Our Q4 2024 Letter & Look Ahead

January 25, 2025

Skewed to the upside. That’s Wall Street’s euphemism for . . . it’s going higher. Apparently everything is, everything and anything with a good story. Like friendly Hawaiians, just sit back and let’s talk story. Crypto, AI, Stargate, even quantum computing. This is our near future. Some more real than others, but most are science projects that seemingly deserve funding when money’s plentiful and hype’s on full blast. Like a tourist trap, our markets are filled with hawkers. If you don’t see what you like, no worries, we’ve got other themes that’ll play better to your senses. Some plausible, most improbable, they’re all ideas that bubble and toil with promises of riches, or trouble. Indeed hopium is the most abundant element in ’24, and it’s carrying into the new year.

We don’t get it though, as evidenced by our wretched year. Truthfully, we never did. We didn’t in 2020 or 2021, and you know the rest. We can’t grasp the value of Tesla, the genius of Microstrategy, and the inevitability of crypto, all of whose brilliance grows ad infinitum. Believing that the recent scarcity in prudence rivals that of bitcoin means we’ve failed to board these beautifully crafted financial flywheels, where bigger begets bolder, and bolder begets richer. People are literally printing their own money now. My unicorn money will perform better than yours, my alt coin has a more amusing name. It’s legitimate because our leaders say so; Trump has a coin, Melania too, heck maybe Barron too. Never mind that this level of self-enrichment creates dangerous avenues for political influence, as long as people get paid.

Lest you think any of this is political commentary, it is not. Greed brings us all together, and together we bask in our collective financial folly. Case in point, Microstrategy, brilliantly issuing a 5 year, $2.6B, 0% unsecured convertible bond. The debt matures in 2029, and they’ll use the cash to buy more bitcoin. The conversion price is $672.40/share, when the stock was trading at ~$473/share. Who willingly “lent” $2.6B of unsecured money to a company for 5 years at 0% interest to get a call option that’s priced 50% higher than where the shares were trading at? Who cares, but someone did. Why? Well as the CEO explained, they’re just providing a trading vehicle for those who wanted more upside exposure. Likely the ETFs that promise 2x the return of MSTR, and need more call options to do so. Genius. If that’s the price for this merry-go-round, we aren’t willing to pay. As they say, “have fun staying poor.”

