Our Intern Makes Lemonade out of Lululemon

June 29, 2025

As we’re apt to do for the summer, we tend to hire summer interns. It’s a great way to pass on some of the things we’ve learned, inject a fresh new view into what we do from someone young, and get a bit of help on a few odds and end. For this summer, Open Square welcomes Matthew Nakagawa, a rising sophomore at the University of California, San Diego. Matt’s majoring in Business, and looking forward to a career in accounting and finance. No better way to start in the field.

OSC: Hi Matt.

Matt: Hi.

OSC: So what’ve you been working on?

Matt: Well my first summer project was to take a look at lululemon. lululemon athletica, inc. (“lululemon”) to be precise. All lower case letters because according to Chip Wilson, its founder, that’s indicative of a “relaxed” vibe.

OSC: Already hate it.

Matt: Haha, it’s not that bad.

OSC: I’m too old for this, but still let’s get on with it. In my mind, this is an interesting company because it’s the “cooler” version of Nike. Originally geared towards yoga, pilates, and women’s fitness, it’s taken the world by storm in the past decade and branched out. The stock rocketed back about 10 years ago, and then continued to climb as we stayed at home during COVID. Recently, though you can see, it’s flattened out, dipping in 2022 as the broader market sold off, regaining those losses, and then tumbling to the $235/share level we see today.

So what gives? What’s happening?

Matt: Well this is a $28B market cap company, based in Vancouver, Canada with no debt, and $2B of cash on hand, giving you a $26B enterprise value.

OSC: Not bad . . . eh?

Matt: Terrible joke. The CEO, Calvin McDonald, who joined in 2018 after a stint as the President of Sephora, doubled revenue from $3.3B to $6.3B from 2018 to 2021. Then in 2022 put in place the “Power of Three x2,” a strategy to effectively double revenue again from $6.3B to $12.5B in 5 years (i.e., by end of 2026). We’re now in fiscal year 2025. lululemon does that and they’ll have a CAGR of nearly 15% per year. It’s slower than the original mid-20% CAGR from 2018 to 2021, but lululemon was also a much smaller company.

So what’s the Power of Three x2? Well according to lululemon’s press release in 2022, it’s “doubling down on the core drivers of success: product innovation, guest experience and market expansion to achieve $12.5B by 2026.”

OSC: That’s a lot of tex, summarize it for me Matt-GPT.

