Our First Newsletter

July 26, 2020

Welcome to our first newsletter. Why are we writing this? Well throughout the week, we’re often asked about our opinions on various topics, the machinations of the market, our outlook on a particular sector/industry, and our views on certain stocks. This letter is a building block for a new service we’re offering, one that will be open and initially free for those interested, and later enhanced to provide additional information/insights. This service is effectively designed by us, for us. It’s the service we wish we had when we founded our funds years ago. Something that centers us with a weekly overview and then gives us a specific snapshot of what’s happening throughout the week and what’s to come.

More importantly, it will attempt to answer the questions you pose directly. We’re looking to understand what you’re curious about, and then in articles, chat rooms, direct communications and podcasts/videochats, we’ll provide our insights. The service will be a collaboration between the fund managers who’ve agreed to contribute and you, our partners, because after all it’s a service for you.

Week Ending July 24th

The market’s flat now, or pretty close near it. Frankly a remarkable turn of events from where we were at just a few months ago. From the very lows reached on March 23, to today, the market, as represented by the S&P 500 has recovered over 41%, erasing the nearly 32% decline from its previous high reached on February 19 to March 23.

Let’s distinguish between YTD (year-to-date) from RTD (recovery-to-date). What’s the best performing sector YTD? Tech (Table 1). No surprise there as robust numbers (earnings) and an attractive narrative (growth story) coupled with the unleashing of liquidity has powered that sector above all others, which will arguably face greater headwinds as the real economy suffers and recovers from COVID. What’s the second best? Consumer discretionary, up 8.4%, helped by Amazon’s 64% rise YTD, and Home Depot and Lowes, who’s “essential” stores have remained open throughout the pandemic. On the flip side, we have the laggards. Energy, still down around 40% YTD after the pandemic and OPEC+’s ill-timed price war halved that index from peak to trough. It’s recovered >60% since the lows, but still leaves much ground to be regained.

What about RTD? From the market high reached on February 19 to the market low we saw on March 23, what’s recovered the most since that crash? Would you believe homebuilders? The low interest rates and homebuilder discounts has sparked a wave of buying (the homes and stocks), which many believe will continue. (Table 2). As the 10 year Treasury continues to stay near zero (0.59% as we write), expect mortgage rates to also stay below 3%, which bodes well for new home buying in the coming year as we recover. This is just another indicator of the widening spread between the have and have nots in the country.

The Senate’s Back in Town

The Senate came back in session on July 20, which effectively restarted the work on the follow-on COVID recovery package (“CARES II”). This sequel will purportedly top $1T, and we’d anticipate that the final reconciled bill will be somewhere between that figure and the House version, which scored at $3T. Given the expiration of the enhanced federal unemployment benefits at the month end, the clock is ticking. It’s not a matter of if a bill will be passed, but how much. A trillion here or there, and we’re talking real money. We’ll dive into the bill when more detailed versions are released later.

