It's All About That Base, 'Bout That Base . . . All Trouble.

May 27, 2022

I can’t sleep. Not because I don’t want to. Something bothers me; it’s a feeling. It’s the same nagging feeling I had during the COVID pandemic . . . you need to get this right.

It’s the same nagging feeling in 2021 with inflation . . . you need to get this right.

It’s the same feeling now . . . you need to get this right.

What’s this?

This.

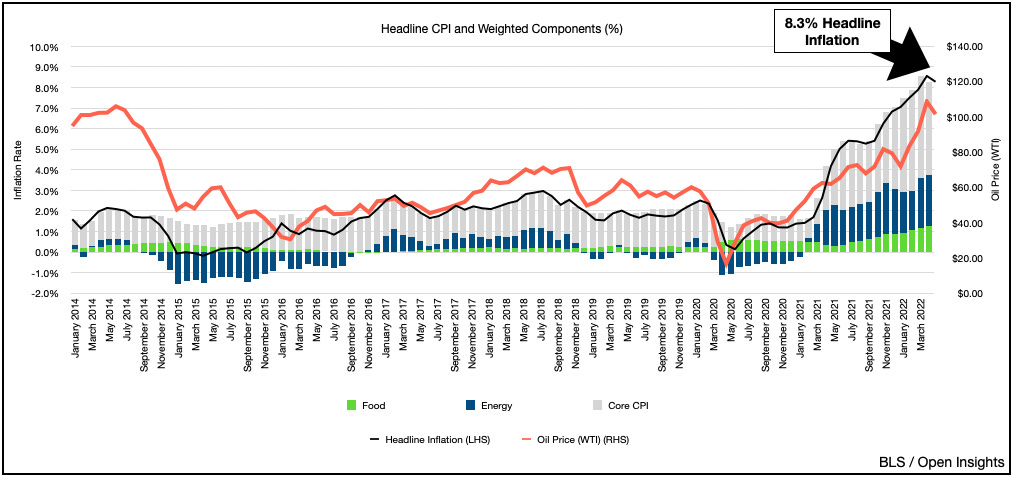

Inflation. Specifically, where is it going? We need to get this right because this, above all else will drive your outlook on almost every investment in the coming years. As we’ve said before, interest rates are gravity, and it compensates you for two things, inflation and risk of loss. If you figure out inflation, then you have a good chance of figuring out gravity. Gravity that determines how high or low asset prices can rise/fall. Lower gravity (i.e., lower interest rates)? Watch home prices soar. Higher gravity? Watch them sink.

So inflation. What’s the trajectory? How rapidly does it increase/decrease? Does it stay flat? What’s driving this chart, how do central bankers and political react to the change? How do we react as consumers? How do investors react? How do we?

We’re sleep deprived because it’s all nagging at us. This notion in the market that the Fed can achieve a soft landing. It can tamp down inflation without nudging our economy into a recession or shoving it into something worse. Sure there’s plenty of doubters, people who can eloquently articulate why that’s an almost impossible task, but the notion is out there. Inflation will calm down, interest rates won’t need to rise further, and growth stocks and asset prices will regain their highs. It’s part reason (as one could make a plausible argument for it), part hopium (because who really wants a rough economy after all), and part possibility (stuff happens). Still, what’s triggering our insomnia?

Well this. Maslow’s pyramid . . .

While everyone’s concerned about whether the Federal Reserve will hike interest rates beyond neutral, we can’t help but wonder if we’re looking at the same things. Hiking rates and quantitative tightening is addressing “the cost of money” issue. It’s making “money” (well credit really, but we’re using the vernacular) more expensive. Make money less available and more expensive, you tamp down demand.

Still . . . that base. As the famed economist/pop-artist Meghan Trainor sings . . . It’s all about that Base.

While everyone’s worried about the top of the pyramid, we’re worried about the base (i.e., food, energy, etc.), the very basic things we need to survive. It’s something we addressed after assessing Russia’s invasion of Ukraine . . .

So we anticipated it, but anticipation is one thing, watching it come to fruition is a whole ‘nutha.

The hoarding? It’s begun.

