Our Q2 2026 Letter & Look Ahead: Bedlam

July 18, 2026

Dear Limited Partners,

The US / Iran War never happened. You think it did, but it didn’t. We didn’t stop global oil production for over three months, deplete inventories at an unprecedented pace, or disrupt and throttle oil flow for 20% of the world’s energy supplies. We most certainly didn’t empower and reinforce a militaristic theocratic Iranian government hell-bent and motivated on destroying its adversaries. We also didn’t gaslight the world into thinking that after this debacle? . . . it’ll be fine.

We did, however, manage to stop the turmoil for a few weeks. Under a hastily concluded Memorandum of Understanding (“MOU”) on June 17, the two warring parties crafted a 14 bullet point agreement. The US’ crack team of negotiators (i.e., Kushner and Witkoff) settled on a strategy of “performance based” economic inducements. If Iran takes specific actions, the US would reciprocate with commensurate economic relief. Leave it to two financiers to solve everything via money and promises of economic prosperity, after they’ve killed the Ayatollah’s family no less. Tough sell, so be wary of the hand that offers gilded gifts, when the other wields a knife.

The MOU effectively created a dètente, which allowed the US to catch-its-breath, refill its quiver, and calm the markets. The Iranians used the respite and the temporary lifting of the US blockade to sell down trapped oil inventories. Around 80M barrels of Iranian oil exited the SoH. Once drained, the shenanigans restarted. Neither side trusted each other, nor were they truly committed to what was in that document. How could they when their political positions were diametrically opposed. Iran effectively promised control of the Strait of Hormuz (“SoH”)? How does that work if the US petrodollar depends on its ability to protect its Persian Gulf allies and control the waterways? So when Iran began closing the strait, the US balked. What was written on paper became all too untenable in reality.

So conflagration spreads as the US and Iran exchange fire. It’s a war between the world’s greatest superpower and an impoverished and isolated country armed with drones and ballistic missiles. Effective as the strait remains blocked. In normal times, we’d expect oil prices to be over triple digits, but through relentless jawboning, the administration’s kept prices rangebound. Every time prices crossed triple digits, a well timed social media post, or leak to a media proxy like Axios, have wrestled pries lower. At this stage, you have the traders’ rapt attention and capital. Given the volatility, few investors can hold any long commodity position. Especially not in the short-run, so open interest has plummeted and short-interest has soared. If the administration won’t let prices rise, then we’re left with the physical market to force it higher. On that front, the increasing pressure stemming from falling inventories have been slower than expected. China, one of the largest oil importers, reduced imports by a staggering amount, instead cutting refinery runs and drawing inventories to avoid buying in a tight market. This, coupled with the release of Strategic Petroleum Reserves (“SPR”), has prevented prices from spiking.

Still these are patches though, bandaids on bullet holes. The SoH remains materially disrupted, and production losses pile on. The reimposition of the US blockade will worsen the situation, and the +1B barrels of production already lost will rise. The US has suppressed oil prices by gaslighting the market into complacency, but do so long enough and the physical market can crack violently. Make no mistake, a choked strait now becomes a stranglehold, and we’ll find out who’ll tap out before the world’s energy resources tap out. Iran knows this and it’s very resilience can threaten the world’s demise.

Oil Demand & Oil Supplies

What a tumultuous quarter. What was off is now back on. A war begun on February 28th that was supposed to have ended quickly, is turning into another Middle East debacle for another US president. Though lasting for over 100 days, the fighting came to a standstill when President Trump realized there likely was no quick end . . . and that the US was losing. Fortunately for the world, if not oil bulls, this war has carried little scar tissue so far, at least on the oil pricing front as the administration incessantly jawboned an impending ceasefire was around the corner. In the past 3 months, an imminent peace deal has been announced nearly +25x. Many of these announcements were met with an oil selloff as the risk premium bled away. Accordingly, this meant few market participants could hold long bullish positions even if the SoH remained disrupted.

So yes, while there was a real material physical disruption, few could bet on it given the price volatility.

