Oil's Hopium at $70/bbl

April 3, 2026

$70.

That’s where we’re at. Sure the price of oil is well above $100/barrel today, but it’s $70/barrel at the back-end.

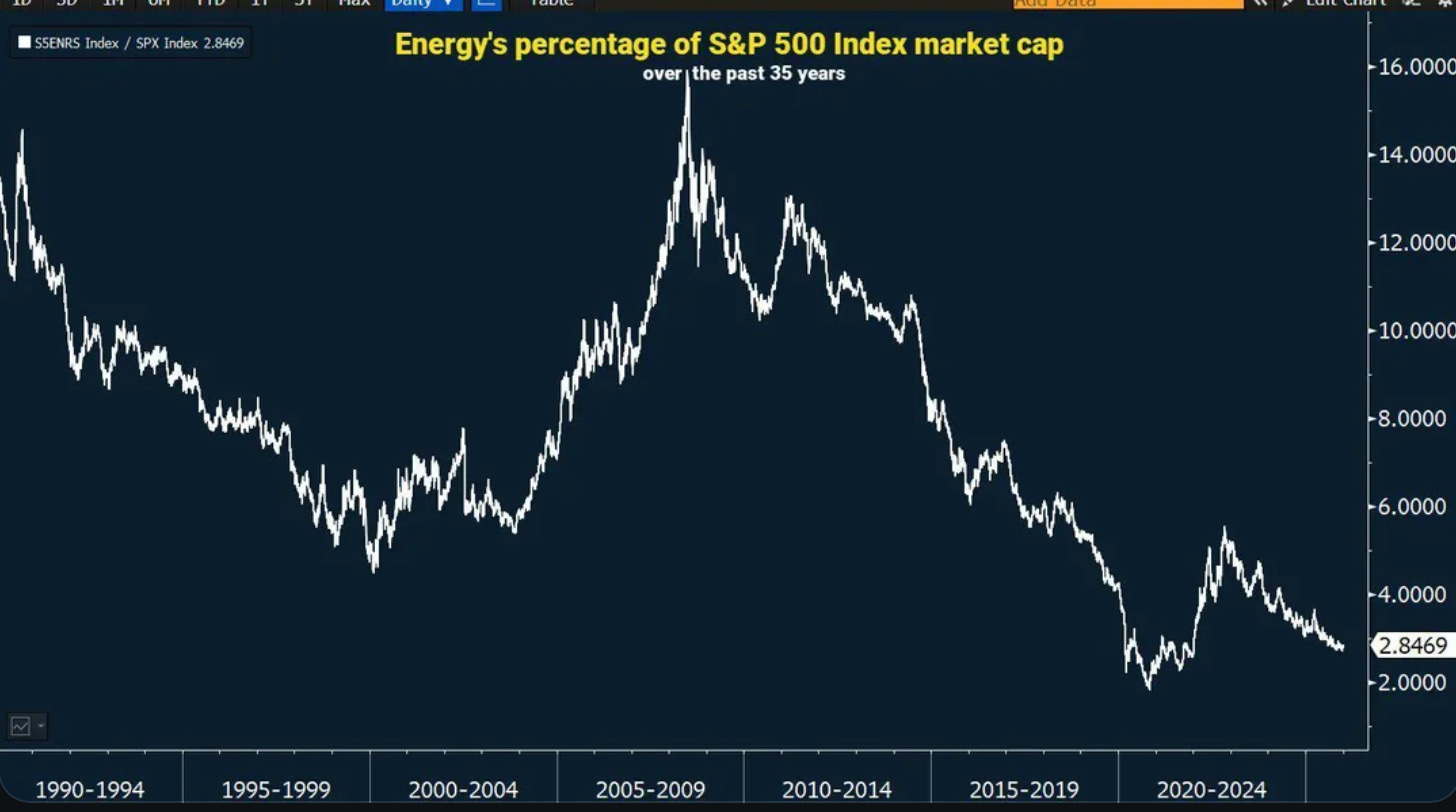

It’s a reflection of what’s become of the market all these years. One where energy holdings cratered to about 3% of the overall value, more than halving from 2022, and multiples more from earlier before.

