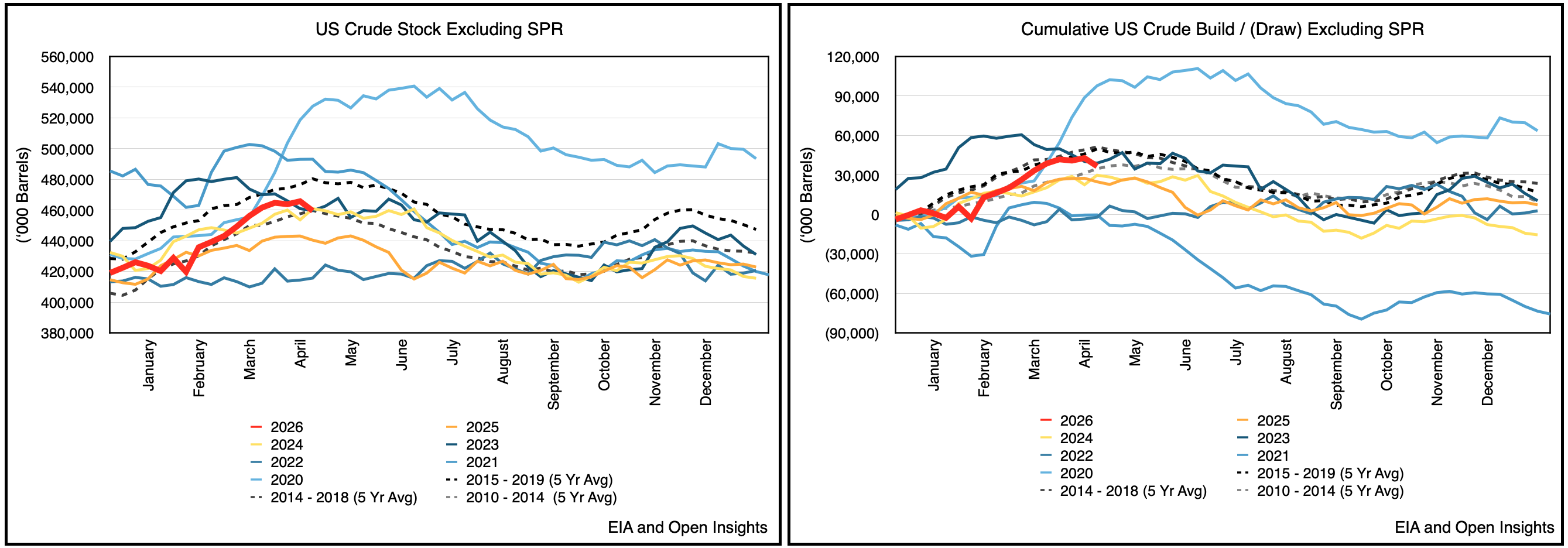

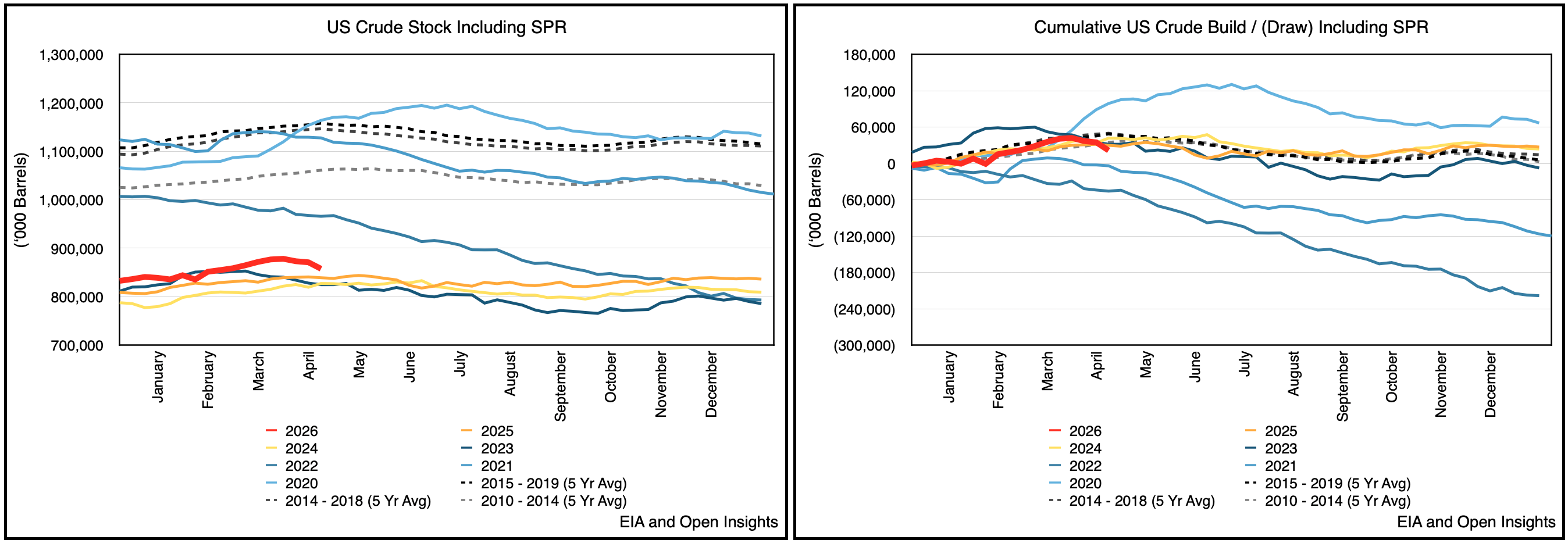

Crude draws are starting as well. Below are two graphs (a crude chart excluding SPR inventories (i.e., US commercial crude stock), and a second crude chart including SPR (i.e., total US crude stock). Commercial inventories are being supported by US SPR releases, but despite this, commercial crude inventories are still falling (i.e., the SPR release helps mitigate not eliminate the inventory declines).