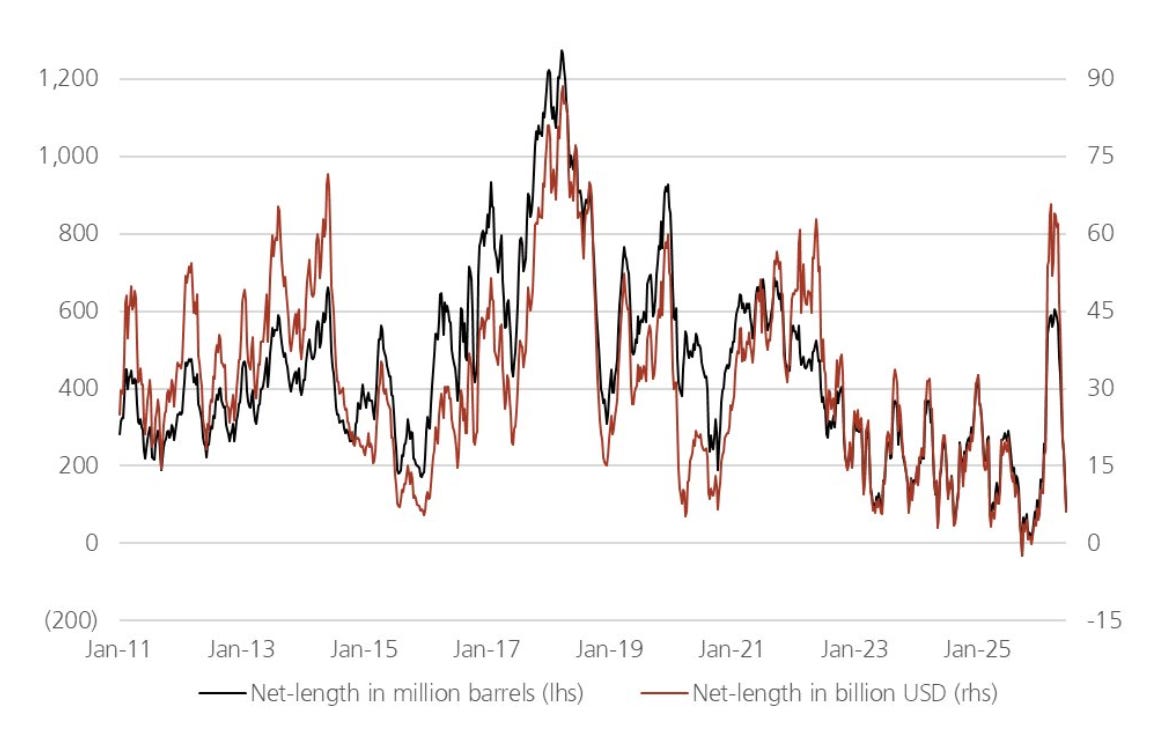

Eventually, the MOU was signed on June 17th so this entire misadventure came to a quick end, or so the world thought. +100M barrels of trapped crude immediately gushed out of the Persian Gulf, and oil prices plummeted as investors mistook the sugar rush fora super glut. Consequently, bearish positions increased markedly, eventually eclipsing any semblance of rationality as they reached near-COVID levels. Here’s Giovanni Staunovo’s chart at UBS, showing the absurdity.

With the paper market dipping to COVID levels while the SoH remained disrupted, it makes us wonder . . . really?

The MOU brought about a 60 day ceasefire to conduct negotiations on uranium enrichment, management of the SoH, and the lifting of economic sanctions. We wondered whether Iran would exert more pressure as the clock wound down to maximize concessions from the US. Since February, Iran’s learned that it can effectively shut the SoH with drone and missile strikes, deplete global inventories reserve to dangerous levels, and push the US administration further since Trump is unwilling to stomach a prolonged conflict given market turmoil. Sure enough, the ceasefire lasted all of 3 weeks. As the US began routing ships through a southern Omani corridor, bypassing the Iranian northern corridor (the middle of the SoH is currently mined), Iran attacked. The Iranians saw the alternate route as a threat against their rights under the MOU, an attempt to diminish their leverage. In short order, the IRGC sent drones into the sides of a few vessels after which everyone declared “fights on.” So we’re trading attacks today. The US will attempt to pound the Iranians back to the negotiating table using air strikes, but unless decapitation strikes lead to regime change, we wonder what’ll change this time when 3 months of bombings couldn’t.

Looking ahead, won’t the Iranians keep the strait closed for a few more months and watch as the global economy heads towards an energy crisis? The SoH has become their nuclear weapon. It’s an economic one and everyday they retain control is another day their leverage grows. Their ultimate goals are insuring regime survival and regional hegemony, and the SoH affords them an opportunity to achieve both.

If the US isn’t willing to commit ground forces, will they be able to completely negate the Iranian threat to shipping to allow it to normalize? We don’t think so. One missile can quickly reprice insurance premiums and deter shippers from sending their ships through. Even if the disruptions were intermittent, commodity prices, which are priced at the margins, will remain elevated.

