Mind the Gap, the $6,000 Gap

June 15, 2024

It’s ritualistic. The timing of these economic data releases. Like oil data, the numbers hit at different times of the month, and the market swarms all over them, debates them, and trades around them. Like oil data, they’re never precise. They’re just models subject to interpretation. Sometimes though, if you grab enough of them, you can finally triangulate a few things. What’re we talking about?

The $6,000 a year gap.

Let’s explain.

The US Department of Commerce, specifically the Bureau of Economic Analysis (“BEA”), keeps track of many of our macroeconomic and industry statistics. Have a question about US GDP and its details? Just ask the BEA. Data galore that economists, market watchers and Bloomberg terminals can slice and dice to their hearts delight.

One thing we’ve been pondering lately is the health of the US consumer, and monthly data for our friend the “Personal Income and Outlay report” just came out. As we can see, Personal Income continues to rise, which is all well and good.

Unfortunately, Personal Consumption Expenditures also continues to keep pace, and when it’s all said and done, the net result is we’re saving very little. Our Personal Savings Rate keeps treading water at 3.6%, a far cry from the 8-9% we saved before.

Translation? We’re spending what we make.

This isn’t a surprise if you’ve been reading what we’ve been writing. That savings rate just hasn’t budged in many months after COVID.

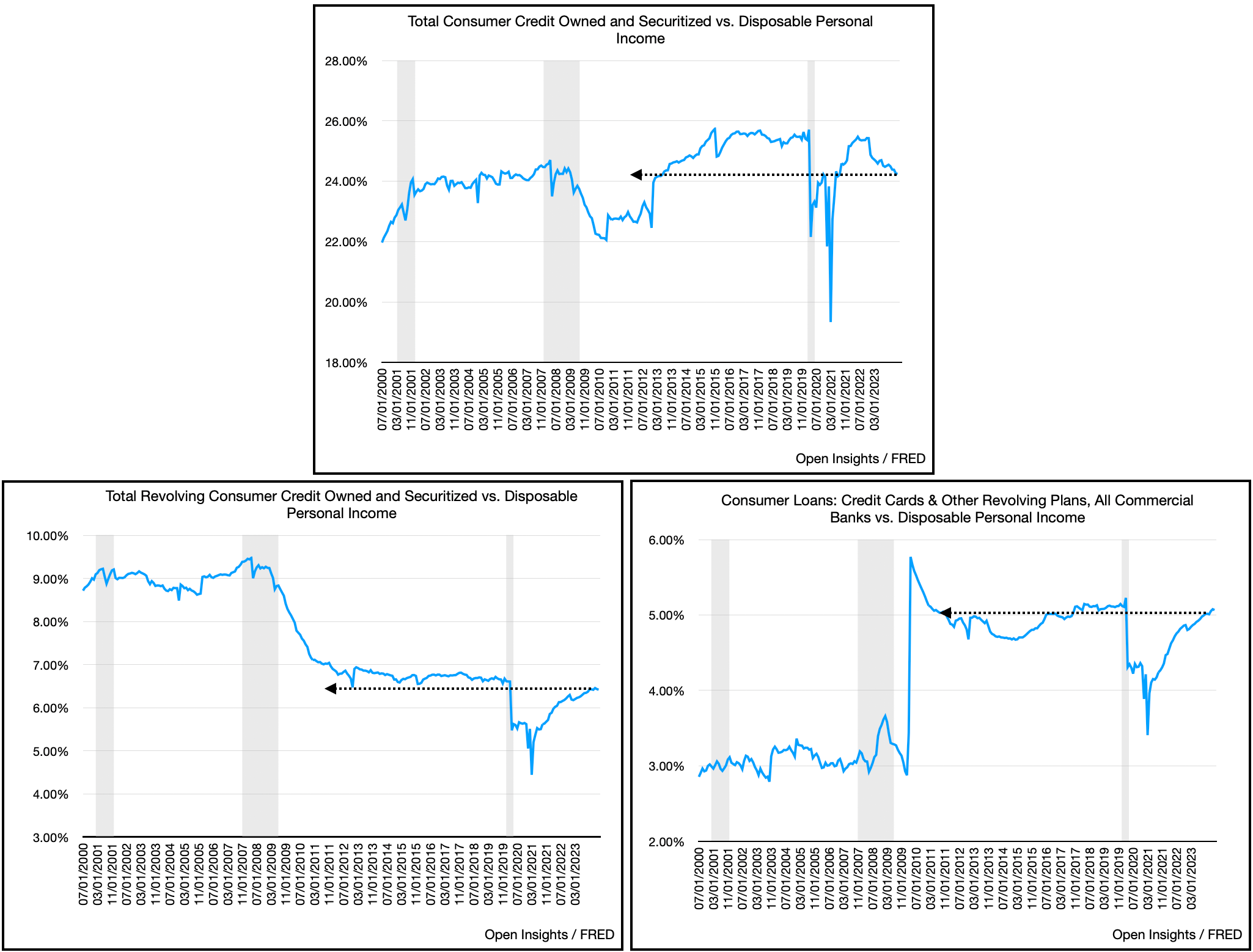

Overall though, the consumer is still relatively healthy, our debt levels are under control as total debt to disposable income percentages are within historical lines.

Interestingly, banks are also more willing to lend, as tightening lending standards are falling, and their willingness to lend have been increasing.

While the numbers above aren’t terribly concerning, dive deeper and there are “green shoots” of darker clouds. Since we’re haphazardly mixing metaphors, we’ll throw in some incongruent data as well. Here’s some troubling trends.