It’s what happens when you spend most of 2010-2014 lighting shareholder’s capital on fire under the pretense of chasing growth. Forget profits, and the market inevitably forgets you. It is the weighing machine after all, and this sector has been found wanting.

So slam the overall value of a sector to 3% of the S&P 500, and it becomes a nuisance. Well actually neglected, as thinking it to be a nuisance means you’d actually have to care about it. Most don’t, so neglect it is.

As an investment analyst, follow a neglected sector for long, and you can watch your career die. Besides, there’s no investment banking fees to be had, so why even bother. Similarly, it’s a trash bin of companies with terrible capital management, so if anything you can short it. Over the long haul, if there’s a way this sector can torch capital, it’ll find it.

So we’re left with 3%, and when the current energy crisis struck, there were fewer analysts to cover it, let alone to understand it. The only group remaining were those who’ve been buried in the sector for so long that they can instantly recognize the crisis for what it is . . . not short-term.

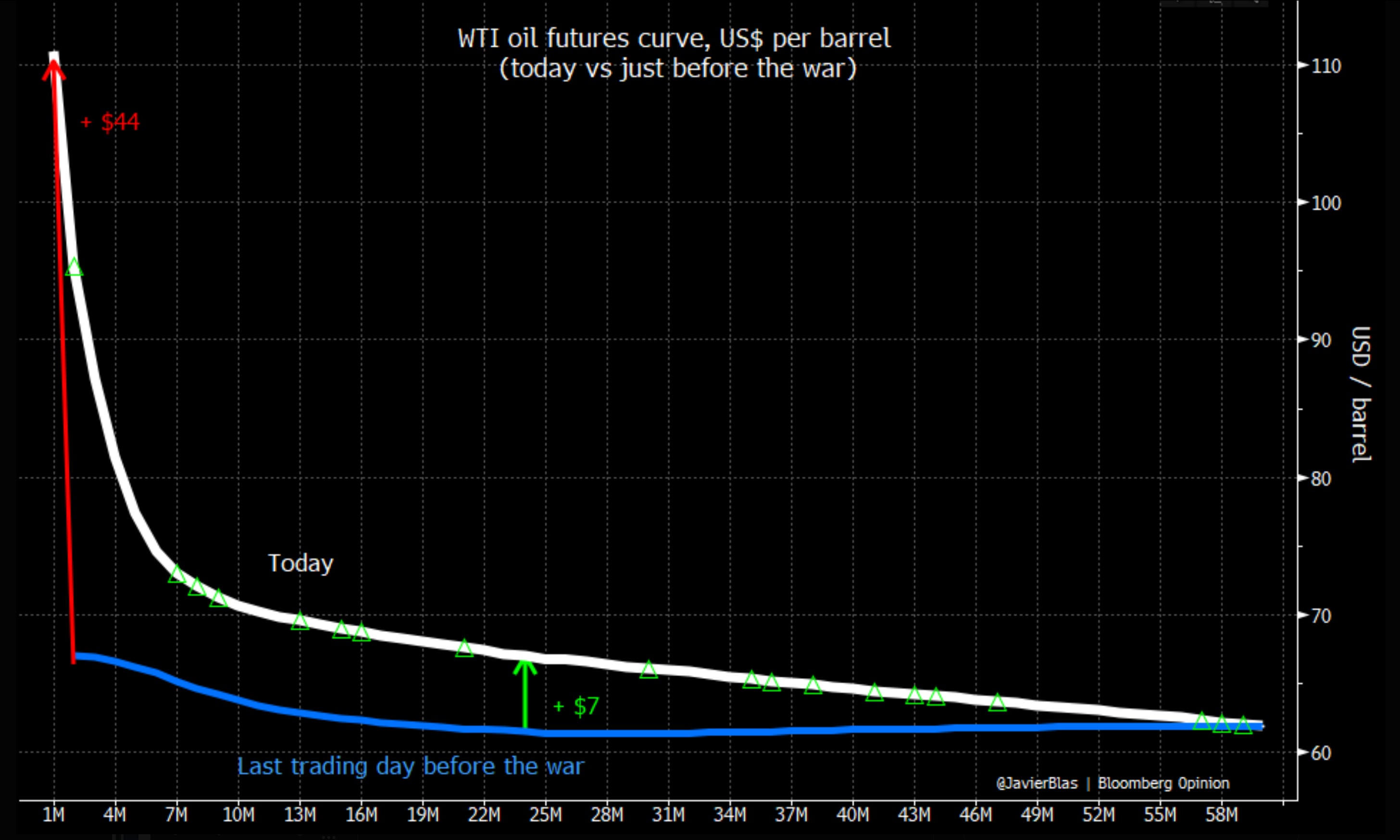

Others though will look at the futures market for confirmation. See? It’s predicting a cheaper price in the near future. Just look at the chart from Javier Blas.

$70/barrel by December! All will be well. Well . . . that’s not quite what it’s saying, but okay. Who are we to quibble, we’ve only been doing this for years.

We are the 3% after all.

The one great thing about social media (and especially Twitter) is the near instantaneous expert commentary (real or otherwise) that appears whenever a novel issue breaks out. As the US/Iran War wages on, market generalists have freely opined on geopolitics, military strategy, energy flows, and the nuances of the oil market. Aided by their preferred AI agent, the analysis has been delivered quickly, boldly and confidently.

This won’t last long they say, it will be painless, and once the Strait of Hormuz (“SoH”) is reopened, oil prices will plummet below the levels seen in pre-conflict. A peace dividend for all.

Frankly we don’t know. We don’t know what the day after will look like, the Day 1 after the all clear sounds. Can it end on April 15th? When Trump’s “2-3 weeks more” nears its end? Will Iran let him walk away, and reopen the Strait? As of now, we’re not entirely sure this thing doesn’t go far, far longer.