Realistically, we think the US could even concede. No tolls were charged under the MOU, but there were thinly veiled discussions of environmental, security, or safety transit “fees.” Call it what you want, but what it really is is a military victory translating to a political and economic one. Allies of Iran (i.e., Russia, China, and maybe India) will obviously receive a loyal customer discount, but expect everyone else to pay. We’re betting that something acceptable will come to fruition. We have to. Given the desperation of the Trump administration to pivot away from this debacle, they’ll likely provide almost any incentive to induce the Iranian government to accept. So long as they can sell it to the public, or their Republican base. Even if they can’t fully sell it, they’ll try to sell it enough or distract enough so that the news cycle can move on from the misadventure. Bringing Iran back into the international community by lifting all sanctions, and reinvigorating its economy could be painted as a win. Never mind that doing so empowers the very adversaries you tried to eliminate just three months ago to no avail.

Red lines that were once unthinkable will be smeared, blurred enough so that we can just agree to something . . . anything . . . so that we can all just move on. Uranium enrichment? They promise to open up for inspection, the greatest, bestest inspections. We wonder just how deep those underground caverns will become once we shower them with reconstruction funds. That’s a lot of centrifuges to buy. What’s left though is a refreshed, refocused, and rearmed IRGC whose focus will be on acquiring a nuclear weapon to solidify it’s future.

Meanwhile, Saudi Arabia, the UAE, and Iraq, will build alternative pipelines and ports to bypass the SoH in the future. The Saudis and UAE will likely complete their projects by 2027, and that should materially reduce Iran’s ability to disrupt their oil exports. Still pipelines and pumping stations are soft targets, vulnerable to attack, so even those can be threatened in any future kerfuffle.

Energetic Nonchalance

None of the above has mattered for oil though. Sure, all of the risk should’ve mooned crude prices, but instead, oil prices have round-tripped the entire debacle. There’re are a few reasons for this. First, visible inventory draws have turned out to be a fraction of what analysts (including us had anticipated). Between the +100 days since the war began and MOU was signed, global inventories have drawn ~420M barrels.

Before the war, ~20M bpd of oil and oil products flowed through the SoH. Since its closure, the Saudis, UAE, and Iraq have rerouted some of their exports to the Yanbu (+3.6M bpd), Fujairah (+1.1M bpd), and Botas-Ceyhan (+0.2M bpd) pipelines, respectively. The ~5M bpd rerouted means the SoH net exports fell to ~15M bpd. The SoH wasn’t entirely closed either as ~2M bpd of Iranian exports or dark tankers transited, which further reduced the outage to 13M bpd. The 13M bpd of net outage should’ve equated to a total of ~1.3B barrels draws, so why did we only see a 420M barrel visible, and a 600-700M barrel total draw (if we assume secondary and tertiary stocks also drew)? Demand destruction and China.