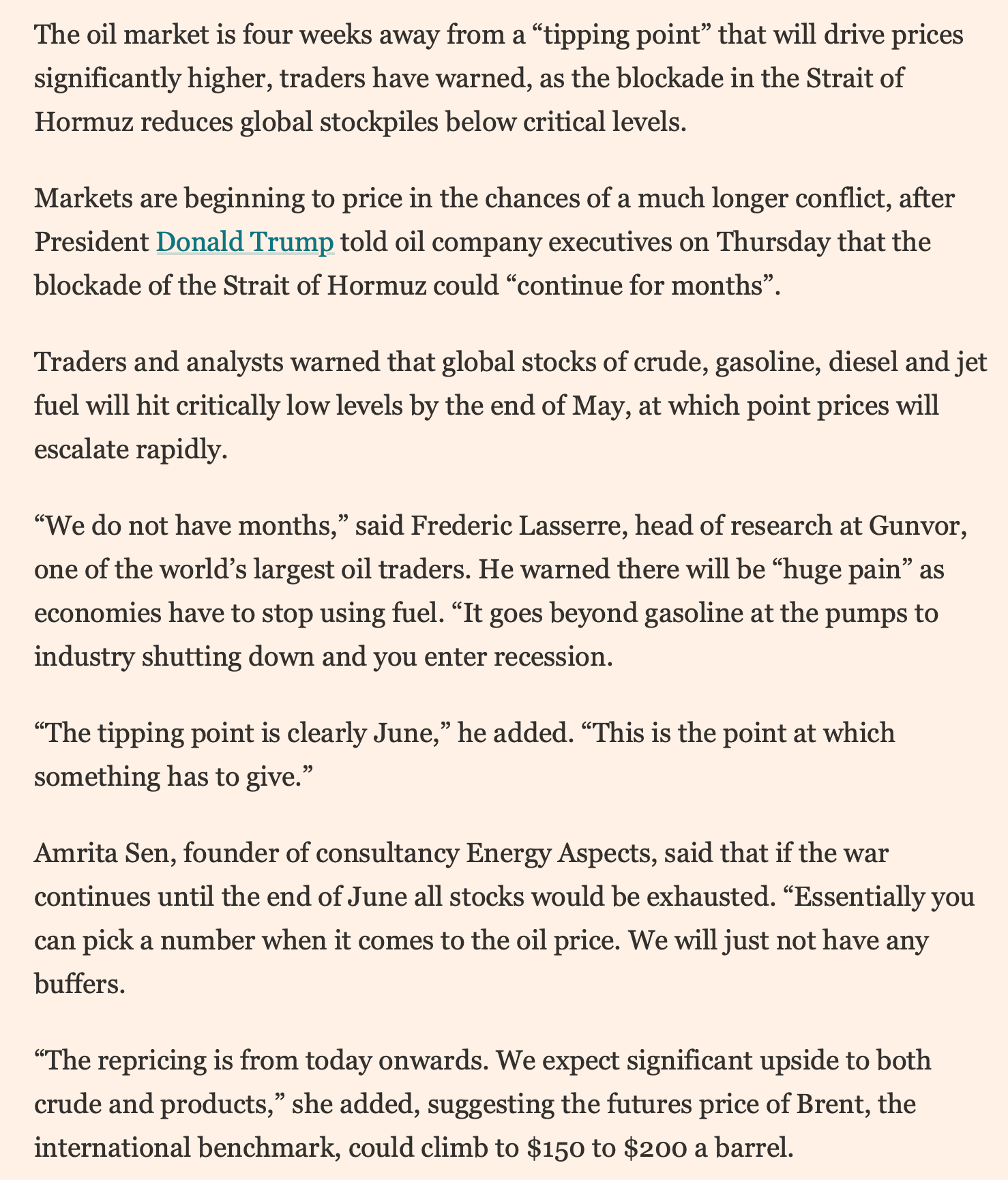

We’re expecting further fireworks in the weeks to come, especially as May starts to kick-off the higher demand summer season. Just take a guess as to what prices will do then. Again, remember, even if the SoH were to reopen today, we’ll have another 2 months of logistics sorting itself out, so another 2 months of draws.

For the time being we’re at a stalemate. While the US and its allies can continue to manipulate the paper market to suppress the prices of oil, the inventory shortage will inevitably translate to price. (Say what you will about Zerohedge, but this is very likely to be true given the movement in oil prices yesterday with little headlines).