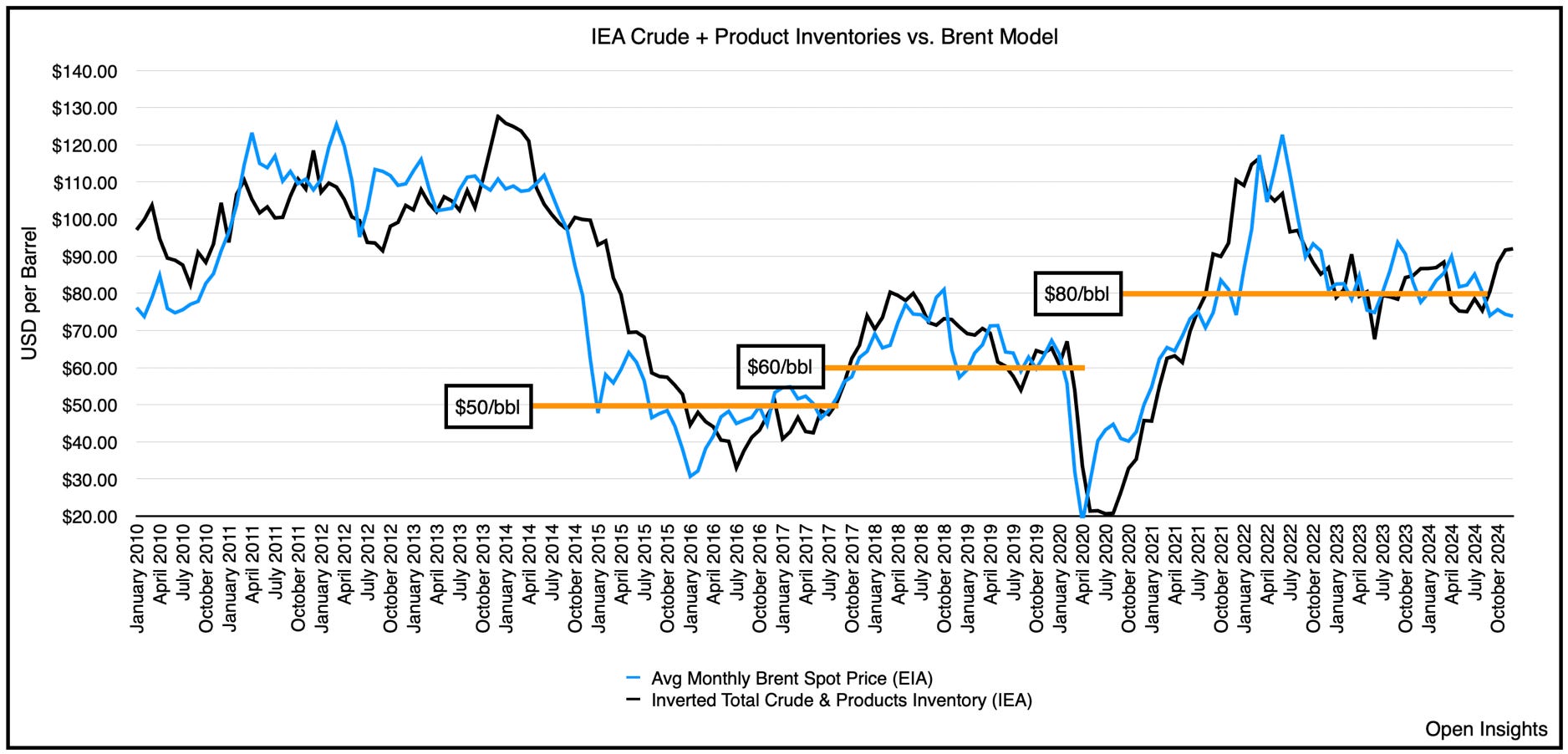

We are though. Staying poor that is, for now. Deprived of gains this year because of decisions of our own making. We can write about “process” or “research,” but the truth of the matter is we not only picked investments in things that are out of favor, we did so in the worst performing sector. Energy stocks were either flat (for larger companies (XLE)) or down (for smaller companies (XOP)). This is against the backdrop of oil prices that round-tripped the year to start and finish at ~$72/barrel despite inventories pointing to ~+$80/barrel. No one cares. That’s the crux. The other market baubles are too shiny not to draw attention, and why invest in a sector whose production can be controlled by the whims of governments, or their leaders? Can they though, will they? Will OPEC+ cooperate after experiencing the quick policy reversals in Trump 1.0? Inventories finished at 5-year lows even with China and Europe economically stagnant. As Non-OPEC+ production slows, OPEC+’s leverage grows. All the while, China is about to stimulate economically, and the Western world is about to run GDP “hot” to devalue its debt. Against that backdrop, we think oil prices are “skewed to the upside.” Again, no one cares. They might though, one day they might care about the real things, the things you use, consume, and build with. Those might matter again.

Oil Update

It’s a conundrum, either inventories are off or oil prices are off, and we don’t think it’s inventories.

As analysts trumpet inventory builds in 2025 based either on faulty assumptions or intentionality, prices have languished below the threshold needed to spur production. To keep inventories steady, oil prices need to be higher than $80/barrel, but as we exited 2024, we were nearer $72/barrel. In the past few days, oil has rebounded ~$75/barrel, but that’s immaterial. The longer we stay below fair value, the more supplies decay. Combining slower supply growth with accelerating demand growth will be a recipe for higher energy prices as we enter 2025.

In 2025, non-OPEC production growth will slow further as US shale production flatlines. Increasingly analysts are looking to Brazil, Canada, and other non-OPEC countries to fill the gap, but just like the US, forecasted growth outside of OPEC will be easier to find on spreadsheets than in reality. Hence, OPEC+ becomes the last man standing. As control over the direction of the oil market shifts to OPEC+, we surmise they’ll use it. The oil price floor has been set at $70/barrel here, and it remains to be seem what the ceiling is. Globally, inventories today are at 5 year lows, so not much to say there other than barrels are drawing as OPEC+’s voluntary cuts offset the free flow of “sanctioned” Russian and Iranian oil. Here’s the latest satellite chart.