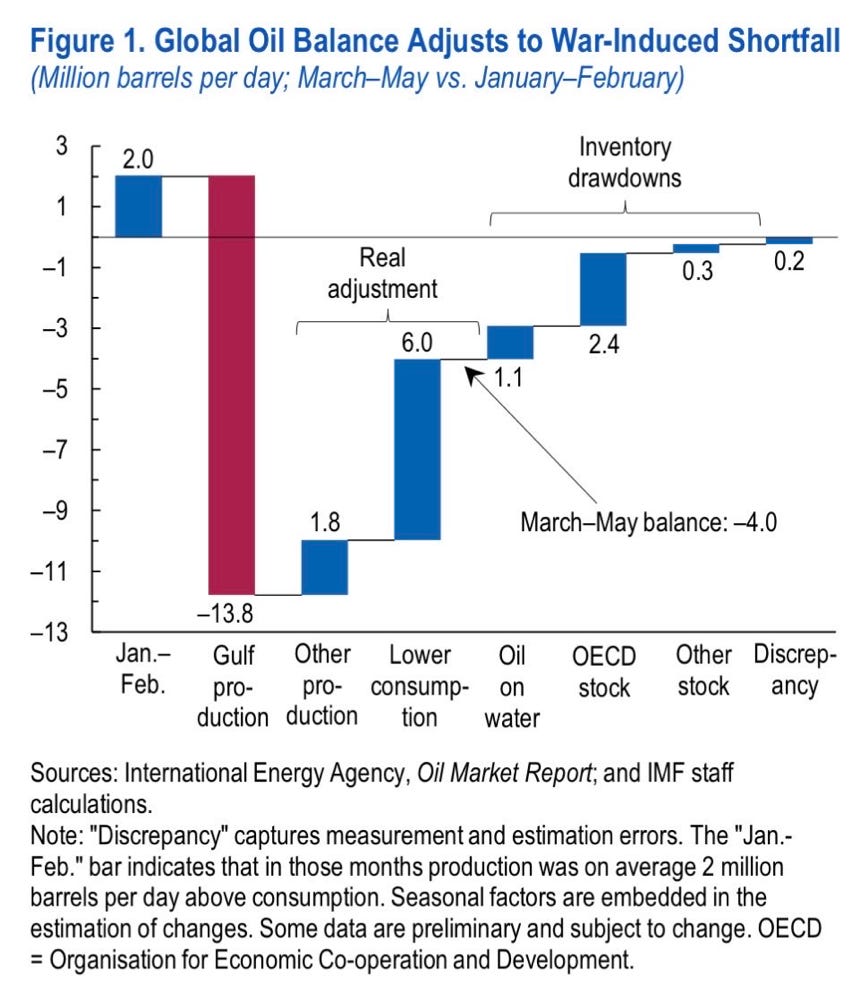

Demand destruction certainly happened not because of economic contraction, but simply because some countries couldn’t find fuel. We know from reports that things like plastic bags and low-end plastic products were in short supply in Asia. Prices of petroleum products in South East Asia also spiked dramatically, which curtailed demand in the developing markets. We estimate about 1-2M bpd of demand destruction, so 1-2% of global demand. Here’s the IMF’s take on it.

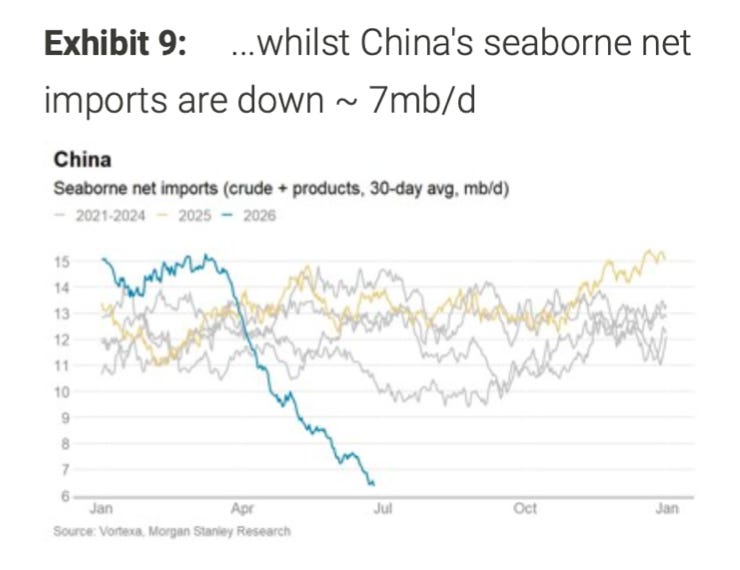

The IMF estimates that demand destruction registered ~6M bpd, but most of that figure is China, and that demand really never disappeared. For the past 3 months, China has stiff-armed and reduced imports by an average of 4M bpd. Today that crude diet has reached ~7M bpd.

It’s a staggering amount for a country that imported ~15M bpd pre-war. By reducing its intake, China’s freed up barrels for other countries, supporting global oil balances. We’re not convinced that this was done because of Chinese largesse. In fact, it’s likely a strategic decision to prevent an uncontrolled price spike. The move also tempers the argument that China’s energy security is beholden to Iran, or that a US attack tangentially weakens China’s energy security. Instead, the middle kingdom turned inwards by banning product exports and imposing price caps on domestic petroleum products. The combo quickly made refining unprofitable as crude prices spiked. Consequently, refineries cut utilization to operational minimums (from the mid-70s to the mid-60% range). Prior to the war, China was building SPR inventories by ~1M bpd, and if we use a 4M bpd average decline in imports, there’s a 3M bpd gap. In all likelihood, product stocks drew by ~1M bpd, and crude 1-1.5M bpd. Demand destruction and exports redirected to the domestic market likely rounds out the remaining balance.

