More Cowbells! . . . Oil's Comedy Sketch

April 19, 2024

(Note: We’ve recently released our quarterly letter. If you are an accredited investor and would like a full copy of our letter, feel free to send us a message to confirm your accreditation along with your email address and we can forward it along).

Saturday Night Live, it’s a live comedy show that’s been on NBC since the mid-70s. Typically hosted by a guest host who’s currently the “it” celebrity, the show airs on Saturday, and for certain time zones it’s live. There’s a particular sketch that lives rent free in my mind.

It’s called the “More Cowbell” sketch, and appeared on the show in 2000.

Will Farrell wrote the sketch along with playwright Donnell Campbell. It’s one of SNL’s most famous skits, and it depicts a band called the Blue Oyster Cult recording in a studio. Guest host Christopher Walken plays a music producer, and Ferrell plays a fictional cowbell player Gene Freckle, who overzealously plays his cowbell and annoys his bandmates. Ironically, the producer loves the cowbell sound and hilarity ensues.

"Guess what! I've got a fever, and the only prescription is more cowbell!"

That sketch just makes me smile. A grown man in a too-tight t-shirt banging on a cowbell while his bandmates jam.

Comedy gold.

My brain dug-up this treasure trove of absurdity this week after watching the situation unfold in the Middle East. If you didn’t know already, Iran attacked Israel in a well telegraphed and strategic strike. It was more strategic (i.e., a show of force) vs. tactical (i.e., causing real damage), and after launching over 300 missiles and drones, Iran’s retaliation for Israel’s attack and elimination of IRGC commanders in Damascus was “concluded.” Their words, not mine. All of the drones and cruise missiles were either downed by Israel or coalition air defenses, so what was thunder and fury essentially turned into an Iranian turkey shoot.

Israel, not one to take a slap lightly, retaliated last night, carrying out a missile attack on an Iranian airbase, Syrian radar targets, and targets in Iraq. Though US officials noted that Israel had retaliated, Iran has publicly denied any attack occurred, and Israel has stayed surprisingly quiet. Clearly all parties are attempting to deescalate, and walk back from the brink of war.

Oil prices, which had vaulted higher before the weekend, promptly sold off given how ineffective the Iranian attack was, and the US’ call for Israel to “take the win” and exercise restraint. Though Israel ignored the “letter” of that ask, their subsequent counter-attack yesterday proved they understood the “spirit” of the request.

For oil investors, the geopolitical premium faded. For all the bluster, prices have retreated by nearly $5/barrel from the highs notched on Friday.

