OPEC+ Cuts Production: Detoxing with the Sheiks

October 7, 2022

Feel that?

Them’s the shakes.

The body aches, the quivers . . .

. . . the cold sweat.

Detox.

Ooooh, this is rough.

Painful.

After more than a decade of easy money, funding pie-in-the-sky dreams, we finally crashed after a weekend bender filled with delusions about universal basic income, cryptocurrency, NFTs, and the supremacy of SaaS as a business model.

I own nothing tangible, nor do I need to.

My apps will feed me, bathe me, and walk me.

I’m free from the physical constraints of reality because if I think it, I am.

Little did we know that those dreams and our suspended reality were all powered by excess liquidity, the endless resource digitally printed by the world’s central banks.

Now the liquidity is wearing off, and now we’re financially detoxing.

Now it hurts.

It hurts as everything gets more expensive, and it’ll hurt as we’re now forced to choose. No longer is everything possible in a world increasingly filled with constraints. Scarcity drives inflation, and in turn, inflation is putting easy money, our drug of choice, out of reach.

The physical disciplines the financial, and it’s a stern teacher. So this is all playing out now, and we’re watching it closely. We’re watching the bipolar market swing between despondency and hope, the days dictated by whether we think the Federal Reserve will pivot . . . or not.

We think they will because it’s bad.

The shakes that is. It’s so bad that our teeth are chattering and if it gets bad enough, the shaking will break things. Eventually. Not now though because we’re still groaning, which means we’re just starting to experience the pain. No real damage yet, but that’ll come because this is detox, and detox is supposed to hurt.

You didn’t think the drugs were really free did you? Oh sorry . . . you did.

OPEC+

Speaking of the sheiks. We sure had a doozy of a news story this week.