See that little tick there on the bottom left? That’s where we’re at today. As the Trump administration takes office in another few weeks, we anticipate tighter Iranian sanctions and the potential loss of Iranian barrels. From the summer of 2018 to the end of 2019, Iranian liquids supply fell by ~1.8M bpd following the abandonment of the JCPOA. We don’t anticipate anything near that this time, even a quarter of that would be significant. Our conservatism stems from Trump 1.0 and Biden’s administration, where the political reality of higher prices can easily outweigh the moral fortitude of enforcement. After being fooled by Trump 1.0, OPEC+ and Saudi Arabia will also play it cautiously this time before backfilling supplies. They’ll likely wait to see barrels come off before unwinding some of their cuts and boosting production. It won’t be an outright rejection, they’ll merely say they want to “ensure long-term energy stability,” or something to that effect, so watch out and read between the lines. Lest we forget, Vision 2030 (Saudi’s attempt to transform its economy) is a mere 5 years away, and oil prices in the $70s have already forced a downsizing of NEOM, its mega-city project that will serve as the cornerstone of the kingdom’s vision. Again this is about creating jobs for a younger generation of Saudis, lest discontent leads to political dissent and instability. So oil price stability = economic stability = a chance at political stability.

So with inventories low, all eyes now turn to 2025 balances. The key for 2025 remains demand. Demand for 2025 largely comes down to our assumptions for the US and China. We think given the push for deregulation and growth in the US, the US economy should keep ticking along. President Trump has already lifted business sentiment and filled his leadership team with executives pushing for material GDP growth. Fortunately, the US consumer is healthy. Wage growth will power higher as the unionized contracts handed out these past few years kick-in and if immigration policies tighten as everyone expects, you could see a pickup in low wage worker positions, driving further wage increases. More importantly, homeownership in the US is ~2/3rds, and many are locked in at low rates. Couple that with low unemployment rates and rising wages you essentially enter a “debt jubilee” period. The remaining disposable income truly becomes disposable.

See the consumer deleveraging? Since the consumer drives this economy, what happens to the economy if the consumers’ debt burden declines? Whoosh goes GDP.

Taking a look at China, much will depend on local demand there. Mired in a housing recession with falling property prices and high numbers of unsold homes, the deleveraging process there will continue. The speed of China’s recovery will depend on the depth of the incoming US trade war and China’s own fiscal stimulus efforts. Monetary policy has been kept fairly loose, but the private demand for loans has been weak. Central bankers are pushing on strings, and everyone’s waiting for the demand pull. We’ll have to wait a few more months. We doubt China will unleash its full barrage of stimulus measures without first evaluating how much Trump 2.0 tariffs will disrupt trade flows.

In the short-run, will China be willing to stimulate domestic demand, and/or will it agree to another trade pact? We think they’ll choose the former first, before seeking the latter. Recently, China released its December politburo meeting statement and changed the wording on its economic policy stance to “moderately loose,” a term last used in 2011 before significant stimulus measures were enacted. These words coupled with “to aggressively boost consumption, and lift investment returns,” and “comprehensively expand domestic demand,” certainly seems to indicate a potential change, but they are right to be cautious. The impact of full US tariffs have yet to be felt, so a wait and see approach makes sense. Net/net though, we do anticipate continuing China recovery this year. Exports will stay flat as they are redirected, and China will mitigate the US tariffs with some currency devaluation and fiscal stimulus. While the property market has yet to bounce back, it does appear a floor has been established. Ultimately, like the prior trade war, we think both parties will eventually announce some type of trade agreement, turning mutually assured harm into a face saving PR event. For the time being China’s oil demand has held firm despite the tepid economy, and risks are skewed to the upside if it recovers domestically.