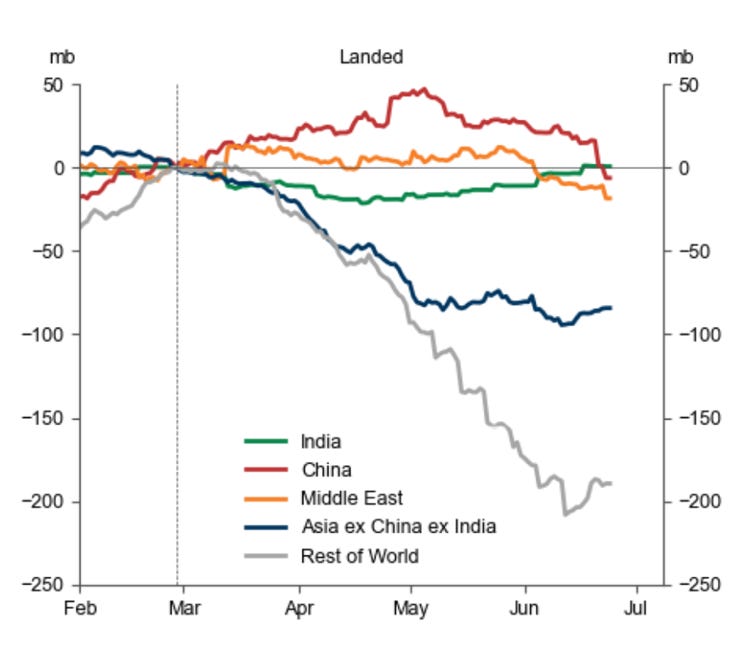

Unfortunately, Chinese inventories are opaque. Product stocks aren’t accurately tracked, and part of China’s crude stocks are stored in caverns that are difficult to gauge with satellites. Still what we can see is that it they’ve begun to decline given the intensity of the push-back.

Landed Chinese stocks have recently accelerated their decline, and have fallen by 2.2M bpd in the past few weeks. How long will this continue? Only China knows. It has 1.2B barrels of stored crude, so theoretically it can endure for quite awhile, but with current net imports running 7M bpd lower today that’s a heavy amount to destock.

As prices have calmed recently, China’s removed some export restrictions, which means Chinese teapot refiners (those not state owned) are starting to lift demand and refinery utilization. China’s actions will play a big role in determining how the war’s impact plays out. If it elects to drain its inventories, then the oil market can remain suppressed. In all likelihood, China will return to the market, and any incremental demand increase should lift prices higher as it’s a step-change in demand in a tight market.

Once and For All?

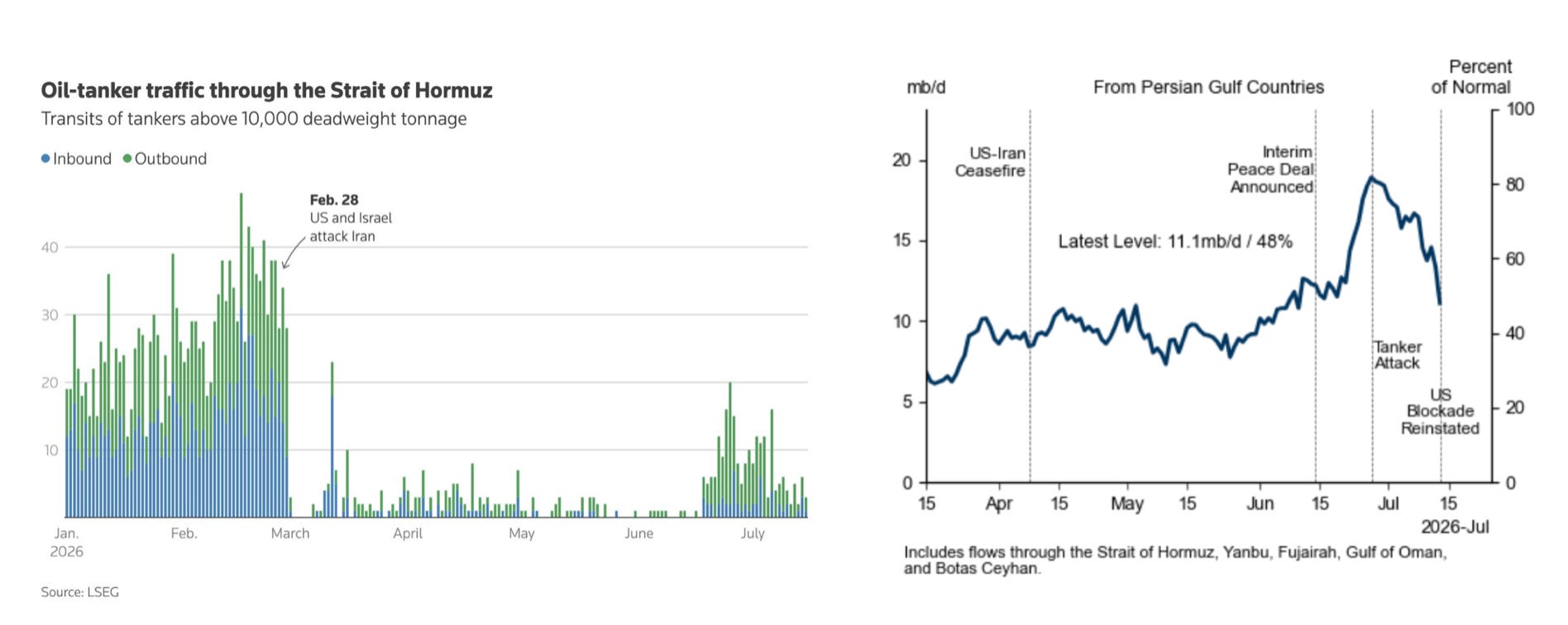

So what happens next? The SoH has closed again and the US and Iran are exchanging fire. The MOU has been declared dead, and the US plans to attack for a week straight to degrade Iran’s ability to threaten shipping lanes. The goal may prove to be impossible given Iran’s topography and size. The SoH reopened for ~3 weeks during which Iran shipped out nearly 80M barrels, which at recent prices was worth ~$6B, and it gave the regime some breathing room for another sustained campaign. Once attacks restarted, shippers turned cautious again. As tankers dipped so did the estimated oil flows out of the Persian Gulf. Today we’re hovering at 50% of normal (i.e., 11M bpd). This includes rerouted crude in the aforementioned pipelines.