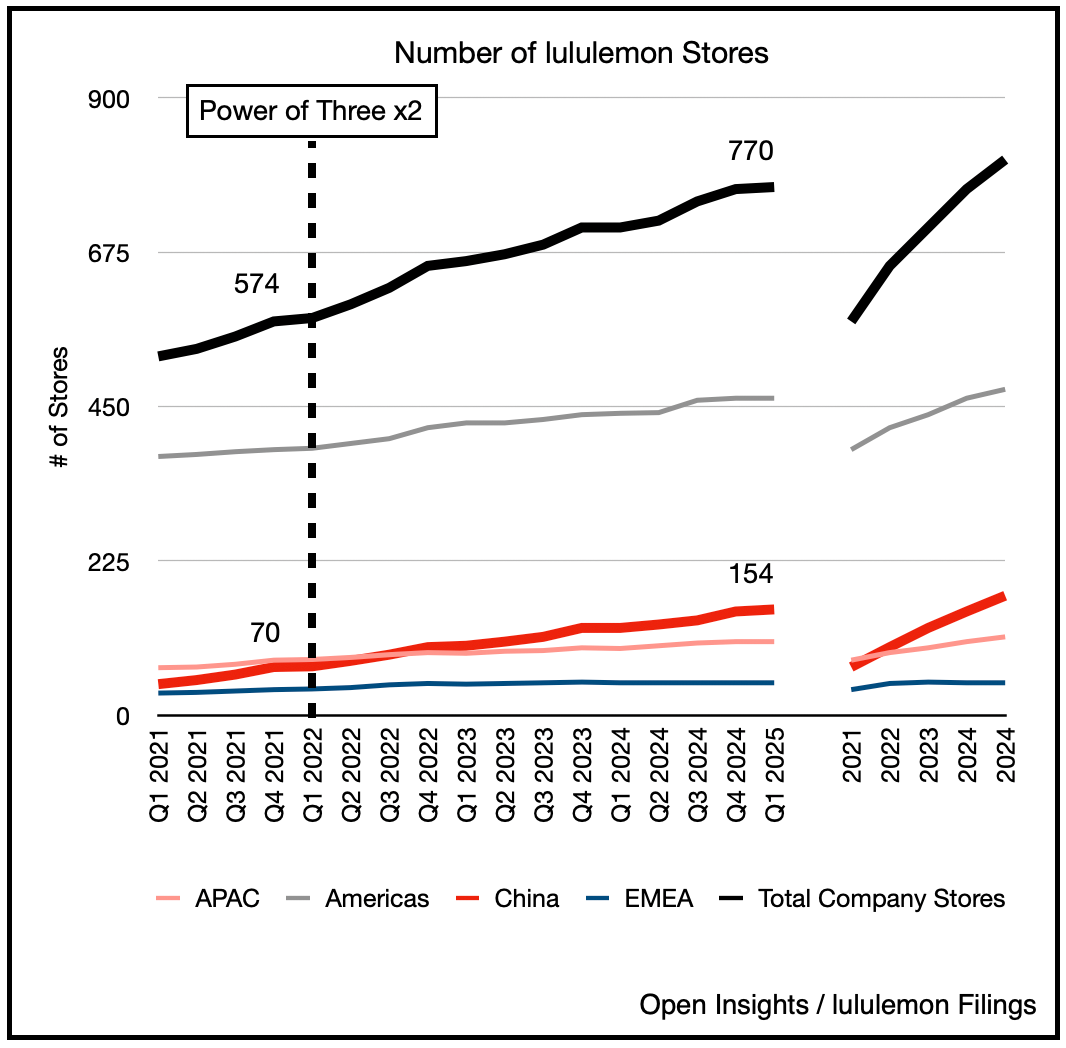

Matt: Stores . . . add lots and lots of stores.

You can see the tremendous growth since the beginning of that Power of Three x2. This is a retailer, and you can see they basically added nearly 200 stores in the past 3 years (i.e., growing from 574 stores to nearly 770 stores by the end of 2024). Nearly 40% of those stores were opened in China. The number of US stores also grew steadily, whereas Asia Pacific (“APAC”) and Europe, Middle East, Africa (“EMEA”) were flat.

OSC: So this is essentially a US and China story?

Matt: Yes.

OSC: Big difference in the GDP per capital between a US yoga practitioner vs. a Chinese one, no? Like one makes an average of $75K vs. another making $13K. lululemon gear is expensive . . . isn’t that “stretching” their budget?

Matt: Yoga puns, fantastic. Moving on, let’s see how much each of their stores earn. Let’s take the revenue by geography and divide it by the number of stores in the quarter or average for the year, for each region/country.

As you’d expect, US stores sell the most every year. You can also see the “spike” in sales during the holiday and New Year quarters.

OSC: Ah, seasonality. Get those New Years resolutions in place.

Matt: Yes.

OSC: lululemon sells online too though, so what’s that look like by region?

They don’t break that information out by region, but we can see that lululemon generates 45% of its revenue from stores, 45% from online sales, and 10% from wholesale. Those figures have been pretty consistent as they grew. We’ll assume that the stores are the drivers of the overall sales, and the more stores there are, the larger lululemon’s presence there is, in turn leads to greater customer awareness.

OSC: That’s fair for now, or until the company breaks out the information in more detail. So it’s a flywheel, plunk down more stores, raise brand awareness, and see e-commerce rise as well?

Matt: Yes, and overall not as many people outside of the US is aware of lululemon yet.

OSC: I see in their conference call transcripts that they hype up their brand ambassadors opening new stores.