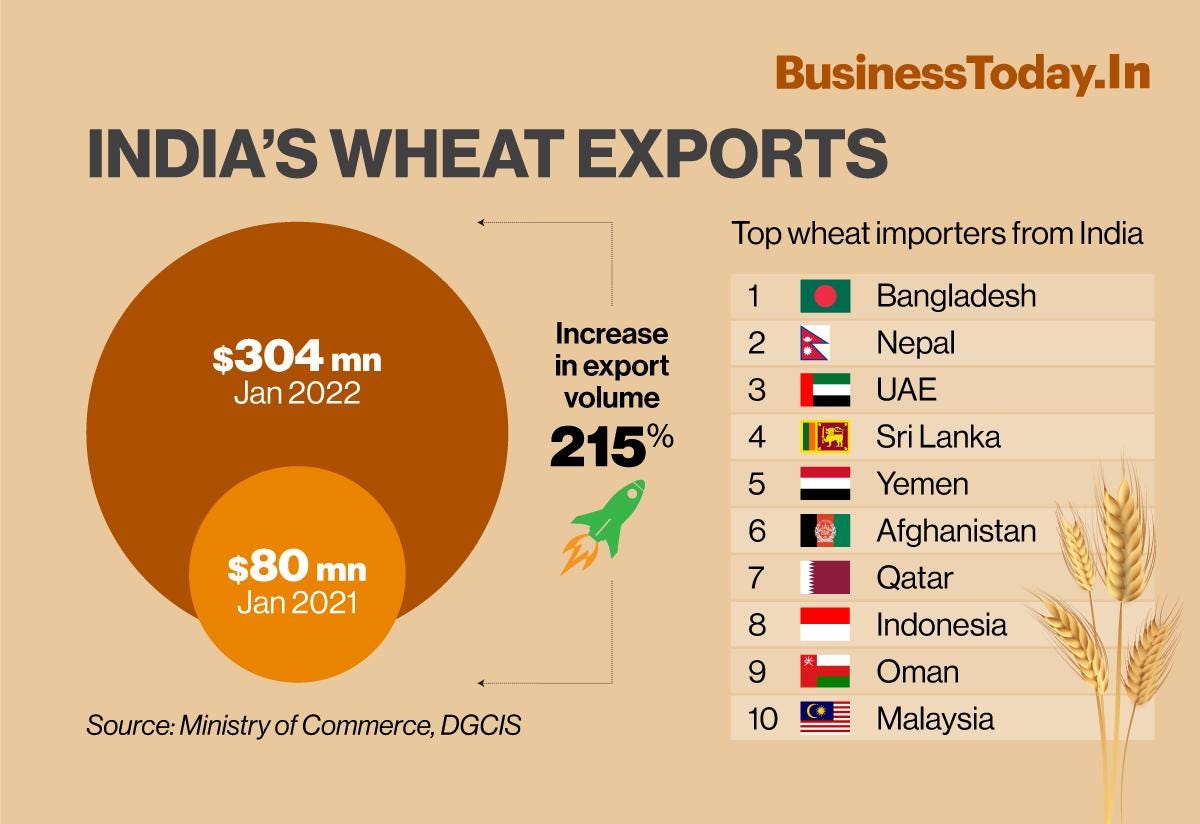

What’s the big deal some will say? Let’s just take India’s ban. India is the second largest producer of wheat in the world, ranking right after #1 China and before #3 Russia. Ukraine is #8. Production vs. exports are different, and when we look at exports, the deck gets shuffled a bit, India is a much smaller exporter.

Still we’re talking about the fringe here. The fringe is where many in the world live. People in some of the poorest areas of the world, located in the Middle East, Asia, and Africa. We’ve christened these areas “emerging markets,” but they’re really places where people are engaged in subsistence living. Take a look at who India exports to . . .

Bangladesh receives 56% of its wheat from India. It’s a country with 165M people (half the population of the US) who earn ~$2,000 a year in per capita GDP, a country that will now be forced to source a portion of its wheat from the global market at much higher prices.