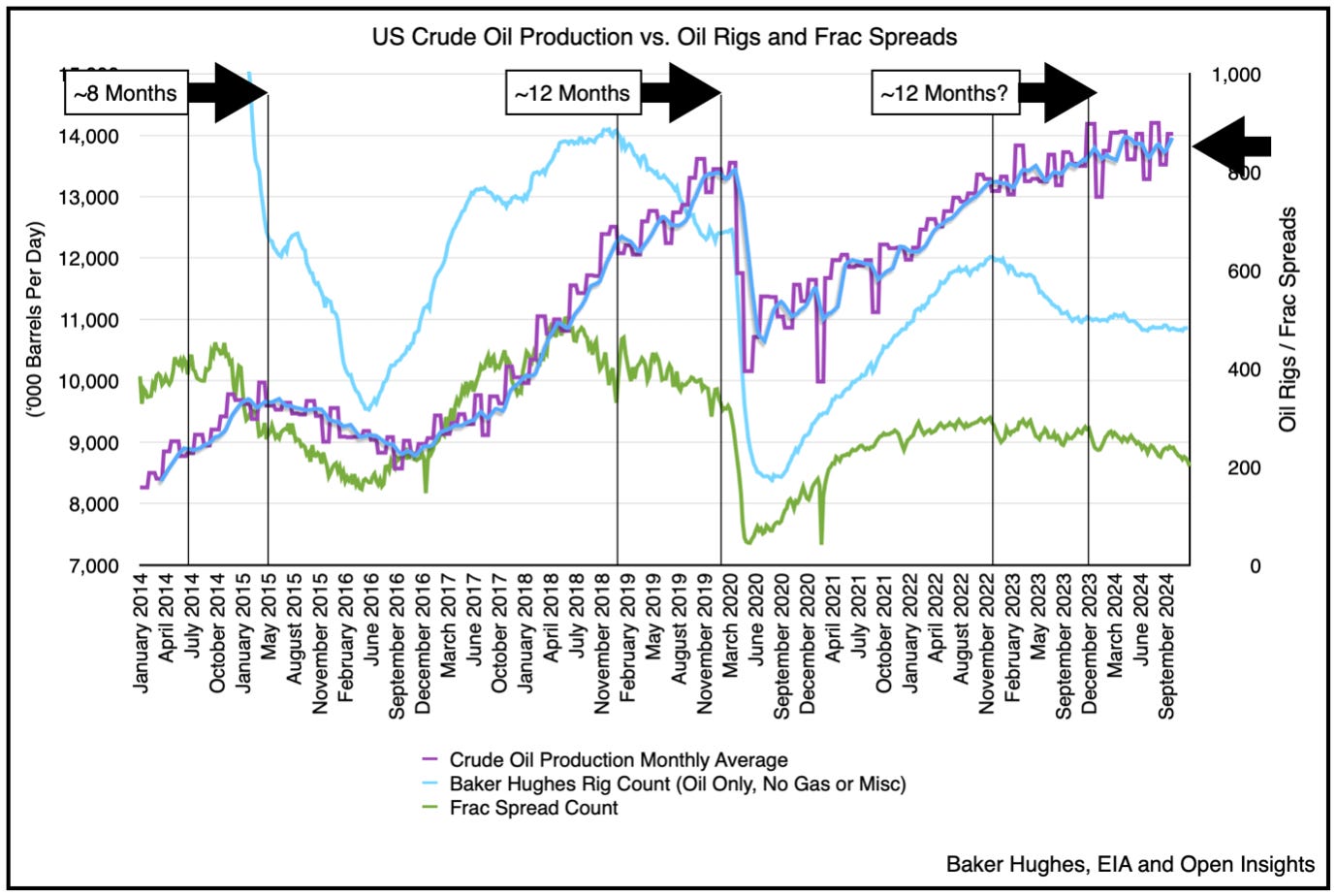

As for supply growth, as we anticipated, spare capacity largely resides in OPEC+’s control. Non-OPEC+ producers have started to weaken, and the IEA anticipates growth to come down to US, Canada, and Brazil. We can see US growth has flatlined, and what growth we’ll likely see will come in the form of mostly NGLs and NG. As the basins get increasingly gassier, we think crude production will stay flat at these levels.

Growth in US production is finally reaching a plateau. The correlation between rigs/frac spreads to production held, and despite the increased productivity of drilling longer laterals, US production has stabilized ~13.3M bpd of crude. In 2024, maturation arrived, which means production will get gassier, producing more natural gas and natural gas liquids (i.e., less crude). So while we may see headlines trumpeting US growth, note carefully much of it will be in “barrels of oil equivalent,” and that “equivalent” is really gas.

Consolidation in the space has left the Permian basin with 6 companies (including our Occidental Petroleum) controlling nearly 2/3rds of the production. What they do largely dictates where US production goes, and for them it’s about farming and harvesting. Annual growth targets are in the low-single digits, and with most of the Tier 1 acreage held by them, the remaining 1/3rd of producers will be hard pressed to add to that. In fact, we think production could begin to flatten in 2026 and then tip-over as Tier 1 acreages become exhausted. There will be some growth this year, but mature basins and large scale consolidation of producers means that despite the administration’s desire for “drill baby drill” 2.0, the realities on and of the ground are very different.