Matt: That’s part of their “activation” process. Their “ambassadors” (spokespersons like Michele Yeoh, Lewis Hamilton, or Kendall Toole (formerly Peloton)), will appear and “activate” a newly opened store, generating local interest and free press/media to drive awareness. lululemon also sponsors Formula 1 events, fitness days, etc. in the countries/locales/demographics its targeting. With the Power of Three x2, there’s particular emphasis on Chinese events.

OSC: So let’s step back a tad. This $26B company has grown revenue from $3.5B to ~$10.6B as of 2024, quite the feat.

The stores in the US and China do most of the heavy lifting, as your chart above shows. US stores generate about $18M a year (and again that includes e-commerce and wholesale revenue mashed into it), China stores about $10M, and everyone else about $9M . . . how much of that do they keep?

Matt: Well after factoring in costs (including adding back corporate expenses, which they like to back out), we can see that they keep about a quarter of every dollar in revenue in the US and China, and about half of that (i.e., 12%) everywhere else (EMEA and APAC (“Rest of the World” or “RoW”)).

OSC: So a US store that generates $18M in US sales translates to $4.5M in operating profits. $9M in sales for a store in China, then about $2.5M in operating profits.

Matt: Yes, so same profit margin, but US stores sell twice as much and keeps about twice as much.

OSC: Still the Chinese sales growth per store is surprising, as is the ever increasing profitability. That’s hard to do as you add new stores, increase “same store sales” and increase profitability. You’d think that normally as you add stores, each location is less ideal, and hence less sales, lower profitability.

Matt: Exactly.

OSC: So where does that get us?

Matt: Well for 2024, this company generated $10.6B in sales, which led to ~$2.3B in operating cash flows. Less $0.7B of capex, you have free cash flow (“FCF”) of ~$1.6B. So basically a $26B company generating about $1.6B in FCF, for an earnings yield of ~6%.

OSC: It doesn’t sound super compelling, but to your point, it’s growing from 770 stores every year by about 40-50 stores per year. Take capex less depreciation/amortization and it looks about half of that $0.7B in capex is for new stores. Said another way, it costs around $5-6M to open a store (think signage, inventories, shelves, interior decorations, etc.), and each store kicks off profits of $2.5M in China and $4.5M in the US.

Matt: It’s probably cheaper to open a store in China vs. the US, but yes, that’s what it looks like.

OSC: So based on that if I’m focused on growing my Chinese stores, there’s a bit of a lalapalooza effect, where it’s a flywheel. Increased awareness boosts same store sales, and overall profitability, and the deeper awareness gives me more opportunities to open more stores.

Matt: Yes.

OSC: It does look like growth though is slowing down. Are they going to hit their Power of Three x2 plan to get to $12.5B in revenue in 2026?

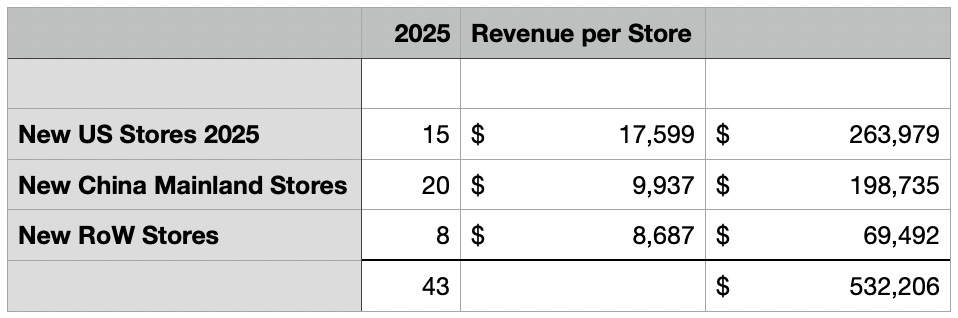

Matt: If we project it out, they’re targeting $11.3B in sales this year, but tack on another 40-45 stores by the end of the year (15 in the US, 20 in China, and call it 8 everywhere else), you’ll get an additional $0.5B in full year sales by 2026 for these new stores, getting you to $11.8B.

