Oil Fundamentals in February. View from Above.

March 9, 2024

Another month just flew by, and now we’re into March. February came and went, and and the market ground higher. Though we’re wobbly today (Friday as we write this), for the most part, February was a good month, even for those not in tech.

Well would you look at that. Even those invested in the energy space did okay. Much of that was because in February, XOP and XLE gained 5.5% and 3.3%, respectively. A catch-up to the SPY, which punched higher by another 5.2%, but just maybe this rally is broadening out a bit. Overall for the year, the entire market (up to Friday is up 7.7%).

Oil prices increased slightly in February too. Having averaged $77.63/barrel in December, we’ve been slogging higher. $80.12/barrel in January and $83.48/barrel in February.

It’s not much of a surprise to us though because if we snap back to our “holy grail” of charts (i.e., inventories to oil prices), we’re getting closer to where we should be.

One could quibble that we are actually slightly below where we should be, and we wouldn’t argue with that. To be fair we’re probably under by a few dollars, but much of that will depend on the direction of inventories in the coming months. So how’s that looking?

Well for February, the price movement has been positive despite inventories not really doing much. For the most part oil inventories have been pretty flat in the new year. This isn’t entirely unexpected since this is the low demand seasons (winter). What is positive is that we aren’t building during this offseason, and more importantly supplies aren’t increasing like they were back in Q4.

For now, we’re seeing onshore storage stay low. Oil on water, however, has been increasing as boats take more circuitous routes worldwide (more ships sailing on longer routes) as attacks near the Suez Canal have disrupted flows. Combine the two (oil on water and onshore inventories) and you get a pretty flat picture.

Here’s an enlarged view for those who want the “full picture.”

That’s a partial explanation, however, as demand has actually been decent even though we’re in the midst of refinery maintenance season. So on balance it’s been “okay,” and “okay” ain’t that bad. So yeah, satellite is showing a flat year-to-date thus far. We’re seeing what others are seeing too. If you were wondering, here’s Morgan Stanley . . .

Not much difference right?

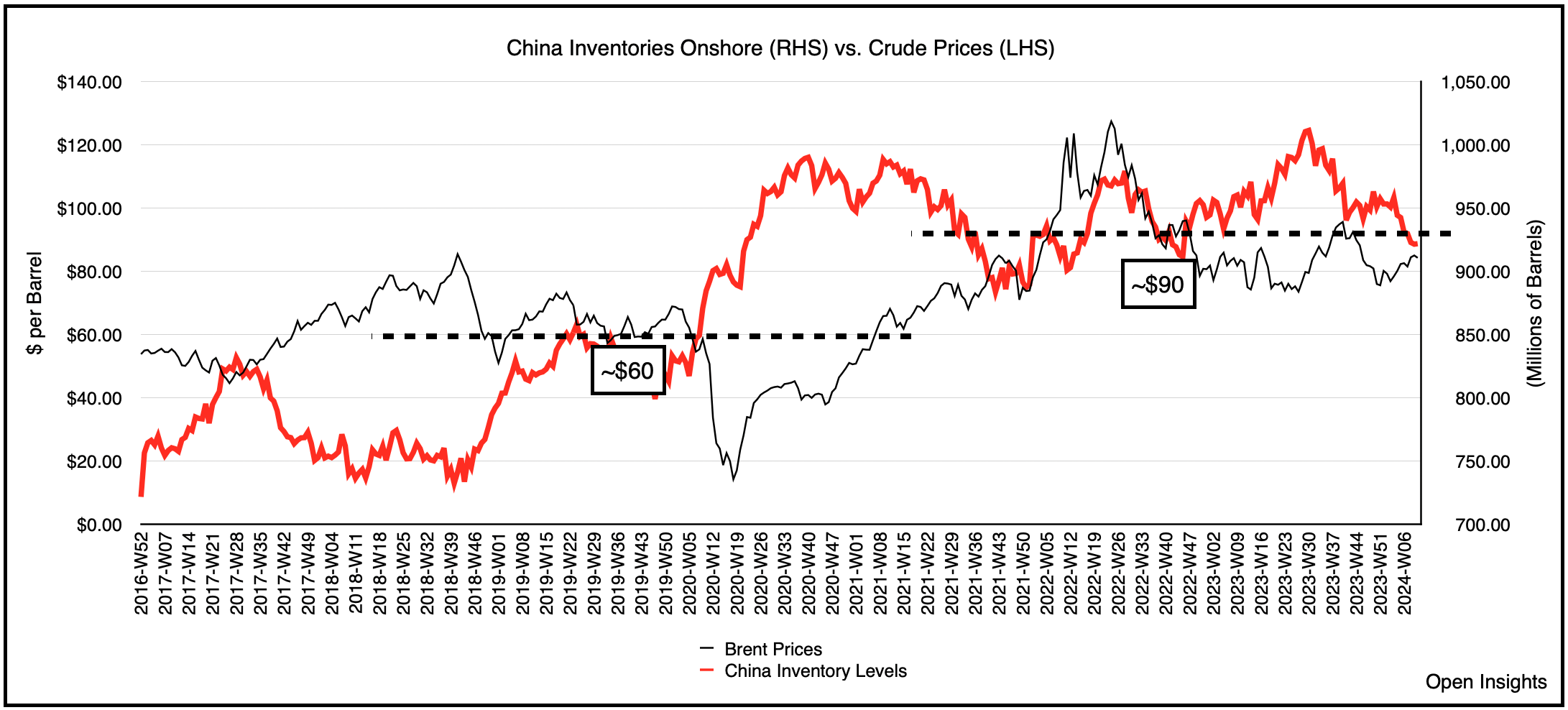

Still though, oil prices have begun to improve. At least in the last two months. As the economy churns, and as we enter and then exit the refinery maintenance season crude demand will turn higher. What we’re hoping to see is also some type of China recovery. If so, they may be forced to dip their toes back into the water and build crude stocks. Surprisingly, China has been whittling away their onshore stores, instead of restocking after release stocks last summer to combat higher oil prices, they haven’t really replenished their stores.