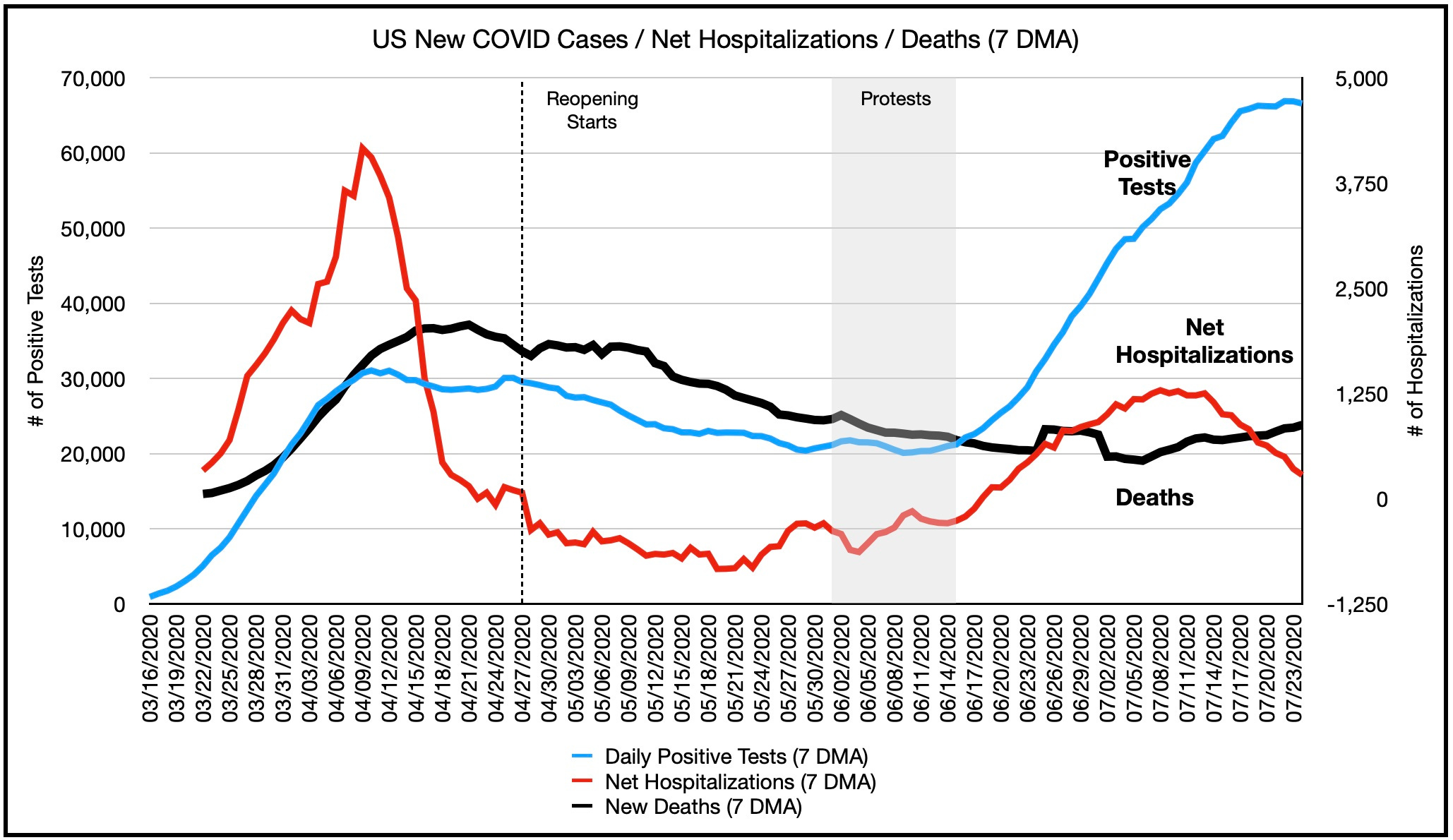

Eyes on COVID

As Congress works on loading the helicopter with money, we’re looking at COVID data and thinking . . . this pandemic may end faster than many anticipate. Looking at the most recent trend lines, something is becoming more clear daily. Net hospitalizations, the number of patients being admitted into and discharged from hospitals for COVID are falling. The tsunami of patients that hospitals saw are slowing to a trickle, and in some states, the water has begun to recede.

Now note that the overall numbers of hospitalized patients are still increasing, but the rate is declining. It’s the difference between filling-up a swimming pool (i.e., hospitals) with a garden hose vs. a firehose. If the strain on hospitals and health care practitioners lessen, with adequate planning they won’t buckle. Our Three Gorges dam hopefully won’t collapse.