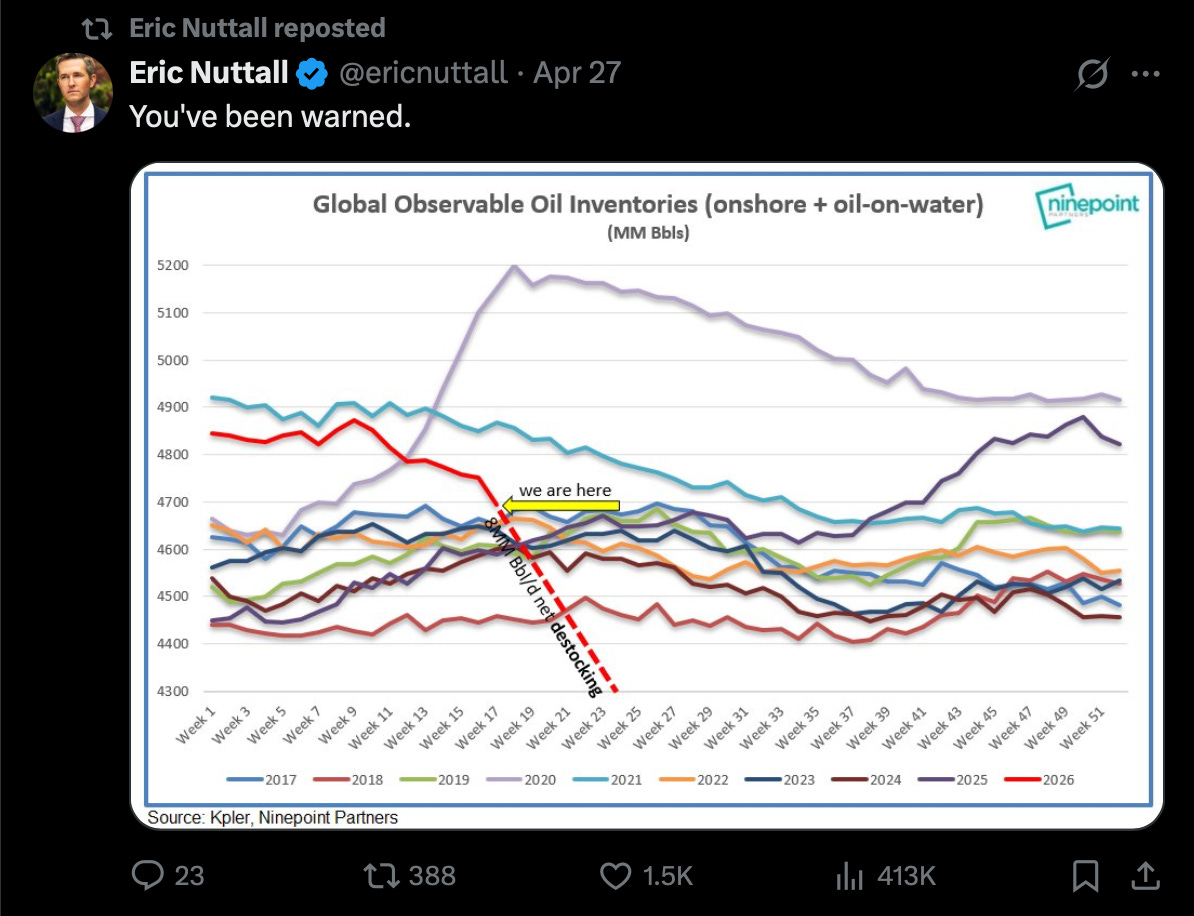

What’s an investor to do? Well, despite the above, we think Eric Nuttall’s tweet about crude inventories is ultimately the most fitting.

Barrels are draining and barrels will continue to drain as the stalemate continues. Every additional day the SoH remains closed, means Iran gains further leverage in any negotiation. In truth though, it effectively needs to hold out for one more month (here’s a Financial Times piece on the timeline).

It’s why we think the next step will likely be another US attack on Iran. What can’t be achieved at the negotiating table will have to be gained on the war table. The US has little leverage here other than blustering and bellowing for Iran to capitulate, but Trump’s desire for a deal is so intense and the potential impact to the global economy so unfathomable that Iran knows the longer it waits, the better the deal.

Unfortunately, a win for Iran is a loss for Trump, and hence, the chasm between their positions can’t be easily bridged unless one of them loses another chess piece. The clock favors the Iranians, and they know it.

As the weeks pass, something has to give, and Iran won’t unless kinetic action forces it to. After which, the table will be overturned, and everyone will pick up the pieces to see where things stand in the sand.

Tick tock. Tick tock.

Week 10 here we come.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

Brilliantly written! The tail risk is how Iran will retaliate if the US resumes its strike!!!

The point missing from this excellent piece is the real reason why we are over there fighting - to restore / defend the Petrodollar system and establish a counterweight to China's hold on rare earth supplies. The missile and uranium questions are much lower priorities. The big worry is whether we can continue to finance our enormous debt if we lose the demand for treasuries fostered by the Petrodollar trade