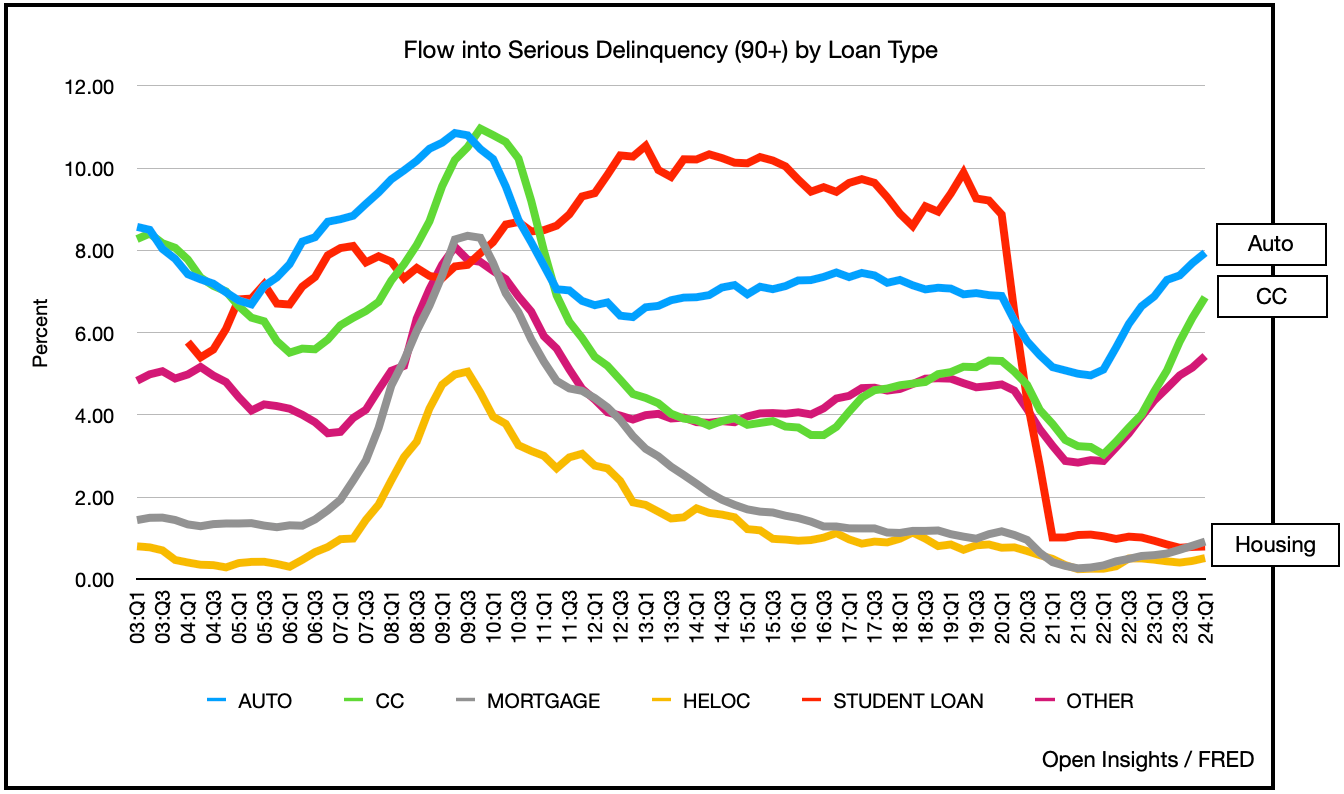

For shorter-term loans, credit cards / automobiles. We’re beginning to see some distress. Think of the next two charts as the “velocity” of delinquency.

Here are loans that are +30 days delinquent.

Here’s +90 days.

See the trend? Notice what’s trending higher? Shorter-duration loans. Auto and credit cards. So while the overall debt balances (relative to our “incomes”) are within reason and the overall delinquency rates are low, as the months tick by, the percentage of delinquencies are beginning to rise, and they’re staying delinquent for longer (read: unlikely to be repaid/recovered).

Different debts though are seeing different outcomes. Look at the delinquency rates for housing (mortgages and HELOCs) and student loans. The federal government’s abatements, forgiveness and suspensions are obviously benefiting student loan borrowers, but what about housing?

That my friends is the tailwind.

