Oil Update and the Lagging Draws

May 22, 2026

Okay, let’s talk oil. $96/barrel right now after what’s news reports that an agreement to defuse the current standoff is within reach between Iran and the US. Though there still are issues, particularly around what’s in and what’s out of the initial agreement, there seems to be some progress being made, or at least a concerted effort to do so.

Is this really a 30 day extension of the current ceasefire, or is this a transitory step to something more . . . permanent? It’s unclear.

What is likely happening is the framing of the issues, and the cadence of the steps each party will take as we walk through these next few weeks. Call it a trust exercise, or heck call it “trauma bonding,” if you want, but whatever it is this will take time. Particularly when both parties are saying “you go first.”

Really though the Iranian’s are feeling flush at this stage. It has the leverage in both time, geography, and political will. The US does have two weapons though: a military hammer and a really large bullhorn. Frankly, it’s using the latter to great effectiveness as oil pries have milled around in a very specific Goldilocks range.

Thanks to US jawboning, the price has stayed fairly rangebound between $90 and $110/barrel. The increased volatility stemming from an outlandish tweet at anytime of day, amplified by certain media members, means traders simply can’t hold long positions with any conviction. Not only will their systems automatically flag the vol, but the value at risk also jumps. What ends up happening is the capital gets skittish.

With traders vacating their traditional role, we’re left with the physical market to tighten and tell us what the true price of a barrel of energy should really be. What’s surprising to us is how well the physical market has hung in there for the past month. While inventories are falling, a buyer’s strike from refiners is occurring. There’s little reason to buy if the pundits, the President, and analysts are all predicting a quick resolution to the conflict. Though they’ve been doing so for the past few months, one of them will be right one day, and the longer this drags on the more likely that happens.

The zeitgeist is almost certainly that oil prices will fall quickly in such an event, and from a risk/reward standpoint, let’s play it out and wait. Draw inventories and reduce run rates, and pray for a speedy resolution. Why bid on high dollar barrels if you can stay patient? Sure product stocks will draw if refiners don’t produce, but that’s the consequences of picking your poison.