You can see above they’ve typically released stocks when oil prices climb beyond a certain point, but they’ve yet to replenish them in full once prices fully dipped. Furthermore, it’s not like they’ve rebuilt their floating stocks offshore either to cope . . .

So as we enter refinery maintenance season, the key question is do we build inventories worldwide? If so, prices may soften to allow China to replenish their stores. If, however, stock builds are contained and inventories remain low because of (take your pick: Middle East supply disruption, stronger demand, weaker supplies, OPEC+ “cuts”/restraint), we could be setting-up for stronger pricing into the summer. So these next two months are pretty critical to shaping the trajectory of where prices are going. Build and we’ll need to digest the bolus. Stay lean, and users will start to get hungry and grab at barrels.

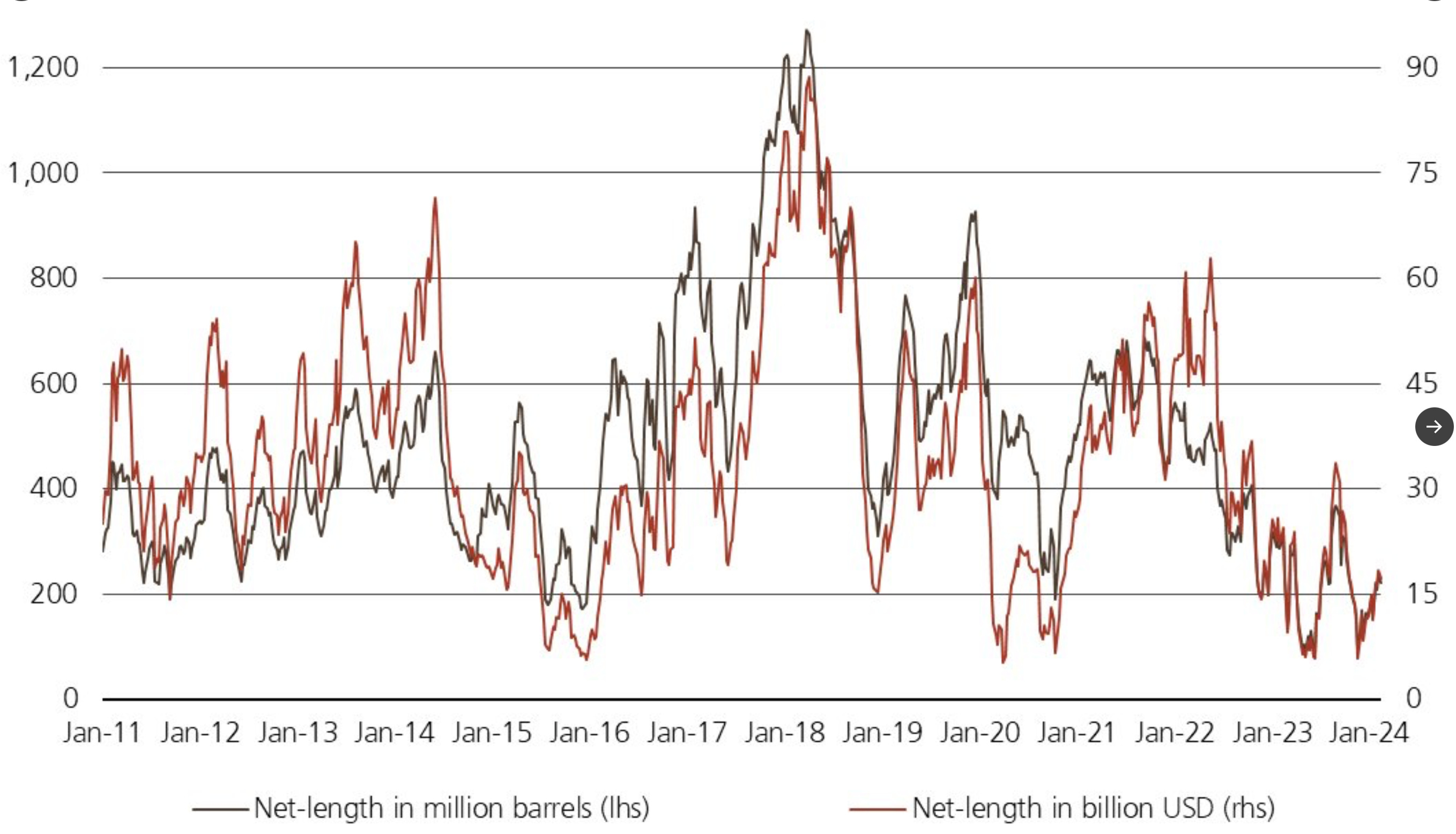

For a market that’s physically strong, but financially ambivalent (credit: Giovanni Staunovo) . . .

. . . this is setting-up for prices to skew higher if the world gets the munchies.

Now that’s a chart we’d like to see.

Please hit the “like” button above if you enjoyed reading the article, thank you.