Oil Investors Today: We're the Turkey

November 26, 2021

How quickly Thanksgiving comes every year now. I seemingly blink and another year flies by. We’re in the fourth quarter of 2021 and the clock’s ticking down. Admittedly it’s my favorite time of year. I’m prone to nostalgia, traditions, and family/friend gatherings. It’s made even more fun now that I have kids as the lights and sounds of the holidays begin to widen their eyes and brighten their smiles.

In the US, Thanksgiving’s that one holiday where we look-up from our daily myopia and spend a moment to give thanks for all the blessings around us. It’s a time where we can express our gratitude for all the things we’ve been blessed with, and yes, to even be thankful for the things we’ve been able to endure.

So as we all gather around the table for heaping forkfuls of turkey and tryptophan, try to give one last thanks before the drowsiness overwhelms you. Try to give thanks to that thing that keeps on giving . . . the Strategic Petroleum Reserve.

Yes, the Strategic Petroleum Reserve (“SPR”). Right before the Thanksgiving holiday the SPR was the talk of the town. In an effort to quell rising gasoline prices, the US has been working with the IEA, Japan, Korea, China, India and Europe to coordinate a crude withdrawal from their individual SPRs. Unsure of the size, the oil market turned risk off, and Brent prices promptly receded by $8/barrel from $87/bbl to $79/bbl. After three weeks of will they/won’t they, the White House announced on Tuesday a coordinated release of SPR crude. This non-IEA release was coordinated ultimately between the US (50M), Japan (4M), India (5M), and South Korea/China/UK (6-11M), for a total release of 65-70M.

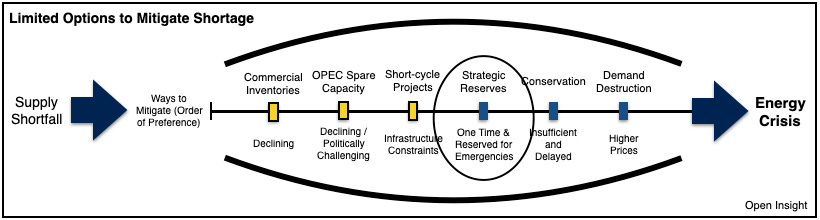

The amount would seem substantial, but a few things to keep in mind:

The US plans to make 50M barrels, but 32M barrels will be made available via an exchange. Although refiners can obtain these barrels, they’d need to return the barrels (plus “interest”) at a future date. Even if traders acquire the barrels today, they’d need to hedge the price in anticipation of the return (lest they overpay in the future). So financially, making more barrels available today means the prices for the front months should decline slightly, but as traders hedge out the later months (for the return), the tail of the oil price curve should rise. Physically, if the structural undersupply continues, inventory balance may be even tighter in the coming months, which means the returns could further drain commercial stocks and be bullish for prices. For the remaining 18M barrels, those are Congressionally mandated sales being pulled forward, so those barrels will shift from the left pocket (SPR) to the right pocket (commercial balances). This amount will subdue inventory draws in the coming months, but truth be told, most analysts have an eye on global balances, SPR or not. Global inventories are drawing and simply accounting for it differently matters a little, but not as much. Tight is tight.

Everyone else - China has yet to announce the amount of SPR release it plans to make, but as they’ve already been releasing crude stores, it’s unlikely the amount is in addition to what they previously planned. India is similarly double-counting as they had previously planned to sell down its SPR to make room for commercial storage rentals in its tanks. Lastly Japan, South Korea, and UK’s releases are immaterial and more symbolic than anything.

Which brings us to symbolism. At this stage (i.e., the last) this is what we’re left with. Symbolic SPR releases.