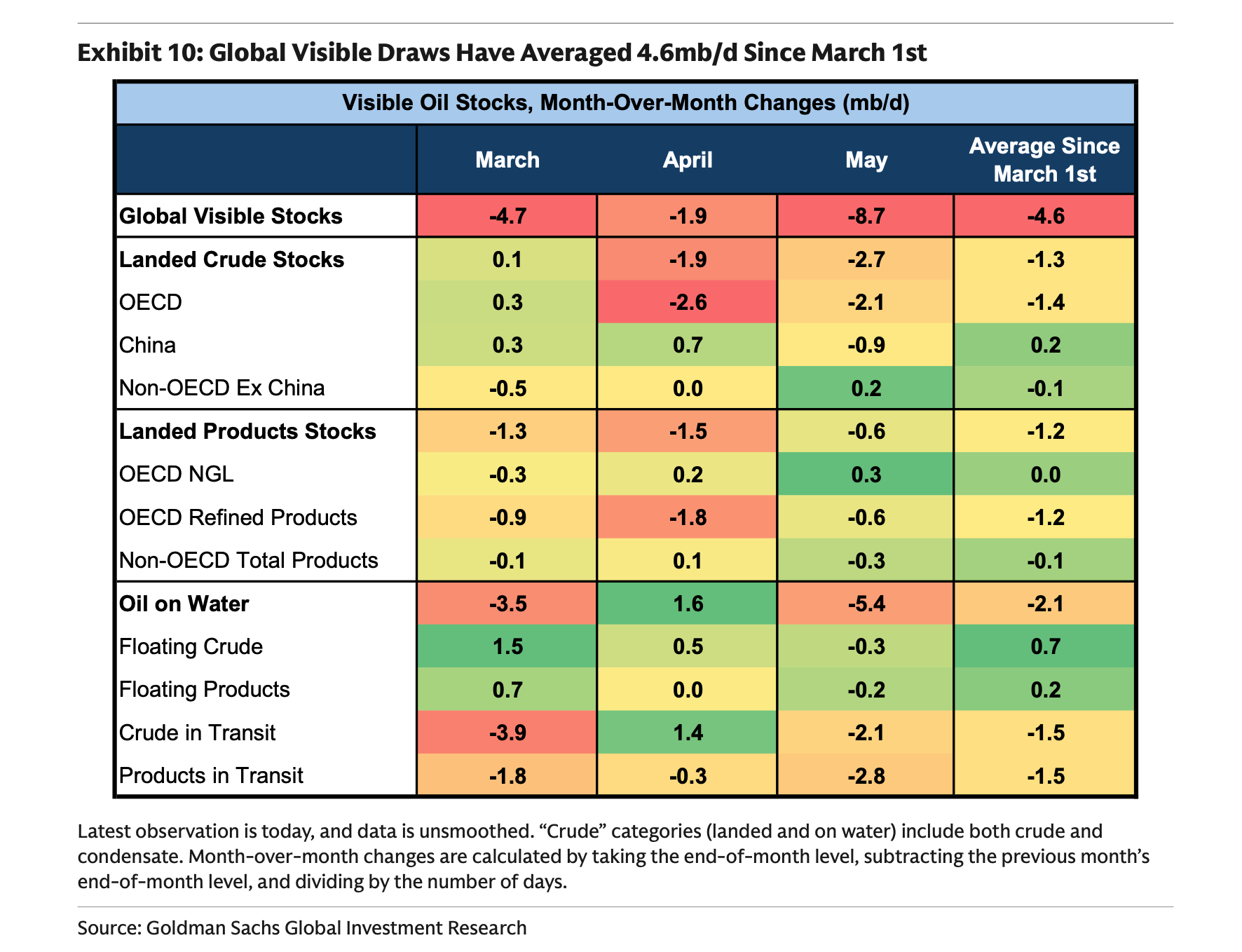

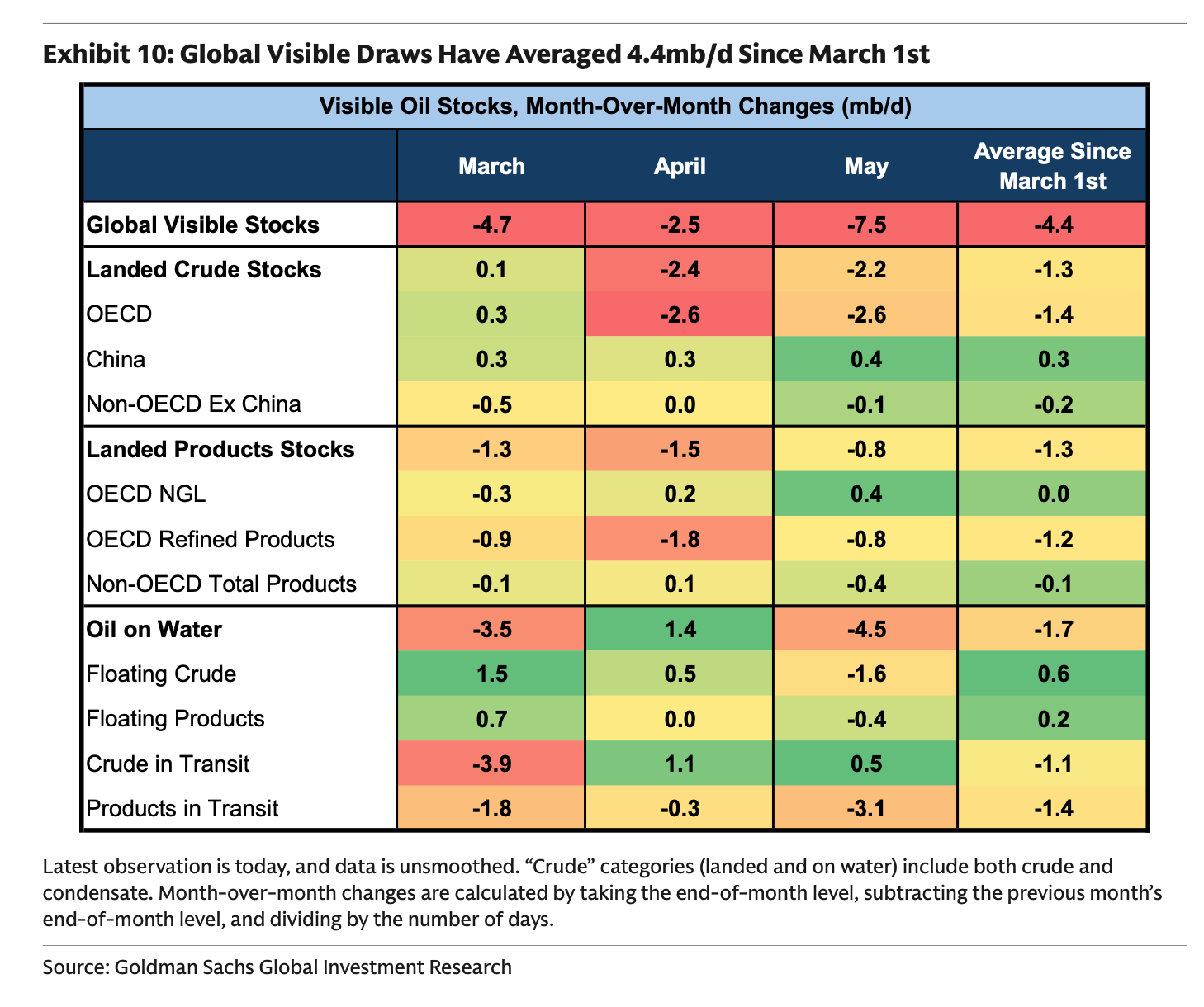

Everyday is a Draw

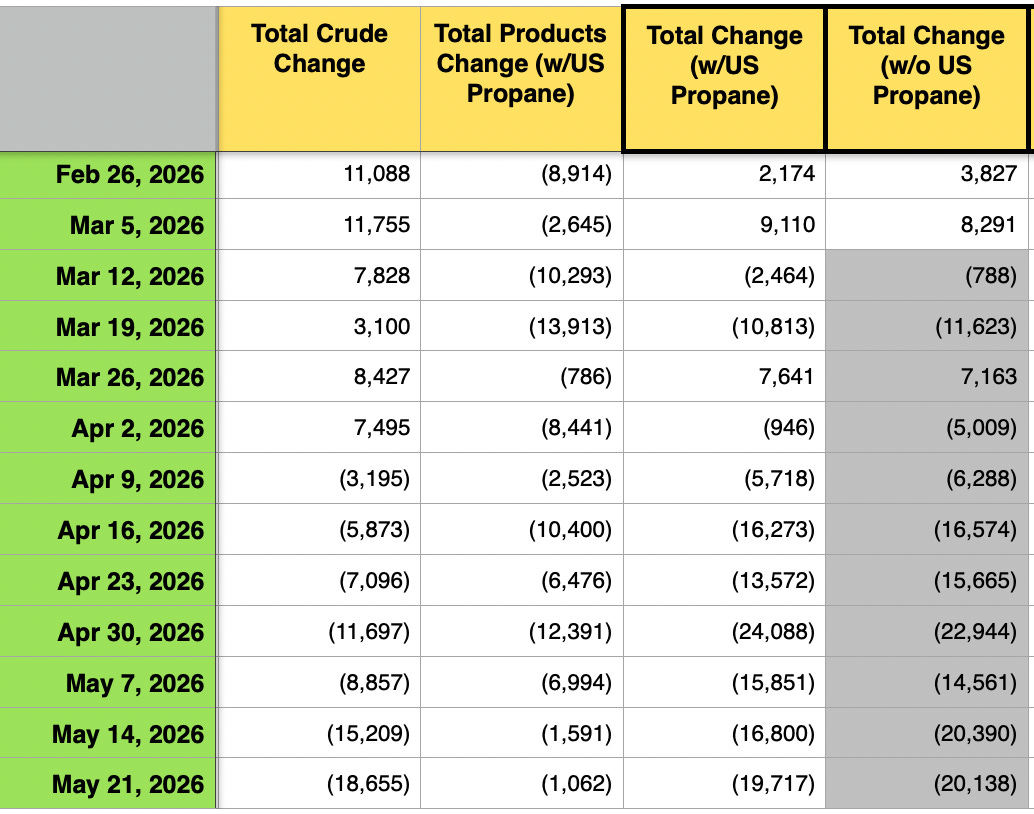

We’re 2/3rds of the way into May, and the overall deficit is approaching 9M bpd as visible oil inventories start to truly reflect the supply outage.

Compare that to the same chart last week, and already we can see May figures have increased from 7M bpd.

Lag-Effects

It’s the lagging impact of this entire venture. Once Asian stocks depleted, the pull on Western inventories have picked up materially. Supplies disrupted in March and April are only starting to show up in the other visible parts of the world (i.e., Europe / US). Storage information/data in these regions/countries is less opaque, and the March and April outages are beginning to show given the lagging impact of how oil moves through the system. It’s lagging both in terms of how it shows up in the data and in timing. As Western crude/products start getting pulled in large amounts, land stocks will draw, but oil-on-water (“OOW”) will increase as the barrels are exported. Once they land, OOW will decline, and land stocks will rise, only to finally fall when the barrels are refined/consumed. Eventually though, it will all fall, OOW will settle, whereas land stocks will decline. It has to unless China decides to just step-in and plug any gaps with its vast SPR (doubtful).