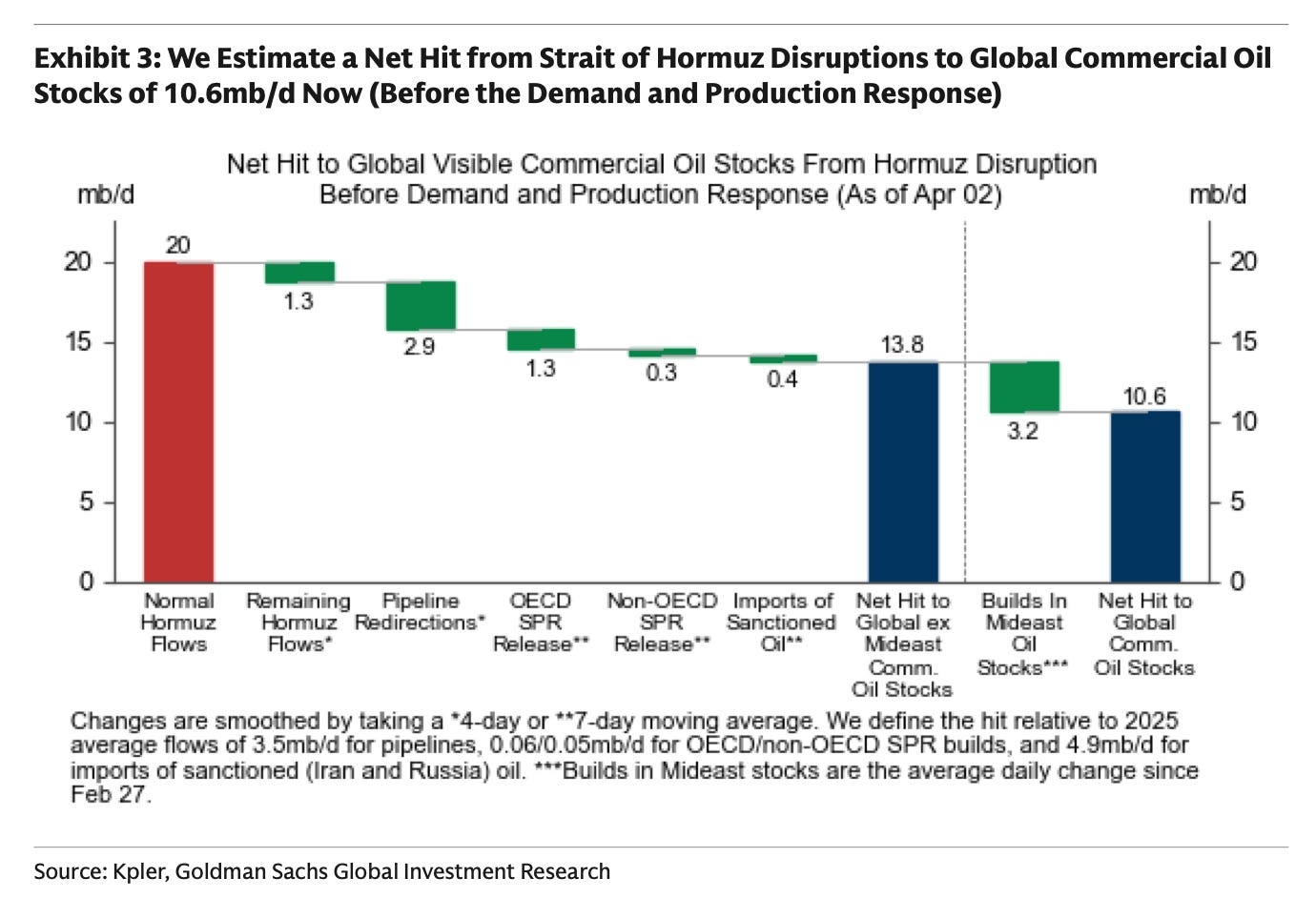

As this war drags on, the global energy situation will worsen. This is a 10-11M bpd deficit, and it will quickly carve-up the world. There will be the haves and have nots, those who can afford the exorbitant prices, and those who cannot. Those who produce energy domestically and those that do not. Third world and emerging markets like the Philippines, Thailand, Vietnam, Indonesia are going to feel the pain, but eventually that pain will migrate to Europe, and then the US.

Here’s some of the items we’re thinking through as the pain spreads, and why we think the pain lasts longer:

TACO - Trump Always Chickens Out works when things are unilateral (e.g., self-imposed tariffs), but in a war, it takes two to TACO and Iran has little incentive to eat and soothe the pain for the Trump Administration. This will drag on.

Abandon the Strait - Impossible. It would represent not only a strategic and tactical defeat for the US, it would subjugate Saudi Arabia, Kuwait, Oman, and the UAE to the whims of Iran in the future. Iran would effectively control nearly all oil flows out of the Middle East. In addition, given that China purchases most of Iran’s cargo, and Russia provides significant support, guess who benefits and gains further leverage behind the scenes? If the US was unwilling to let China gain an economic toe-hold in the Panama Canal, what makes you think they’d let Iran become a toll-taker in the Strait of Hormuz? Walking away isn’t a viable option.

Existential Threat - By removing the Iranian leadership and attacking Iran’s infrastructure, the remaining members of the IRGC know that this is a fight to the end. There’s little daylight to negotiate when everything is on the line, and they know the US/Israel could attack again in the future. If it’s a choice between our lives and your global livelihood, they’ll bet on the world blinking. This effectively extends the conflict and forces participants up the escalation ladder until the pain becomes unbearable.

The Price Gap - few appreciate the magnitude of this deficit because the prices aren’t accurately reflecting it. Whether it’s the jawboning, or the belief that this war can end immediately, there’s plenty of reasons for skepticism. Ironically, the artificially lower prices actually forestall real conflict resolution, and in fact allows the US and Israel to press their attacks. This reinforces the market’s optimism because all they see are successes of targets being bombed and the tweets about Iran’s inevitable capitulation. The war, however, continues, and the SoH stays blocked. Yet, since the back of the curve is at $70/barrel, then surely we’re fine? We are not.