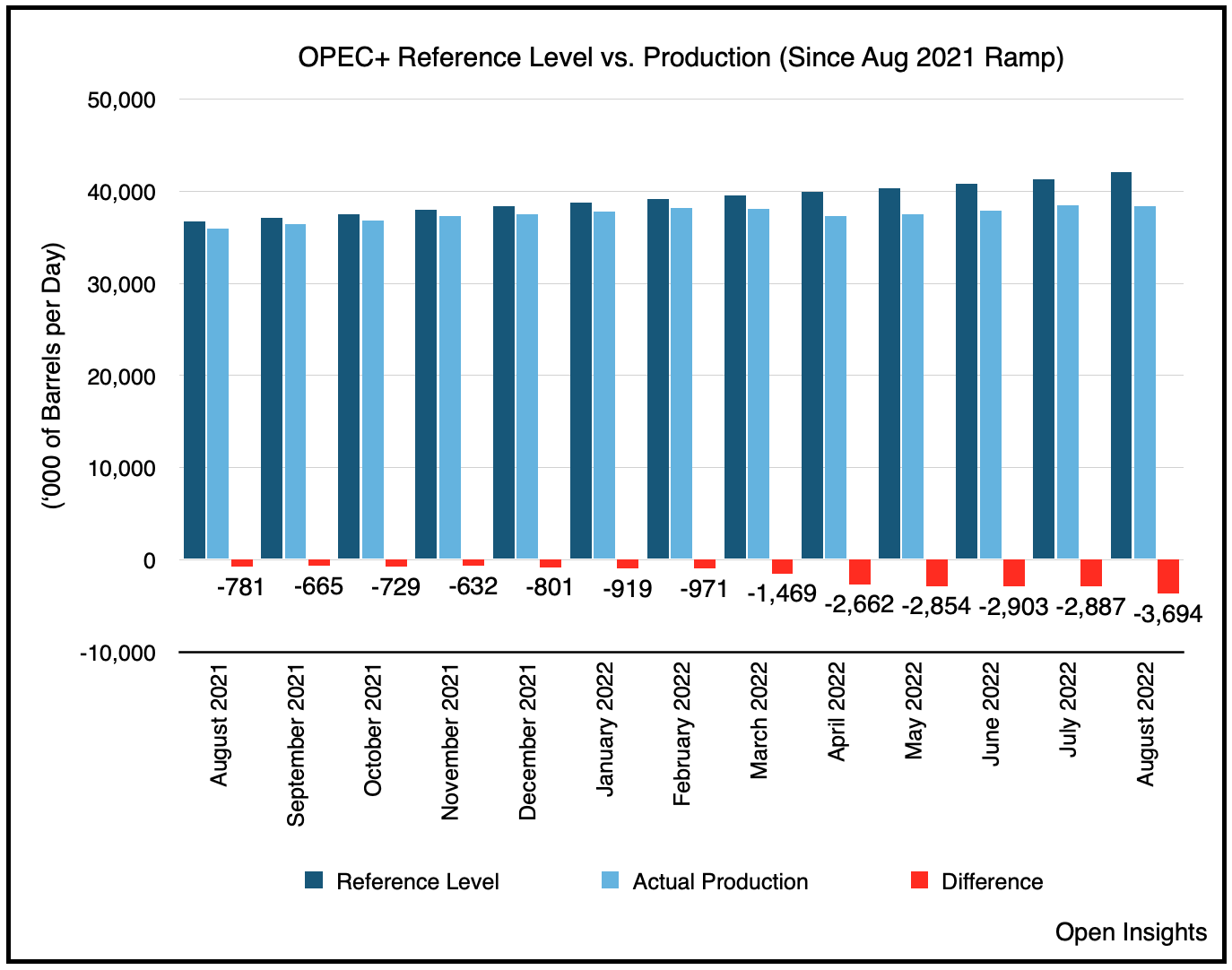

Whoa . . . them’s a lot of barrels. Okay, let’s step back a bit. Global demand is about 99-100M bpd, OPEC+ produces about 47% of that, so give or take 47M bpd. Each member has a production quota (a figure they can’t exceed) to control the amount of supplies flowing into the market, and for all intents and purposes only Saudi Arabia, UAE, and Kuwait (“Big 3”) are producing anywhere near what their quotas allow. As an entire group, they’ve struggled mightily to meet their own goals.

Although the quotas were set artificially high (implemented during the early turbulent days of COVID to stem oil’s free fall), it’s fairly obvious that today’s production levels are fairly close to most members’ maximum output.

In the end? Only the Big 3 have any material capacity left to give. The 2M bpd that OPEC+ decided to cut, is a cut to the quota and not actual production, and since essentially only the Big 3 actually produce near their quotas, only about half of the 2M bpd “quota cut” will translate to a “real cut.”

Still 1M bpd. That’s real, it’s a significant chunk when crude inventories aren’t building when they should.

What’s even more surprising to the market is that this cut will extend to December 2023.

Yes, one whole year.

This is a stunning development because although it allows the Big 3 to preserve spare capacity in the event demand spikes or Russian sanctions actually do work, OPEC+ is essentially front-running a “possible events” (recession/Russia) with an “actual cut that’s sure to happen” come November. What it also does is it removes from many Wall Street models the notion that OPEC+ will actually increase supplies in 2023.

Despite the fear of an impending recession (or it’s already here), many analysts are still forecasting oil demand to increase in 2023 as they all rely to some extent on IEA’s report.

So as they hunt for sources of supplies for their Excel spreadsheet, it’s only natural to punch in some increased OPEC+ production. Failing to do so means your supply/demand balances will begin to blow-out, making your conclusions “unrealistic,” the moniker of death for any self-respecting analyst.

Still, plug in a OPEC+ cut instead of a build, and you start to get some obscene numbers . . .

Mind you, there are some really conservative assumptions in those number too (e.g., Iran returning by H2 2023), and we encourage you to take a look at HFI Research’s excellent post.

So obviously all of this didn’t go down well with the US administration, particularly after an intensive lobbying effort in June that led to the fist bump heard around the world, one that helped rehabilitate Prince Mohammed bin Salman’s image after the Kashoggi murder. Despite the rekindling of relations, oil’s recent fall from June to September (i.e., a nearly $40/barrel decline from $120 to $80/barrel) made the Saudis reminisce about their first love, OPEC+.

The US fist bump? That meant nothing.

You OPEC+, you complete me.

Not that the US didn’t try to keep the sparks alive as they tried to avert higher energy prices heading into the midterm elections only 4 weeks away.

After OPEC+ went ahead with its decision, the White House was left fuming and jilted with only a slew of bad options that came with large unknowns and potentially many unintended consequences.

NOPEC - passing legislation that would designate the OPEC+ oil cartel an illegal monopoly. This would hand the baton to the Department of Justice by stripping OPEC+ members of sovereignty, allowing the US to sue cartel members in federal court for Sherman Act (anti-trust) violations. Whoa whoa, slow your roll there. Whole slew of diplomatic, economic and financial repercussions. Beyond just sovereignty and reciprocity issues (i.e., OPEC+ members could also pass similar laws impacting US interests in their jurisdictions), we also have financial risk (i.e., Saudi, UAE, Kuwaiti financial investments held in the US could be exposed). Do they sell US assets? Moreover, will the law have any impact? Would it simply drive the cartel underground and use diplomatic back channels to collude? Would the US use wire intercepts of diplomatic conversations to prove it in court? Would the legislation even have any impact in the near term? How long would legislation and lawsuits take, etc.? Will hampering the cartel actually lead to more energy price volatility? Who’s looking out for the marginal supplies (that sets a commodity’s price) if OPEC+ is somehow weakened? So you see, NOPEC sounds easy, but the implementation, impact and unintended consequences are certainly not. Lastly, the legislation would have to be passed again by Congress and signed by the President. How feasible is that before a midterm election only 4 weeks away, and how realistic is it afterwards if the House or Senate shifts control? More questions than answers that’s for sure, which is why we think this option is DOA.