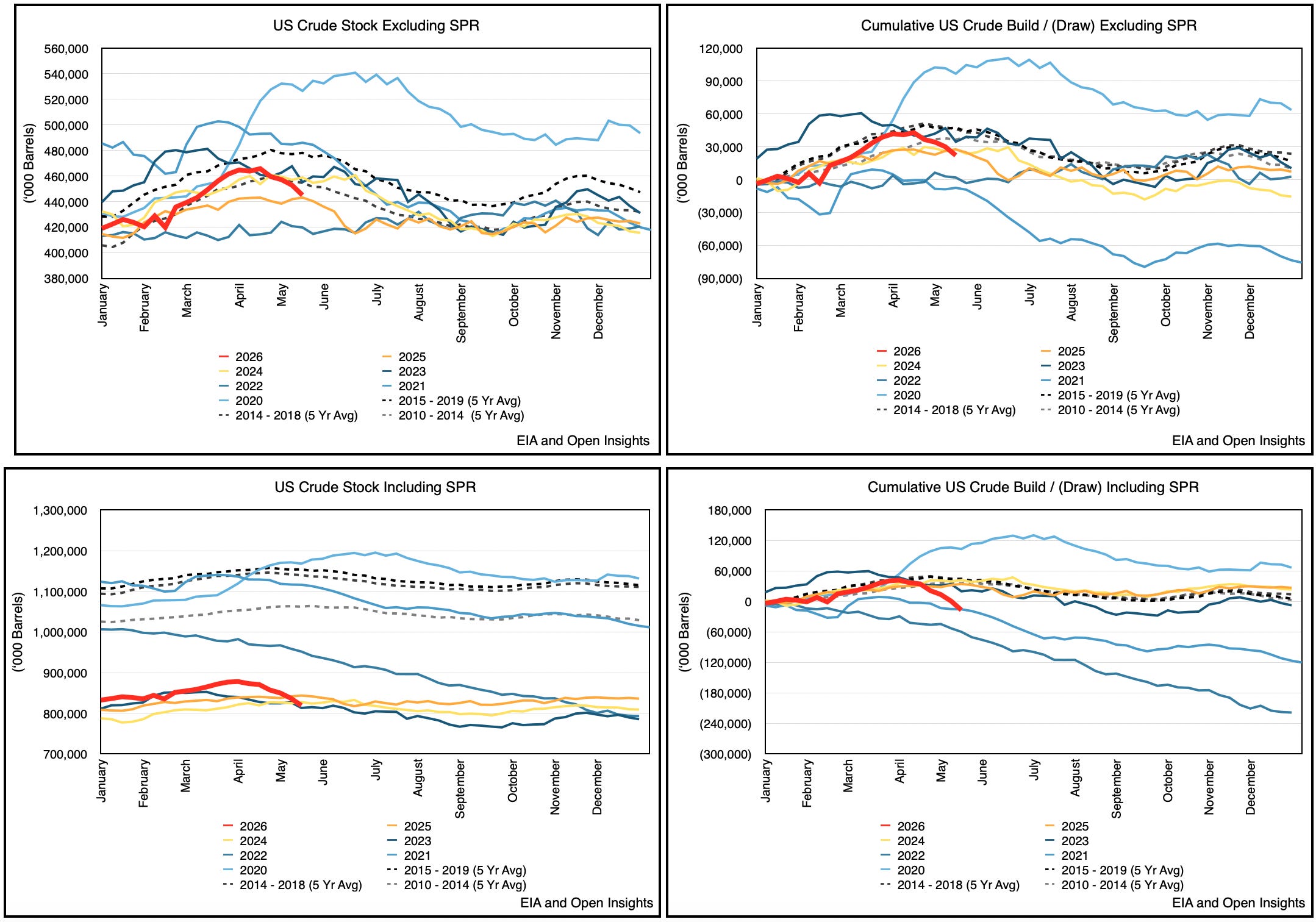

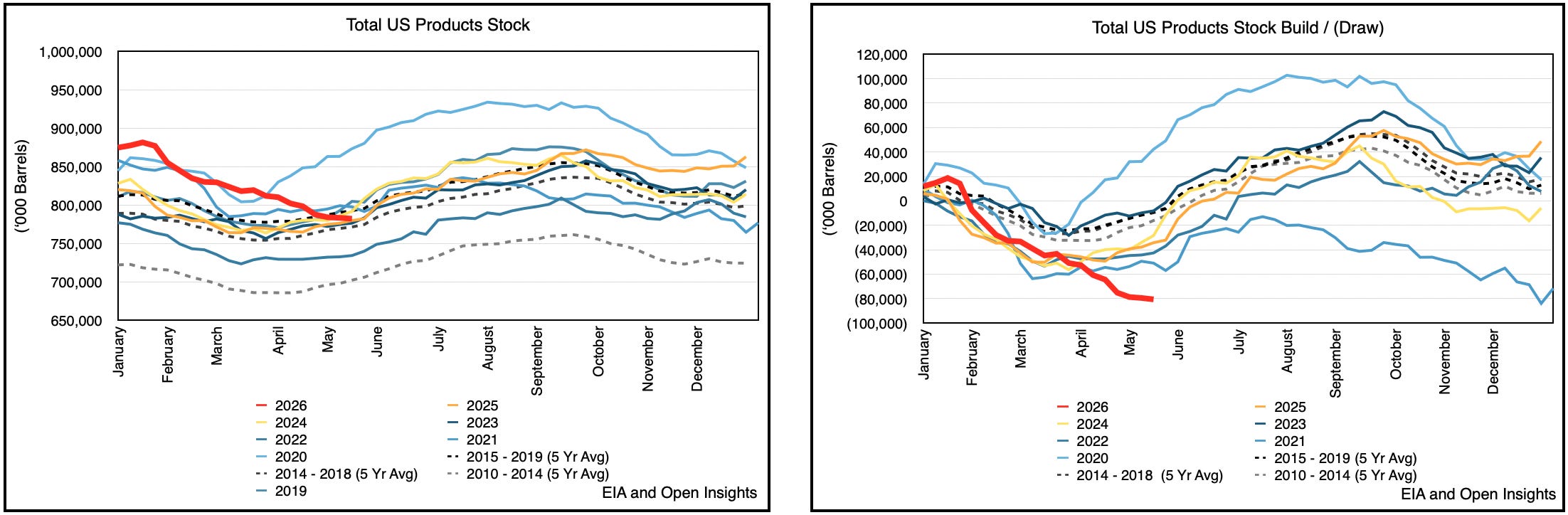

From a timing perspective, we further anticipate this will continue into late summer, as March’s SoH outages “show themselves” in the figures for April, and April’s SoH outages show in May, and so on and so forth. We can already see the impacts in April’s data as inventories of both US crude and products have started falling counter seasonally.

It’s clear from the charts above that product stocks here will get spicy. We typically build inventories now and into the summer for consumption in the fall/winter season, but this year, we’re seeing a counter-trend, which means there won’t be as much available by October. Product prices are likely to stay elevated into year-end, which means refineries will run flat out. Commercial crude inventories are doing much better though since releases from the US SPR have been so hefty. That portion won’t stop for awhile. Net/net, commercial crude stocks will still draw despite the SPR release and for many months as seasonality coupled with global export demand pulls barrels away. WTI and Brent pricing will need to close that gap for barrels to remain in the US, but they’ve yet to do so.

Zooming out a bit, our real-time OECD tracker also shows the bleed down. With little to no evidence of demand destruction (particularly in the better insulated and wealthier countries (i.e., filled with high energy consumers)), the draws will keep occurring until supplies improve.