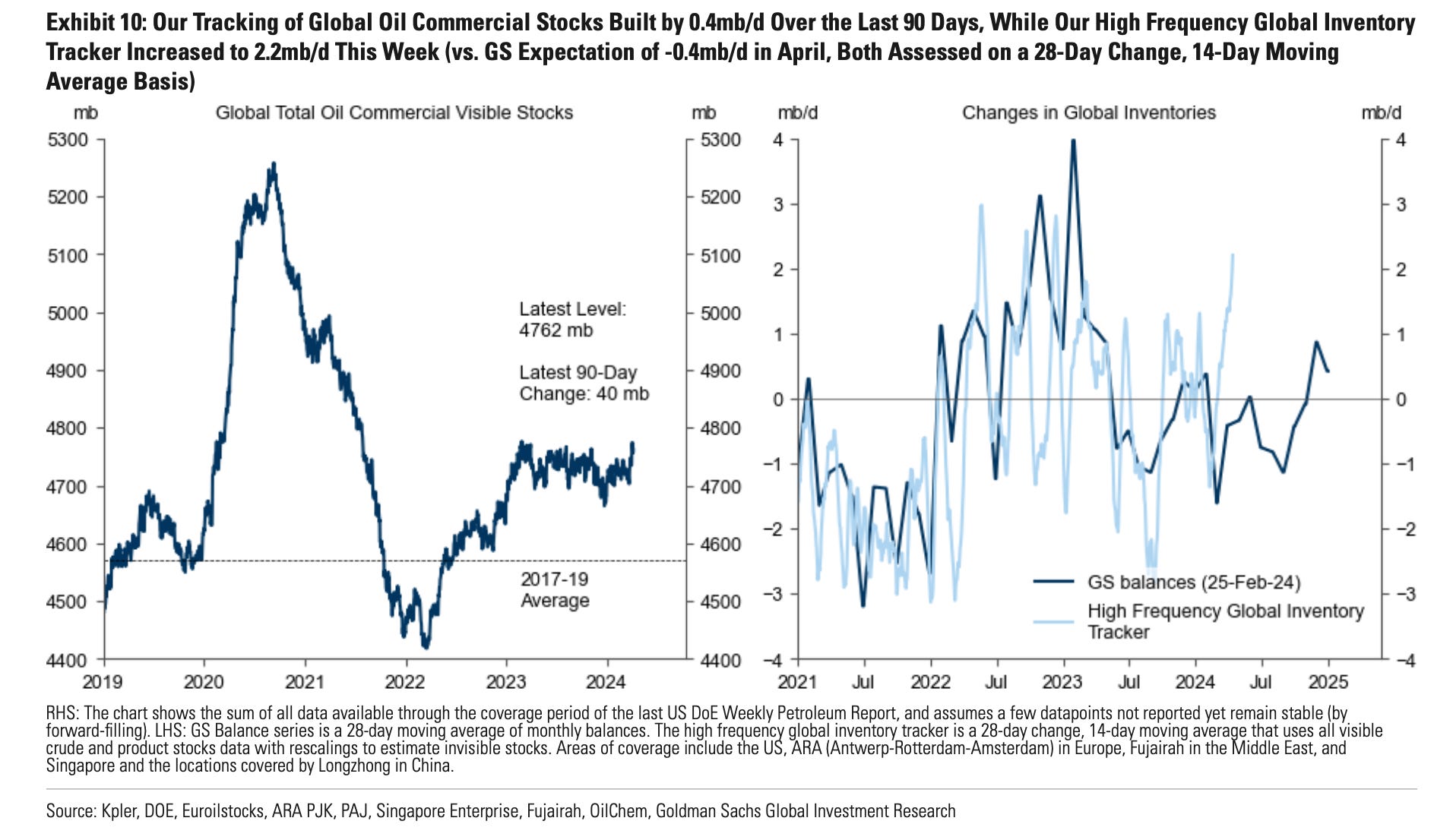

Fundamentally, oil inventories have built this April, offsetting the draws we saw in Q1.

On the demand side, crack prices have similarly fallen from the highs.

One would think that if oil prices fell, refinery margins would pick up if end consumer demand stays the same, however, the fade has rippled through to the entire energy complex.

It makes sense though because geopolitical premium is ephemeral. Unless the attacks disrupt supplies for an extended period of time, or threaten to do so, the premium will inevitably evaporate.

More cowbell!

What’s interesting are the reactions by the speculators and the recent tourists in the space. Those who are taking positions in the sector in the expectation that tensions in the Middle East will flare-up. The argument? Geopolitical uncertainty should lift oil prices higher because there’s a real threat that oil supplies could be disrupted. Iranian/Israeli tit-for-tat could escalate uncontrollably. At best oil sanctions will ramp higher, and at worst, oil assets could be attacked. In a word? War. Perhaps, but isn’t that a tail risk? A lower probability of that occurring?

Twitter analysts though would have you believe otherwise. Yet, that breathless exhortation that this conflict will rage uncontrollably and that oil should be repriced when all the backers are urging caution reminds us of Will Farrell banging on that cowbell.

The cowbells are funny because they’re so out of place. Unless there’s more cowbells, more and more uncertainty, what happens eventually is the tension fades and reality settles in. If supplies aren’t disrupted, then what are we talking about?

More importantly, OPEC+’s spare capacity (read: Saudi Arabia) looms in the distance. The Saudi’s participation in the coalition that helped defend Israel from Iran’s attack further shows that it could be convinced to release oil if properly induced. New security pact, Palestinian statehood, and economic agreements translate to a higher chance that the spare capacity can be brought back sooner than later.

Moreover, remember this key point. In the US, it is an election year. As we stated in our recent quarterly letter . . .

What could also detour the train is the Biden Administration. So close to November elections, would they allow oil prices to runaway? Doubtful, so if oil price cross $100/barrel because of a geopolitical spike prices, expect the administration to appeal to the Saudis to release its spare capacity. Barring that, the administration will likely release crude from the Strategic Petroleum Reserves (“SPR”). Since Russian’s invasion of Ukraine in February 2022, the US has released ~230M barrels from the SPR. With ~360M barrels remaining, it could easily release 60M-100M barrels at 5M barrel per week to cover any shortfalls. Sure it would leave the SPR depleted, but for swing state voters, the economy and their perceptions will be key factors in deciding the November election.

Look, we’re not saying that there is a zero percent chance that the Middle East players won’t make a mistake and push themselves into a war. What we’re saying is that given the actions so far, it’s a far lower chance of a miscalculation, particularly as Iran has always preferred working in the shadows/through proxies and Israel’s backers are preaching caution. Furthermore, even if there was a war, there’s little appetite to threaten oil supplies when it could boomerang back on the West, all of which are OECD countries that depend on low energy prices. If Western countries are turning a blind eye to Iranian oil sanction violations, that already tells you something. Lastly, there’s ways to mitigate a disruption, from the Saudis releasing spare capacity and boosting production to US/OECD SPR releases. Even if supplies were disrupted, there’s patches in place to calm the markets for a bit.

Ultimately, we’re on a continuum. It’s not war or no war, it’s not zero geopolitical premium or $10/barrel of premium embedded, and it’s not binary. Should one exist? Yes, our “gut feel” is a few dollars ($1-2/barrel), nothing more, nothing less. Given the stretched money-managed positions (i.e., the betting paper market), there’s downside risk here.

If geopolitical premium does continue to fade, then we have a few more dollars to go if Brent is to hit ~$85/barrel, where inventories would tell you where the price should be. Since we’ve fallen from $92/barrel (sitting at $87.50/barrel as we write this), we believe the money managed position above has already been slightly reduced. There’s still some downside left. Not a huge amount, but the oil market tends to over and under-correct, so be cognizant.

So enjoy the cowbells, just don’t bet the farm on them since they're transitory, or immaterial at this stage of the game. We’ll settle where fundamentals settle, and that’s a bit lower if the cowbells fade.

"Guess what! I've got a fever, and the only prescription is more cowbell!"

. . . comedy gold.

Please hit the “like” button above if you enjoyed reading the article, thank you.

Great read!