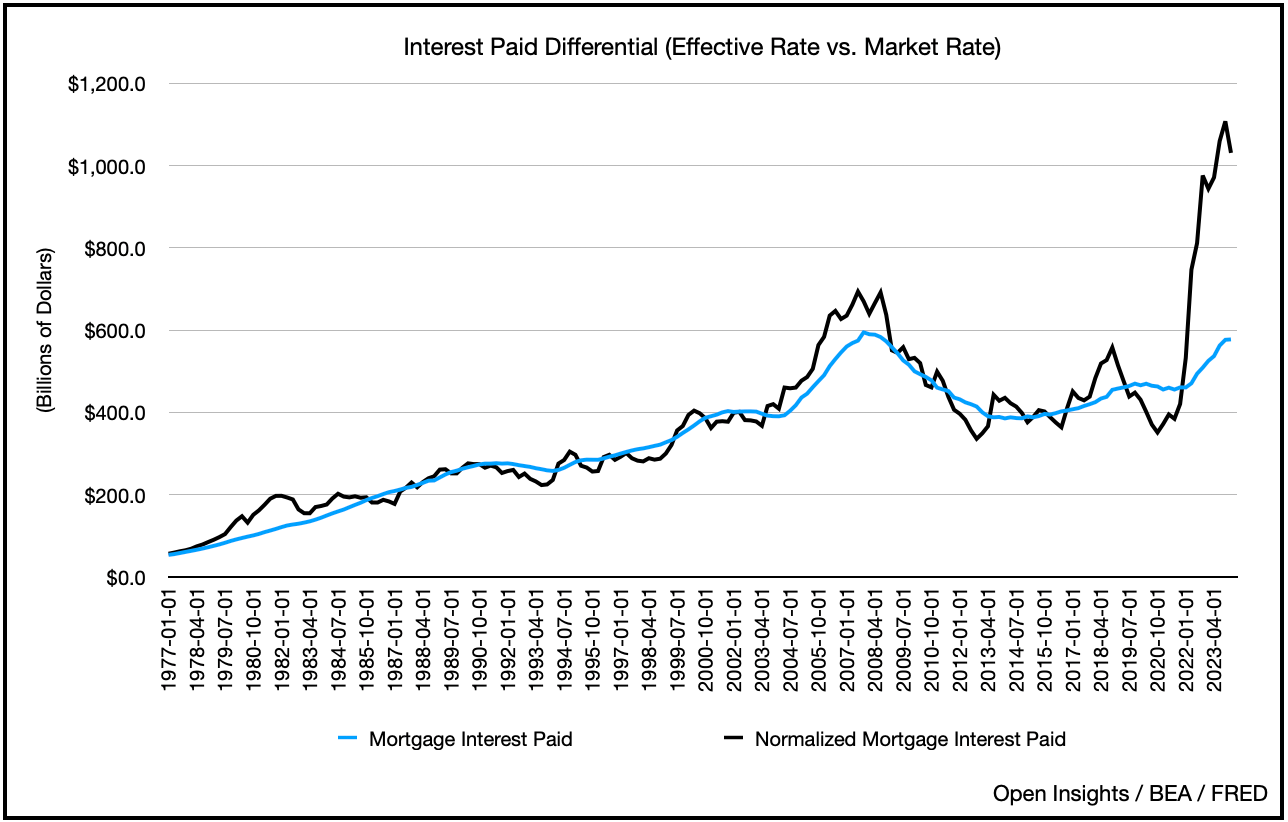

It’s the years of low interest rates that have allowed so many homeowners to refinance and sit tight. Here’s the current “effective interest rate” paid by all homeowners, vs. the current 30 year mortgage rate.

Rates don’t typically “blow-out” as they did during COVID, and the rate differential exacerbated by inflation has really thrown a wrench in our economic machinery (i.e., 6.7% 30 year mortgage rate vs. 3.8% effective rate). Deep analysis we know, but just take a look at how this “gap” translates to actual dollars.

Historically the amount of mortgage interest paid has simply followed the trajectory of interest rates. Higher rates = higher interest expense, and quickly so. If homeowners weren’t locked into their low mortgage rates, we’d see them pay nearly twice as much in interest costs.

Said another way . . . as homeowners, we’re collectively paying ~$500B less in mortgage interest expense that what the current rates would indicate (or how historical averages have played out) (i.e., +$1.1T at 6.7% vs. $~$580B at 3.8%).

For context, go back to our first chart above where we’re saving 3.6% of our income. The $500B of “net interest rate savings” we’re enjoying now because people locked in their mortgages? It equates to nearly 2/3rds of the ~$750B we’re personally saving.

Think about it two other ways. First, there’s about 85M mortgages in the US. Divide that $500B by 85M and you get ~$6,000 per year savings on each mortgage (for simplicity we’ll leave aside the deductibility of those payments, and the fact that you’d need to generate pre-tax dollars to service the debt).