SPR - the Strategic Petroleum Reserve releases aren’t a salve. It’s a bandaid on a bullet hole. The volume is insufficient, and the value is questionable. At full capacity, we think the SPR can release 2.5M bpd against a 10-11M bpd global deficit. In addition, much of the 400M barrels of SPR release (e.g., US’ 176M barrel release) was designed as a loan so refiners would need to pay back the loan at a later date with interest. Refiners are balking at that currently so the uptake on SPR barrels have been tepid. Eventually though, if there’s not enough barrels outside of the US, you can surely bet that US exports will ramp higher.

Immediate return - there’s a perception that once the SoH is reopened the barrels will quickly return. Logistically given sailing/discharge times, we put that at 2 months. So even if the war ended today, it would take 2 months to sort out the logistics of transportation, and for the first barrels to show up. The delta between supply/demand will shrink as the weeks move on, but we should expect inventories to fall further even after a ceasefire and detente is declared. Having said that maybe . . . and just maybe the curve is correct. It’s expensive today, but if it clears up, prices should fall, but stay elevated for a few months, and then head lower, though still remaining in backwardation, and still much higher than before.

Inventories - there’s also a perception that because there’s so much inventories on land and on-the-water, we can easily drain and handle a 1B barrel drawdown. That’s an illusion. If we continue this war until mid-April, we’ll have exhausted a significant amount of oil-on-water, and land inventories. By the end-of-April, analysts anticipate that close to 1B of barrels of oil are lost for the entire year when all’s said and done. This isn’t unreasonable given the 10-11M bpd of shut-ins, coupled with a slow logistical return. None of this is taking into account any damage to field integrity, etc. for oil fields that have been shut-in for so long. Kuwait estimates it would take 3-4 months to bring production back online. Hardly surprising as you’d need to repressurize the field and conduct tests.