India understands their dilemma, it’s sad stuff kid, but we have 1.3B people with an average per capita GDP of $1,900 a year. So tough cookies . . . we win. Well, more like . . . we hoard. That’s what this is. This is hoarding.

It’s hoarding by 1.3B people out of 7.7B people in the world. Ponder that for a second, 18% of the global population have begun to hoard. Well more than that because these are the recent export bans and their respective countries via CNBC.

So the ripples begin. Well they’ve already started much earlier, but we’re beginning to see them on the surface, and it’s not just food, but energy as well, as we’ve detailed before.

Of course the US is in a much better position because of our midwest bread basket and Permian basin (for energy). Our productivity relative to our production size will insulate us from the worst of these price shocks, but we won’t emerge unscathed as the emerging markets start to grab at whatever is available. Right now we still have some inventories, but as we approach harvest season later in the year, we’ll begin to understand the impact of the supply shortfall. USDA projects global wheat and corn production to fall. Fortunately, global rice production will increase, but for all three grains, consumption is projected to be higher, leading to inventory draws. Look we are not food exports nor farmers, but we understand commodity markets and market dynamics. So play this out even a little and you can see the knock-on effects.

Leaders in the emerging markets will almost assuredly increase subsidies for their constituents in a bid to maintain political power and stave off riots (if not hunger). Whether they will succeed or not depends largely on whether they’ll be able to acquire the food stuffs/commodities in an increasingly aggressive/expensive global market. We fully expect a food and energy shortage to have a . . . . let’s call it a deleterious . . . effect on the emerging market economies, significantly weakening growth and currencies.

All of this perniciously feeds into more local inflation, as many commodities are priced in US dollars (“USD”). Investors seeing the global instability, riots, and political turmoil, flee towards safety, again reinforcing the USD. Ironically, this will help the US offset some of its inflationary issues as a stronger USD helps it “export” its own inflation problems when it “imports” cheaper things. US companies, however, with material international exposure will face headwinds as economies slow and the weakening local currency, when translated back to USD for reporting purposes, decreases earnings. Those decreased earnings could impact the still high stock multiples that some of these companies trade on. That’s on fundamentals, and we’ve not yet even discussed what a contracting and increasingly turbulent world/global economy would do to market sentiment.

Amidst the instability, China will also be stimulating and subsidizing should food/energy stocks dwindle. As we anticipated, it’s about to go full Red Bull on its economy.

Just yesterday, the central government held a widely attended and reported meeting with 100,000 officials to discuss the economy. Per CNN

“The unexpected video teleconference by the State Council was attended by officials across provincial, city and council levels, according to a report in the government-owned Global Times. High-ranking Chinese officials were also present, including Premier Li Keqiang, who urged authorities to take action in sustaining jobs and reducing unemployment.”

So expect the juice, expect consumption to rise. Yet, on the currency side, as China stimulates, but the US tightens, will the RMB further weaken against the USD? Likely, but given that the RMB’s exchange rate is fixed (okay “measured” against a basket of 13 other currencies), it’s hard to say. We’re not sure, or at least right now.

So you see? The ripples are increasing. We believe two of the most important commodities, food and energy, will become increasingly scarce as we head into the year end, and that will have larger repercussions on the global market than many anticipate.

While the market is worried about the cost of money, we’re worried about the things money can’t even buy. We’re worried about the base.

Meghan is right.

. . . it’s All about That Base, ‘bout that Base . . . all Trouble.

Please hit the “like” button below if you enjoyed reading the article, thank you.

I get your point and you are probably, i guess, right. Whats more interesting, or frightening, to me is that we are looking at the big picture and not the details. For years everyone was talking OIL and GAS. Now everyone is talking about Refineries (from OIL) and fertilizer (from GAS).

So im more curious about the details that we will uncover in the coming months, possibly years. One cant yet fathom what exactly we will see, because "Energy" and "Food" are really just so general, but the devil is in the details. Thanks for writing !

Any thoughts on the sizable increase in GDP/capita of EM nations vs say the 2010-2014 period and their ability to absorb inflationary pressure? USD is the elephant in the room still but could see energy demand stay fairly healthy especially with if China goes full stimulus.