$6,000 isn’t insignificant considering per capita US GDP runs about $75,000 per year. What’s further interesting is that homeowner’s locked into low rates yesteryear are also refusing to move, exacerbating the shortage in housing and sustaining higher housing prices. Normally falling housing prices (because of higher rates) would help counteract the higher interest expenses that came along with higher rates, but not so today. Hence, this round of Fed quantitative tightening hasn’t quite trickled all the way through economically.

Slowly, but surely though we think it’ll be felt. The $6,000 tailwind will eventually unwind and become a headwind. As homes are sold and buyers obtain new mortgages, the real rates will trickle through to this large portion of our economy, dragging on the consumer’s ability to spend. Sure, you can arguably say that one’s person’s expense is another person’s income, but will that interest income necessarily flow through as equally? Do bank profits or government coffers cleanly recirculate/redirect that money back into the economy via higher wages, etc.? Perhaps, but not before the US consumer feels it first when that new mortgage bill arrives.

It’s inevitable though. Thus, it’s a foot race. Interest rates need to come down to relieve the increasing friction of higher mortgages rates, but in order to do so, inflation figures need to decline as well. They just might as balance sheets weaken and the consumers’ ability to spend (i.e., demand) softens.

For now though, understand that if shorter-term loans like credit cards and auto loans are increasingly becoming delinquent, that already tells you a lot about a subset of consumers today. Still, if you then add a headwind of higher interest rates blowing through the housing industry, we may all just experience an economic stumble. The drop in consumer demand could come quickly as we misstep.

So as they say in some countries . . . mind the gap.

The $6,000 gap.

Please hit the “like” button above if you enjoyed reading the article, thank you.