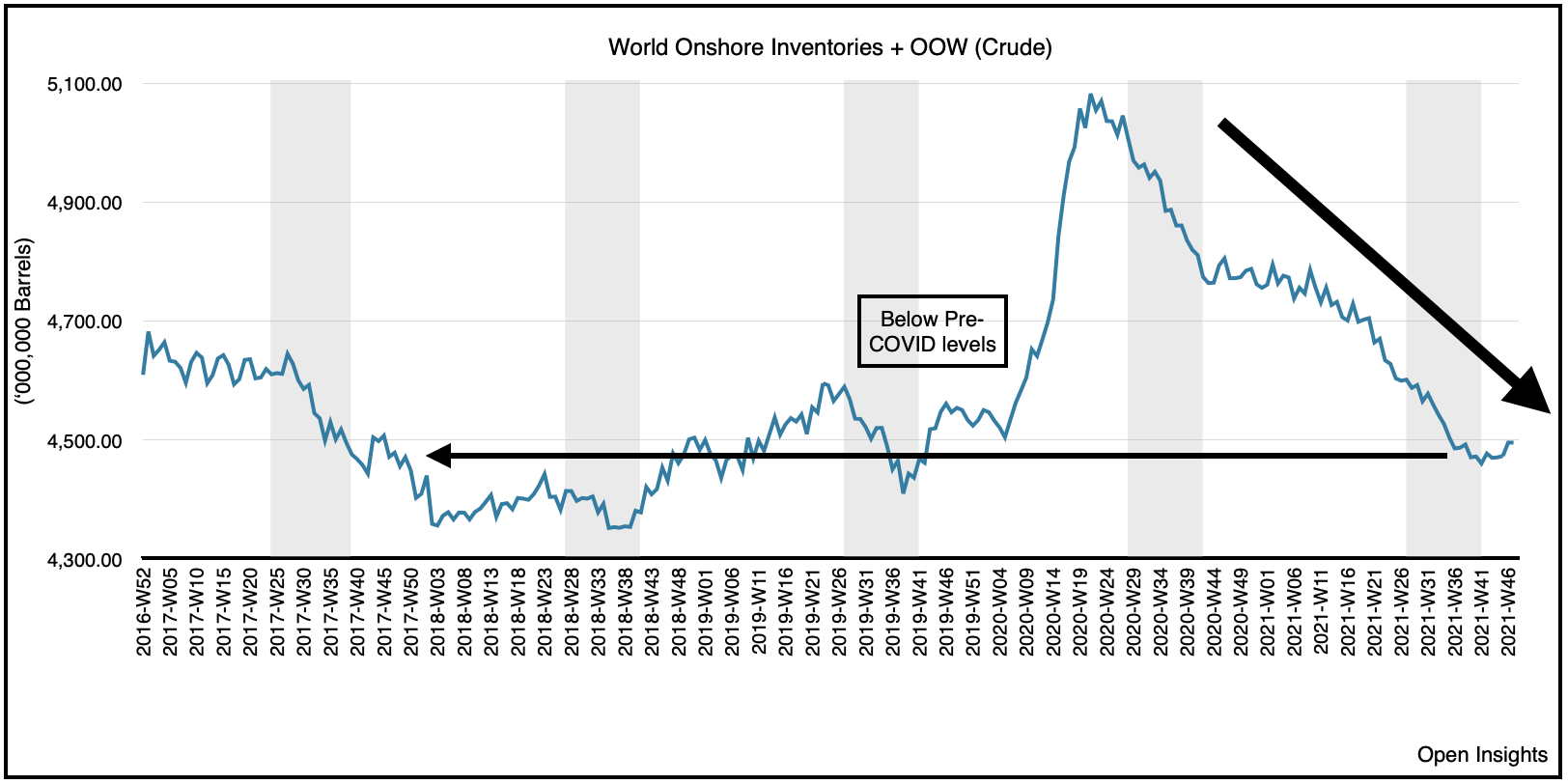

The winter stores. We’re now releasing and eating into our emergency stocks just to quell $3.50/gallon gasoline prices. Prices that are not deterring consumption one bit as evidence by implied demand for gasoline in the US. For the past week, our implied demand in 2021 notched higher than 2019 levels (the graph below for 2021 compares to 2019).

Global inventories also continue to draw unrelentingly even with the recent spikes in COVID cases, and we don’t believe demand will contract materially.

Recovering air travel coupled with pent-up demand will spike consumption, despite COVID. The US holiday travel season is already proving robust, and we anticipate similar travel patterns will repeat in China as two years of COVID have prevented many families from congregating. Take a gander at the last graph (TSA checkpoint travel numbers, which are near 2019 levels).

In the end, we see the SPR release as a choice among a palate of bad choices. Reducing RINs for refineries would draw the ire of farmers and environmentalists, banning exports would inevitably spike Brent prices and push gasoline prices higher, and pushing NOPEC legislation and/or acquiescing to Iranian JCPOA demands would have garner grave geopolitical consequences. Eventually that leaves an SPR release, but that option simply delays (and only briefly) the inevitable. A structurally imbalanced market that with each draw draws us closer to an energy crisis. At this stage the SPR release is akin to a stop sign in front of a freight train that’s our impending energy crisis. Still be thankful . . . be thankful that our leaders haven’t pulled the ripcord on any of the other worse choices. Not that they won’t, but for now, even they know that they could make it worse. If symbolism is all they’ve to offer, then we’ll take it. Happy Thanksgiving.

Update . . .