We expect flows to slide lower as the reinstituted US blockade on Iran begins anew. Iran will suffer more airstrikes in the interim, and how it retaliates (i.e., does it attack the bypass pipelines or close the Red Sea) will determine the next phase of this campaign. The US appears to be taking out Iran’s maritime infrastructure, the one used to control the northern corridor, but we’re not sure they can eliminate the shipping threat without landing troops at Bandar Abbas or Qeshm Island. If correct, this campaign has many stages left.

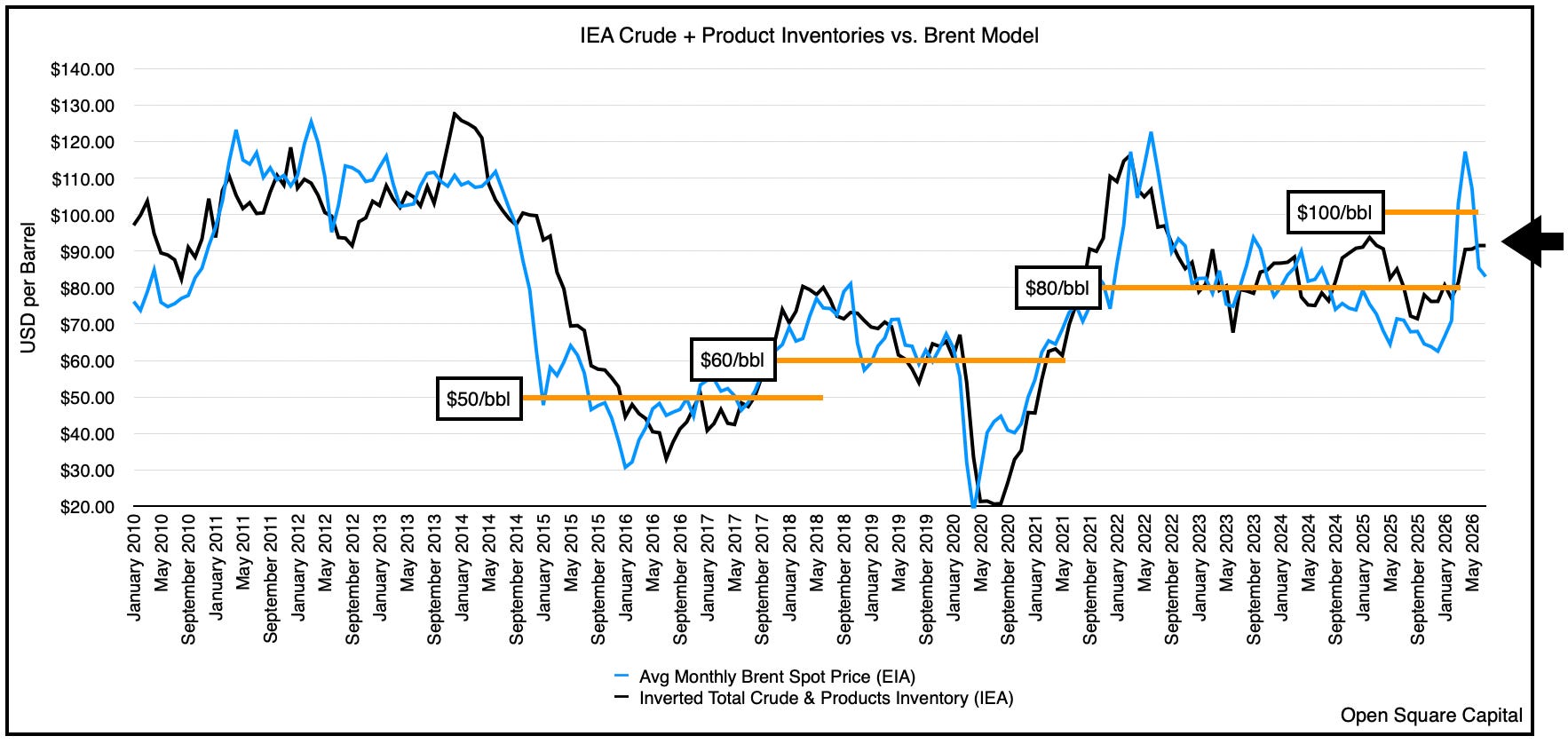

So we’re really back to where we started, except inventories are much lower. Oil prices have bounced, but the recovery has stalled near $80/barrel for WTI. Given the size of the outage and current reserves that’s . . . unusual. We hesitate to claim that there’s manipulation in the current market, but if crack spreads (i.e., what refiners make) are any indication, the culprit is in crude. Jet, diesel, and gasoline margins are screaming higher, and near $120-140/barrel. Historically crude prices are tied very closely to products. We think it’s inevitable crude prices catch-up if this conflagration lasts.