You figure they’ll then add another 40-45 stores in 2026. Tack on some small growth from existing stores, and yeah $12.5B by end-2026 is plausible, and in fact likely.

OSC: Okay so they hit their plan, if we then take a look after 2026, we can say that at their 40-45 store pace, you’re looking at $0.5B of incremental sales every year and $120-130M of additional cash flow if we assume the same mix. Run that out for 5 years to say 2031 and assume that lululemon grows revenue only modestly from existing stores (and assumes almost all of the growth comes from adding additional stores), we get about $15B in revenue by 2031. If we assume 25% of that falls to the bottom line, we’ll get around $2.7B in FCF for a company that you can buy at $27B in enterprise value today. Seems fine but cash flow is basically growing at a 6% or so rate per year, not super compelling.

Matt: They’re shrinking share count though, so per share cash flow rises.

OSC: Oh, it looks like they’ve really started repurchasing their stock in 2024.

Matt: They retired about 4% of their common stock, spending $1.6B for 5.1M shares in 2024.

OSC: Lets think here. Diluted shares declined from 127M to nearly 123M today, and the company continues to repurchase shares even last quarter. So grow the top line by 5-6%, and shrink the share count by 4%. Like growing the pizza, and reducing the number of slices. Each investor’s slice gets bigger. We like that. The combination of the two will lead to cash flow per share increasing by nearly 10% every single year.

I guess you could say the stock is cheap in this market. At $230/share, the valuation has definitely come down materially from the stratosphere of yesteryear. FCF per share is what we tend to look for, and despite the headwinds we’re seeing (tariffs, slower economy, etc.), the lululemon management team appears to be getting their arms around it and quantifying it. If tradewinds abate, the bad news can be considered baked in, as the company pivots to a new fashion line rollout (Align with No Line (my wife says it’s leggings that do not have a front seam, and that is a good thing apparently)).

It’s also an interesting way to play the China market, and the growing appetite of the consumer there as they embrace athleisure wear and health and wellness. Also, a bet on lululemon would be a bet that the management team can continue to execute. We think it’s likely they’ll achieve their 5 year strategy by 2026, and thereafter, they’ll come up with something more compelling for shareholders to look forward to (i.e., a new 5 year plan). The recent downgrades and price declines were largely because of margin issues (tariffs impacting COGS, etc.), and shouldn’t have garnered such a harsh response (full year operating margin is guiding to only a 1.6% decline). The $180M dollars of lost profits due to higher tariffs has resulted in a $16B hit to the company’s value (i.e., the stock is down 37% YTD). 89x multiple on that tariff hit we guess. Such is the market. We think a recovery back to $300/share should be achievable as trade sentiment calms down, the company finds some work arounds for its supply chain, and raises prices to pass along the costs of Liberation Day.

Longer term though, as growth has come down, this company is maturing, but maturity should also mean greater cash flow, and a higher return for shareholders (vs. solely relying on capital appreciation). This might be a good pivot point for an investor to start enjoying both. At worst, modest growth on the top-line, while share count shrinks which improves per share cash flow. Using the same multiple, the stock likely doubles in 5-7 years . . . as a base case. Even better though, there’s a bit of a cheap call option on China’s longer growth term, and for the possibility that management finds a way out of the trade morass and into new endeavors. This is a team that’s doubled revenue in 3 years (2018-2021), and is set to double it again in 5 years (2022-2026). If growth reignites, then the stock can quickly rerate back to its high. There’s runway ahead, after all Nike has 5x lululemon’s sales and 4x the market cap, so there’s room for growth and/or market share . . . in this market.

Now that would be a truly “transformative experience.” Great job Matt and welcome aboard.

Matt: Thanks!

Please hit the “like” button and subscribe if you enjoyed reading the article, thank you.

Cool format for presenting a investment idea. Cheers!