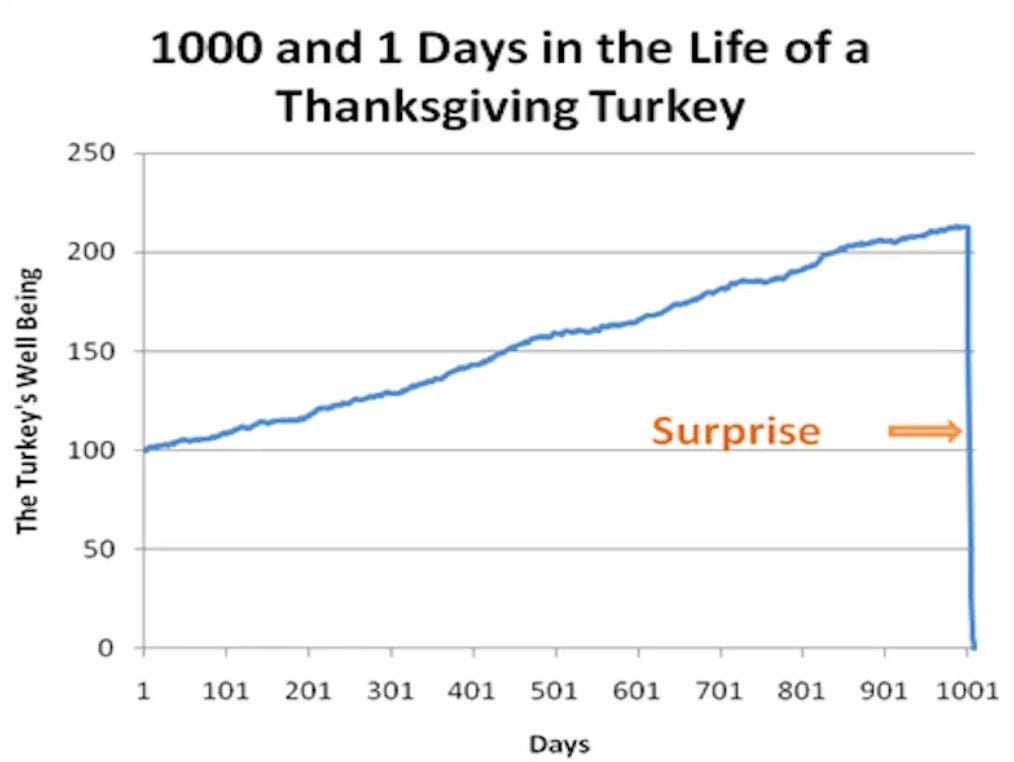

Now we penned that article above a few days ago in anticipation of posting an updated global inventories chart on Friday (which we have above), only to find ourselves in the midst of a panic induced, liquidity reduced, holiday market sell-off. Today . . . we’re the turkey.

Oil prices are off 12% for WTI and 10% for Brent, with the former having fallen to $68/bbl and the latter $73/bbl, almost $9-10/bbl less than the day before. Headlines about a Nu COVID variant have been running rampant, and with many traders on the sidelines already (whether because of the holidays or they closed out their trading books to be “risk-off” into the year-end with all the SPR jawboning), we’re left with a dearth of buyers. Bearish COVID headlines means the algos are running wild. Algos meet the market . . . algos run over the market.

So fall the oil market does, careening uncontrollably as stops are taken out and funds re-hedge even lower. The selling cascades.

Yet, we sit here pondering whether all of this is warranted . . . knowing full well that in many ways it’s not. The Nu variant was identified on Tuesday (November 23) in South Africa, stemming from samples collected November 14 to the 16 (South Africa Department of Health). Scientists have yet to fully test the virus against the current batches of vaccines, and Moderna has indicated it will take a two weeks before we understand whether their vaccine is still efficacious against the new variant. We’d anticipate the same time frame from the other vaccine manufacturers. Even if we had lab results, the real world results will be different. More data will still be needed not just on transmissibility, but on hospitalizations and deaths among the various demographic groups.

Yet, before this basic groundwork has been laid, South Africa and the WHO held a press conference to announce their “discovery.” We’re not saying to ignore the news, this certainly has implications on the global economy and public health, but can we at least take a moment to weigh the implications of what’s happening before cratering asset prices and sending people into a frenzy? It’s not the world we live in though right? Our need to “beat the competition” in the news cycle or “warn the people” means we have scientists and politicians playing Paul Revere. That’s problematic because if anyone bothered to stop the galloping horse, the rider wouldn’t be able to answer the natural follow-up question . . . are the vaccines still effective?

Insert should shrug emoji.

Then what the heck are you yelling about??

If Moderna states that it’ll take a few weeks of testing before we know something more definitive, that’ll be our timeline. So risk adjust those portfolios accordingly, but the market has likely already done so by dialing “risk-off” to maximum.

What’s happening now, however, is that the uncertainty of Nu COVID will outweigh the certainty of what will happen to supplies after oil prices have declined so precipitously. We’ll know in a few more weeks whether Nu COVID renders our vaccines less efficacious (because that’s really the fear here), but we’ll know within a few days how OPEC+ and oil companies will react to the recent price volatility. Undoubtedly (no, UNDOUBTEDLY) they will all turn increasingly cautious, reducing supply increases and tempering 2022 capex budgets. This isn’t the temperament you want when just two days ago we announced an SPR release to tame oil prices in a structurally undersupplied market.

We don’t know yet how the Nu COVID variant will or will not impact global health and in turn, global demand, but we do know supplies in the future will now be lower than just yesterday. We do know that a $9-10/bbl decline in prices is equivalent to pricing in a 4M bpd demand hit (i.e., double the 2M bpd demand hit in last winter’s COVID wave), when in fact no such hit has occurred yet. We do know that in the oil industry, shades of 2020 COVID fears will reemerge and if you stay still for a moment, you can hear the collective shudders in the executive suites of the E&Ps.

Our path to $100/oil won’t be smooth, but if Nu COVID turns out to be manageable, it’s becoming increasingly assured. For today though . . . we’re the turkey.

Great article. "Filtering the Market Noise" - not an easy task these days.