The End is Near . . . Just Not the One You Thought

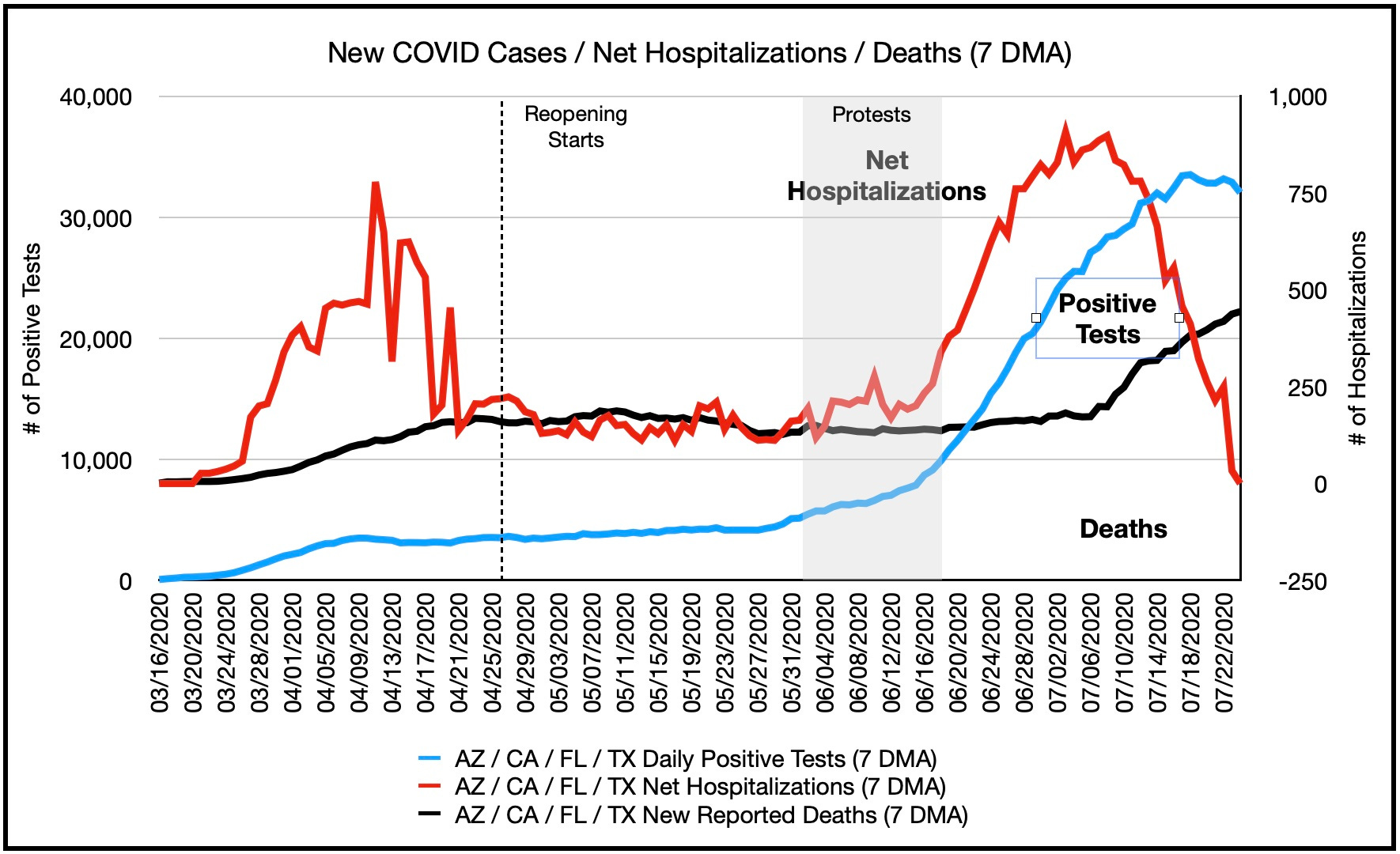

It’s not just in the overall US picture that we’re seeing this trend, but importantly also in the “hot spots,” the states that have borne the brunt of the spreading pandemic. Arizona, California, Florida and Texas, collectively have seen a dramatic decline.

If positive cases/tests are exploding (and no doubt they are because the pandemic was allowed to spread effectively unchecked), then hospitalization rates should not decline if the severity is intensifying. Yet, it’s not, and as the patient demographics expand, we’re seeing that SARS-CoV-2, the virus that causes COVID, isn’t as deadly for younger patients who are infected. As you’d expect, those who are younger/healthier are able to better weather the disease, thus reducing hospitalizations, length of stays, and deaths. Therefore, we believe hospital discharge rates will actually accelerate. The massive inflow of hospital patients have been younger, which means as the outflows continue, the hospital turnstile will spin faster.

If Arizona is any indication, California, Texas and Florida will also soon dip into the negative, and the hospitals will be emptied. As that occurs, the narrative will shift.

The media will be the slowest to shift. After having emphasized positive tests as the leading indicator for so long, the narrative has been consistent . . . the flood is spreading. We’ve contended all along that positive tests are a lagging indicator. Once the tsunami crashed unchecked, we’ve been on the road to “effective herd immunity”. So like New York, hospitalizations will be the first to crest, then positive tests will plateau (as those susceptible to infection will have already been infected), and lastly deaths will follow. For the media, if the positive tests no longer carry the narrative, it will likely shift the focus on deaths per day, which should increase just based on how hospitalizations initially increased. Deaths, however, are the ultimate lagging indicator and in the end that number will fall just as hospitalizations fell (unless you believe more people will die at home from COVID than at hospitals).

Meanwhile, business and community leaders will place increasing pressure on governors to reopen and that pressure will collide against conservatism because having already been criticized for “reopening too early” leaders will naturally hesitate. Who’d want to risk a rebound in cases? The first rebound was largely the viruses’ fault, the second yours. So if hospitals begin emptying rapidly in August as we anticipate, by late-August, early September, we believe governors will begin reopening. The Congressional CARES 2 package may temper this pressure (by incentivizing people to stay unemployed (IF) the enhanced federal unemployment insurance (on top of state) is renewed), but as we’ve seen in the state data, people are eager to get back to work despite the added benefits. Nonetheless, overall, we think late-August / early September is the timeframe if COVID abates, which is months in advance of what the market is anticipating. Thereafter, we’ll be in tepid recovery, as cases remain low and people adjust to the “new norm” and wait for the vaccine.

Feigning Leadership for Credit = Marketing

It’s one of the reasons why we think the Trump administration restarted its coronavirus updates again this week. After months of political abdication (i.e., shifting the political responsibilities and the blame of dealing with COVID to state governors), the administration suddenly reversed itself and restarts briefings? The timing is suspect, unless you also see the trajectory of net hospitalizations. As those fall, the water recedes, and guess what’s next? Positive tests, the main figure the media focuses so heavily on. So start the briefings again. Advocate for masking, call it patriotic. Talk about vaccines and the progress made, because why not? The pressure from the hose is falling, and when the water ultimately recedes, someone will claim victory . . . and why not him? He’s never been shy about claiming credit where credits not due.

Join the Distribution List

So that concludes our first letter. Well endeavor to send these out weekly, so if you would like to be added to our distribution list, please click on the subscribe button above. This is our start and it’s our invitation for you to join us and share your thoughts. Welcome to Open Insights and let the conversation begin.