Our working assumption is that eventually some sort of agreement favorable to Iran will be finalized. Outside of killing all of Iran’s leaders and attempting a regime change, the US has very little leverage given Trump’s aversion to landing troops. Air strikes can only do so much. This means Iran’s in the driver seat on managing the SoH, uranium enrichment, and the lifting of economic sanctions. We believe they may eventually get all three. Control of the SoH protects the nuclear issue, and vice versa, and now that the Iranian’s have a chance keeping both, they’ll start from that position.

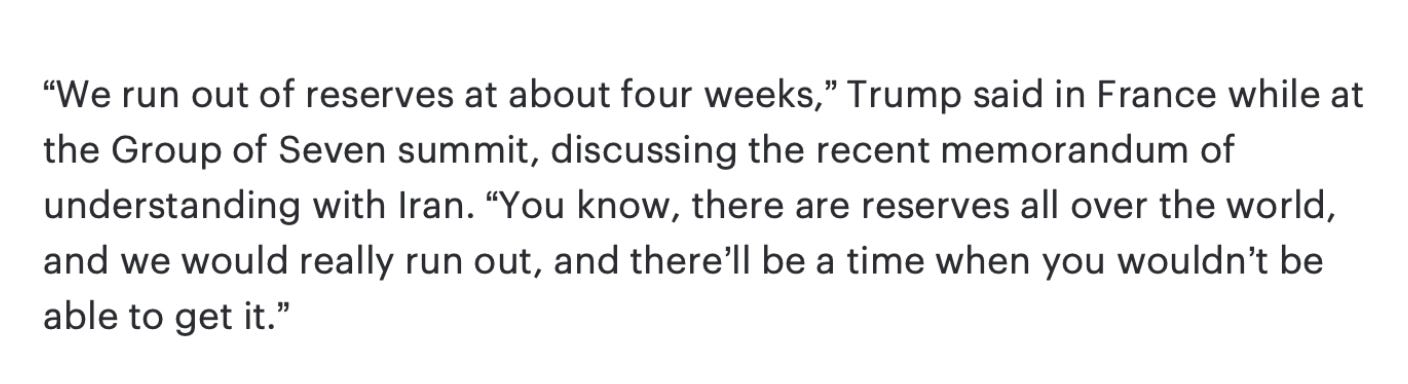

A few weeks ago, Trump shared this tidbit at the G7 summit meeting. This was after a ceasefire had been signed, and negotiations were progressing. The clock is ticking and if it continues, in his words “bedlam” will happen if oil ran out.

Our Companies

Like oil, our energy equities have round-tripped back to February 28th prices (i.e., when the US attacked Iran).

OXY finished the quarter lower than its share price before the war started ($47/share vs. $53/share). It’s since bounced higher after the quarter-end, but you can see it’s only at pre-war levels even though oil prices and geopolitical risks are significantly higher.

At $65/barrel, we anticipate OXY will generate around $5.2B in free cash flow (“FCF”) or $1.3B a quarter. Tack on a 10x multiple and this is a $50/stock . . . basically where it’s at right now. Fortunately, oil prices did average $95/barrel, $30/barrel higher, in Q2, which equates to another $1.5B in cash for the quarter. Add that onto the $1.3B and OXY should generate ~$3B for Q2 in total. It all likelihood, this figure will be higher because OXY makes interest and tax payments in Q1/Q3, so Q2 typically has higher cash flows. By the next quarterly report (in a few weeks), OXY will have achieved its near term goal of paying down its debt to $10B after ending April at $13.3B.

The company almost certainly knew this was achievable when it offered up that goal during its May earnings call (as they’d already booked half of Q2 by then). Fortuitously, oil prices cooperated when the SoH closure stretched out. Though prices fell off at the tail end, OXY should’ve earned enough to repay the debt. At a 6% average interest rate, the debt pay down will reduce interest expense by $180M a year, again apply a 10x multiple to that, and its good for about $2/share.