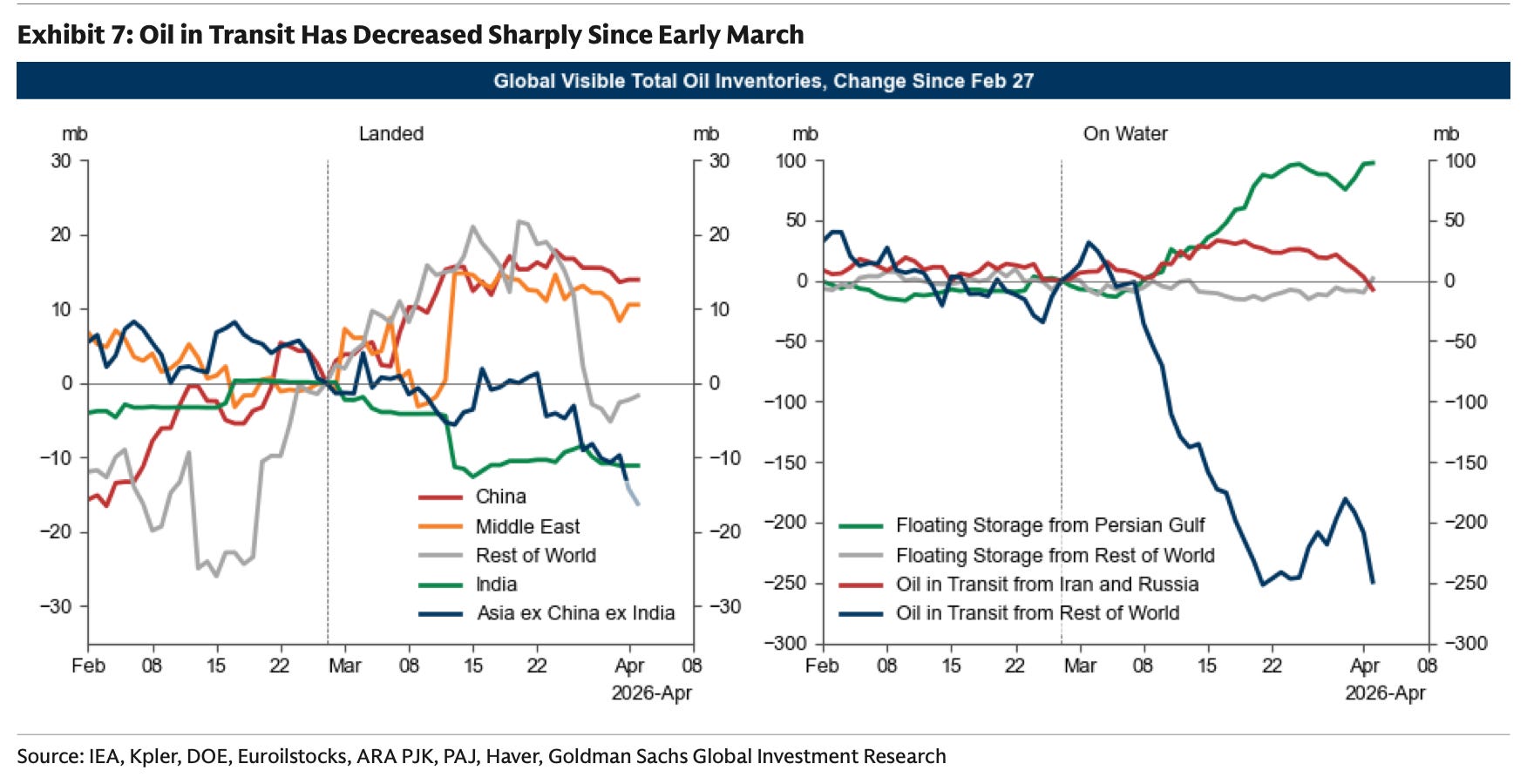

For the time being, inventories are draining from oil-on-water first as the physical air pocket increasingly impacts other regions besides Asia. As the last oil is delivered, watch inventories on land drop precipitously. We’d expect to see product stocks fall first, and then eventually crude. For some OECD countries like Japan, they’ve already stopped publishing data on product inventories, which tells you a lot about the direction of their reserves already. Europe is next.

Sum it all up right now, and the charts don’t look that bad. The issue though is its early stages, and the data lags a bit. We’re most definitely hemorrhaging inventory here, and it’s only just beginning as the Western world will begin to see the impacts this coming week. The data’s starting to trickle in, but doesn’t fully capture the lost barrels. The irony is that the US, whose actions are causing the closure, will feel it last and likely feel it least. Inevitably though, energy is a global commodity, and despite being a net exporter, US prices will catch-up.

We believe the oil price curve is completely mispriced here given the duration and quantum of outage. A $5/barrel bump at the back end of the curve doesn’t adequately reflect the lost barrels. If anything, the minor bump represents hopium that immediately after reopening we return to past.