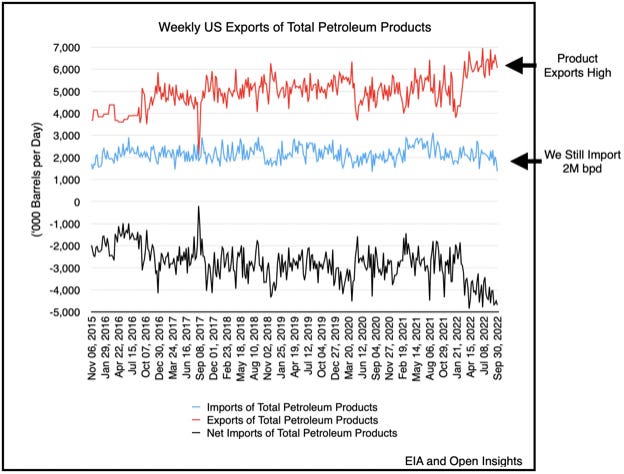

Export Ban - a ban on the export of products sounds sensible and easy. If we kept the gasoline, diesel and jet fuel at home, it’ll keep the barrels cheaper. Yet that presents huge challenges as well. The US exports nearly 6M bpd of products, so capping or eliminating the product exports would immediately spike prices overseas.

In turn, the ban would shut-in certain refiners as the export market would no longer be a release valve for products refined in the US. Once the refineries are shuttered, upstream producers that feed crude into the system would also have to reduce production as WTI falls in price. Some US customers in the East Coast will also ironically experience a price increase as products refined overseas will now be more expensive (as customers outside of the US bid-up the remaining products to cover the lack of US exports). Again note the chart above, we still import 2M bpd of products, so if we remix the pot of liquids, we’ll definitely get a taste of the consequences. So you see, export ban sounds great, but the outcome could actually worsen the US quandary.

SPR Releases - after declaring a 180M barrel release from the SPR in March, US crude inventories are near all-time lows.

The SPR isn’t a persistent source of supplies, and as we continuously tap into it to relieve increasing prices, we’re leaving our safety blanket threadbare. As of today, SPR inventories have declined to 416M barrels, but it’s set to fall by another 20M. Thereafter, Congressional sales mandated for ‘23-’27 means another ~200M barrels will be sold, leaving only 200M barrels left, which is insufficient to cover the IEA’s requirement to maintain 90 days of net oil imports in reserve (i.e., for the US ~2.7M bpd of net oil imported * 90 = ~250M barrels). Eventually the US will buy-back these barrels when market conditions permit, but that likely won’t be in the near future as we anticipate supplies to stay tight in the coming years. At this stage, further draining the SPR (i.e., more than the already announced 180M barrels, and announcing it prior to mid-terms) will invite louder criticism from Republicans, something the White House is unlikely to welcome this close to election. The pantry is getting empty, and the emptier it gets, the more obvious it becomes.

Ultimately, none of the choices above are attractive, every one of them has trade-offs and many of them may not even lower prices in the near-term and certainly not before midterms. Given the few remaining weeks left, we anticipate the White House’s actions will be more form than substance.

They’ll try and pivot the message, and talk-up the previously passed Inflation Reduction Act and the $270B of energy tax incentives.

Re-run/repeat the already previously announced 10M barrel SPR release for November.

Allow Congressional members to talk about the NOPEC legislation.

Emphasize that oil prices haven’t risen dramatically since the announcement (Amos Hochstein, White House Energy Adviser).

“The decision hasn’t had as significant an effect on prices as the White House expected, Hoschstein said earlier on Thursday.”

The key to all of this though is to stall and hope oil prices don’t inflect dramatically/materially before midterms. Although oil prices have crept higher from the low-$80s to the high-$80s since the OPEC+ announcement, they’ve yet to cross the $100/barrel “media” headline threshold.

Recall when Biden went to Saudi Arabia in June, WTI was over $100/barrel. With the market’s concerns about a global recession, we’re still below that, and if the administration can wait, they may not need to act so hastily. For now, we believe they’ll slow-play the consequences/reactions to the OPEC+ decision, or backstage them. The real repercussions may be weakening security cooperation and/or other diplomatic, non-oil related actions given the US’ lack of leverage in the energy space.

In truth, by not incentivizing domestic/international producers to step-up and continuing to excoriate the energy industry for political gains, we’ve effectively ceded control of our energy security to countries that are unsympathetic to our interests. As today’s energy scarcity plays out, expect more of this, and expect our helplessness to continue. While we may loathe our thirst for fossil fuels and those who provide it, our dealers know the reality . . . we’re hooked.

So let the shakes and the sheiks, continue.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

thanks, very article - as always.