Really though, what’s next? We’re stuck at $50/share right now, after touching mid-$60s on March 31st. Oil prices are ~$80/barrel, but based on inventory data we should be mid-90s. To reiterate, forget the mid-90s or even triple digit oil. If oil prices persist even in the mid-80s, cash flows would be close to $9-$10B a year. Apply a conservative 8x multiple and the stock would be close to $80/share, 60% higher than today. OXY’s shares are significantly undervalued and after bulking-up via M&A, repairing its balance sheet, and refocusing on oil production/development (post-OXY Chem divestiture), the company’s deep inventories and significant midstream infrastructure makes it a compelling takeover candidate. If the public market doesn’t recognize the deep value here, we think a larger company eventually will.

Transocean

Similar to our OXY holdings, our Valaris (“VAL”) investment also round-tripped. As you may recall we purchased shares of VAL last quarter after it announced a tie-up with Transocean (“RIG”). At close, each share of dAL converts into 15.235 shares of RIG. In RIG’s most recent quarterly update, the company indicated that the US Department of Justice (“DOJ”) issued a second request and will require additional time to review the transaction for anti-trust issues. The government’s forced to take a closer look because a combined VAL-RIG (“New RIG”) will own a larger global share of the 7th generation offshore drilling rigs.dThere are a few positive factors though, New RIG will only own ~1/3 of the 7th generation drillships, and given it’s a large global market, it’s not an entirely dominant position. Additionally, thede are 7 stacked rigs, which is indicative of a soft market, and RIG can add those back, or sell them if the DOJ requires mitigating actions. A New RIG will become the leader of the industry with $10B in drilling backlogs, but Borr and Noble will still be nipping at its heel.

We think eventually an approval may require some divestitures, but overall the drilling market is large enough if we look at the totality of drilling ships and jackups that a combined VAL/RIG should clear the necessary hurdles. VAL shares currently trade at a slight discount to the RIG shares, which is the market pricing in a fairly high certainty that the merger will be consummated.

We continue to hold the shares, and may look to add if we see some weakness.

Parting Thoughts

The oil market’s round-tripped the entire US/Iran War. Frankly, that’s bizarre, considering the conflict never ended. It’s moving to a new phase. While the MOU signed on June 17, allowed trapped Persian Gulf tankers to exit, the market extrapolated the temporary relief (+100M barrels of pain numbing anesthetic) as normalization. It then proceeded to forecast a resumption of free trade, reintegration of Iran back into the global economy, and a super-glut of oil supplies in 2027. Not so fast, as Iran’s recent attacks coupled with US counterstrikes have ended any illusion that the parties are close to a lasting agreement. Their positions are simply too far apart and intractable.

This will all take time. Negotiating leverage will need to be won on the battlefield. The brief respite has allowed both sides to catch their breaths and refill their stocks (whether it be in oil, weapons, or coffers). Refreshed, they’ll likely keep bombing each other, but avoid strategic targets lest the situation spirals uncontrollably. The US military controls the battle space, but the Iranians run the clock. It knows that the global economy is weeks/months away from “bedlam,” and/or wholly relying on China’s good graces to be the world’s energy savior if we run out. Both options are obviously deeply unpalatable for the US.

Again, conservatively global production is down 10-11M bpd today. Sure “visible” inventories are drawing half of that, but both of those numbers are still overwhelming. OECD commercial inventories point to a mid-$90s price for oil, but product prices are the tell. They’re already pricing $120-140/barrel.

Is it really surprising that Iran will do all that it can to keep control of the SoH? It’s an economic thermonuclear weapon . . . and second only to the pursuit of their first thermonuclear weapon. We handed it to them, and they’ll try to keep it.

So as we write this the ceasefire is dead, the MOU is dead, the US blockade on Iran is reinstated, and the attacks are intensifying. Product prices are trading over triple digits, and crude is lagging badly even as inventories plumb new lows. From our standpoint, as the turmoil continues and the disruption lasts, social media postings claiming that an agreement is near will become increasingly ineffective. Positioning is already bombed out and the market was short before the latest barrages, so who’s left to sell? To us, the administration’s dug a hole, but they’ll keep digging. It’s the only option. Nonetheless, even when it does, we’ll find ourselves in a whole new world.

Mommy: Those kids came over and wanted to play next to you?

Addy: Yea, I suggested they dig a hole in the sand.

Mommy: They just kept digging and digging . . . I thought they’d end up in China.

Me: hmm . . . I wonder what’s actually on the other side of the world.

Mason: (casually) . . . The Indian Ocean . . .

Me: Wait, what? . . .

Me: Seriously? Like, really? Not China? The Indian Ocean?

Mason: Yeah.

We better stop digging.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

What are the chances of Trump implementing an Oil export ban? Will that not decouple WTI from global markets and crash it?