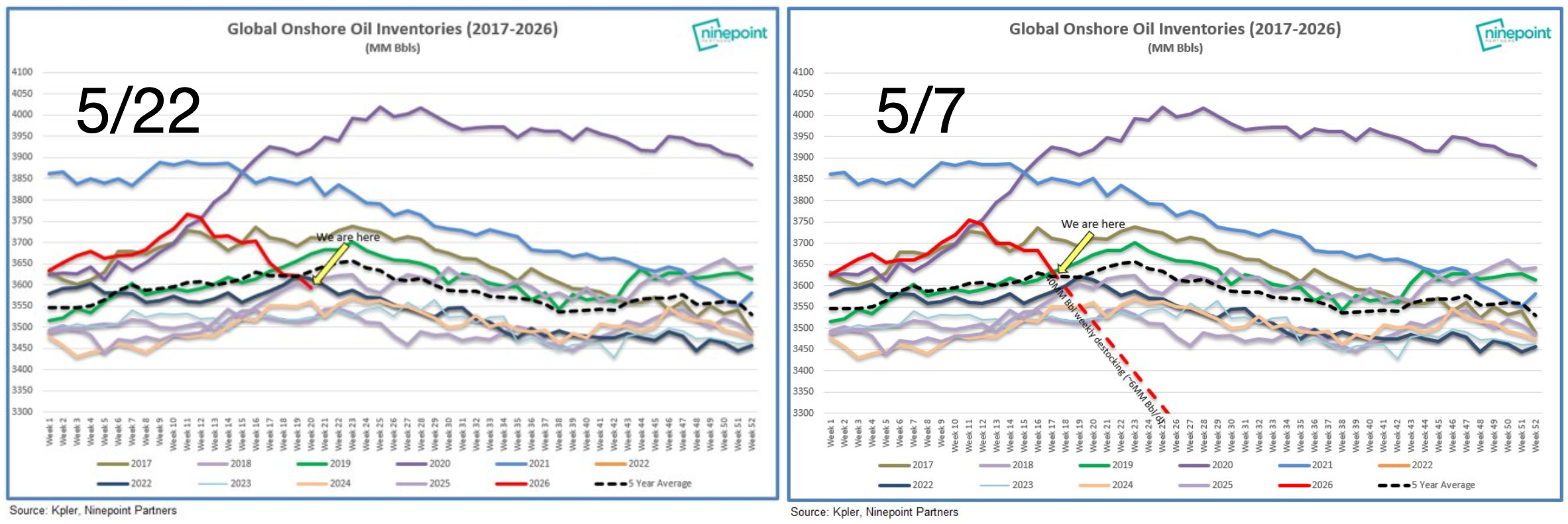

In total, global onshore storage though is falling, and will continue for the coming weeks. Here’s Eric Nuttall from Ninepoint.

Though not as steep as he initially projected, we think the draws will still be about the right amount in quantum, if not pace. If no one’s cutting back materially in their habits, then the draws are inevitable.

Drawing Now, and Drawing Later

So what happens in the coming weeks, will matter for inventory balances at the end-of-summer. Thereafter, remember, there’s still the matter of “normalizing” the SoH. Most analysts estimate it will take another 1.5 months to reorient the tankers as many have been sitting idle or re-tasked to other routes. Producers will need to drain on-shore inventories before they can restart the field, and they can only do so if the tankers start loading inventories. So even on a conservative basis, pencil in another 200-300M barrels lost as the ships traverse and reform their congo lines. We’re likely well into July before we start to see the first barrels reappear in Asia if things get sorted out . . . today.

It’s unlikely though because the current ceasefire draft between the US/IR means negotiations will begin after Hajj. The sacred Muslim pilgrimage to Mecca starts this Sunday and ends sometime next Friday, which means we’re into June already before the parties really sit down and grind through the specifics. If we’re being optimistic, we’re looking at a resolution likely in mid-June.

Even that’s a bit fanciful because can Iran and US resolve the open issues of uranium enrichment and the SoH in two weeks? We doubt that. The nuclear issue has been going on for nearly a decade, and the SoH has finally been weaponized. What’s the likelihood Iran enters these negotiations on its high horse and flexes its muscle? Yeah . . . high.

It makes sense though. They are “winning,” and the longer IR draws out negotiations, the more leverage it gains as global inventories really start to drain during the high demand summer season. We’re a bit surprised that the SoH has been closed this long, and at this stage, it’s really a wait-and-see approach we’re taking. Every week of closure means another +60M barrels lost. More if you count non-visible inventory draws and China’s SPR releases (some of which is come from underground stores). We still have 10-12M bpd of shut-ins and that’s really the missing key. March, April and May . . . and now likely June. Another month or two of this, and the impacts will directly impact Q4, and effectively all of 2026.

In turn, this will drive full year free cash flows (“FCF”) for E&Ps so high that they will materially deleverage, and/or drive significant shareholder returns (i.e., buybacks). Many companies will likely increase dividends by redirecting the newly freed-up cash used to previously pay higher interest expense, and by systematically shrinking their share counts. Companies could also issue one-time dividends, but again, they’re more likely to repurchase stock to permanently bake-in the benefits stemming from all this uncertainty. Every day is another dollar, and as this continues, it’ll only expose how cheap the shares of energy companies are, and how much of a folly this entire exercise has been.

June, here we come.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

thinking about export restrictions from US?

Well guess there's another (fake?) peace deal announcement. The 10th one in the past 10 weeks