We completely disagree. Geopolitical uncertainty, inventory depletion, and supply balkanization/uncertainty moving forward means longer-term oil should be somewhere near $90/barrel even if the war were to end today. Given that it is not, and on track for another 2-3 weeks?

Expect triple digit prices to stay. Especially if the US does send boots on the ground (our base level assumption), and their stay isn’t short (also our assumption).

So price oil at the back end at $70/barrel (and energy equities too)?

We’ll see you on the other side of that trade.

God Bless America and our troops.

short-term pod\hedge traders cannot career-wise afford to miss any weekly trump spike up regardless of contradictions, and are masking reality.

although dismissed by some credible energy experts, the IEA has simply stated the current impact is volume equivalent to the past 3 major energy shocks COMBINED.

it is critical to separately analyze the 3 phases of a trump daily victory claim :

- will he make a claim? (mostly irrelevant)

- will media promote it effectively? (mkt sentiment)

- what is the time-lagged reality ? (one's own money)

Thanks.

I've read ton of stuff, podcasts too. You are right.

Also, I would say a unilateral TACO = Abandon the Strait = Impossible. Why? Because:

1. Trump admin loses publicly. They can't spin it as a win.

2. Trump loses his position on all future negotiations (China, EU, etc). This is so important.

3. Yes, abandoning an important / critical choke point is no no :)