The IEA further anticipates Brazil will grow by ~250K bpd in 2025. We highly doubt that as Petrobras, Brazil’s national oil company, just published its 5 year strategic plan, a plan that shows 400K bpd growth . . . in 5 years. So like the 300K bpd forecasted growth in 2024 that never materialized, we think Brazil’s supply growth for 2025 will be overly optimistic. Lastly Canada, with the new Trans Mountain pipeline, it’s conservative to say that the forecasted growth there will come to fruition. If there’s egress, producers will fill it. Overall IEA forecasts non-OPEC Supply will grow by 1.7M bpd and the EIA forecasts a 1.5M bpd growth. For the IEA, this will lead to a nearly 800K bpd build, or nearly 290M barrel build in inventory. No comments on that other than to say they did the same thing last year and overestimated supplies. We’ll take the under this year again.

Select Holdings

For our energy holdings, 2024 was the year of incremental progress. Let’s run through our larger holdings. Occidental Petroleum (“OXY”) closed its major acquisition of privately held CrownRock, and started on a path to deleveraging. On the other hand, MEG Energy (“MEG”) achieved its debt targets and then committed to returning 100% of its free cash flows to shareholders via a small dividend and share buybacks.

For the first name, the pace of OXY’s debt pay down will depend on oil prices, but with synergies to be captured this year (e.g., expiring unfavorable midstream contracts, synergies stemming from CrownRock acquisition, and OXY Chem improvements), we expect to see enhanced cash flows to accelerate the debt reduction. These savings should be independent of what happens to energy prices, which is unusual, but speaks to the company’s operational capabilities. The new Carbon, Capture, Utilization and Sequestration (“CCUS”) hub called Stratos will also begin operating this summer. Getting that facility up and running will help prove out the CCUS business model and de-risk the capital being spent.

Even with Trump’s inauguration, we don’t think the Inflation Reduction Act (“IRA”), which provides 45Q credits to sequester the carbon, will go away. 45Q tax credits are critical to the economic viability of this nascent sector, but the IRA bill was crafted so that a majority of its benefits will flow to Republican leaning states, so these subsidies are likely to stay.

The 500,000 tonnes per year (“KTPA”) Stratos will initially operate at half its capacity, with the remaining 250 KTPA to come online in 2026. To put that in perspective, Stratos will capture the carbon emissions of ~120K cars a year, or the same amount as a forest half the size of the Grand Canyon. The second phase is designed with 30% fewer air contactors and fewer pellet reactors per train, which greatly simplifies construction and reduces operating expenses. OXY is also progressing on its much larger King Ranch project, where it’s expected to receive $500M of funding from the Department of Energy, and many of the Stratos enhancements will find their way there.

Currently the market assigns no value to OXY’s green endeavors, operational improvements, or post-acquisition synergies, but while we believe the first makes sense until Stratos is operational, the latter two don’t. OXY’s been playing conservative with guidance, and if oil prices return to fair value, the cash will flow. Lastly, Warren Buffet/Berkshire reinvested all of their 2024 OXY dividends into common shares of OXY stock, which is another vote of confidence. Yes, that is confirmation bias, but we’ll take it.

As for MEG, it’s announced capital plans to increase production from 110K bpd to 135K bpd at its Christina Lake facility by 2027. 2027 is a bit aways, but the increased spend will eat into cash flows for the next three years. Fortunately, the investment is manageable as free cash flow (“FCF”) approaches nearly a billion when WTI notches $80/barrel. On the production front, the company plans to produces around ~105K bpd on average in 2025. From our perspective, MEG will continue to execute and cannibalize its stock. Canadian E&Ps are currently trading at a discount to their US brethren, which is why we’ve stayed in the name. Threats of US tariffs are hampering the rerating, but we doubt they’ll be put into place. If they are and the costs aren’t passed along to consumers, then MEG’s 2025 cash flows will be impacted. In reality though, oil is fungible, so eventually the costs will be passed along to consumers unless the US consumer elects to stop driving. Canadian oil primarily flows into PADD 2 refineries, so tariffs will hit the Midwest voters first, which may prove to be politically unpopular.

Speaking of which, the announcement that Justin Trudeau will step down as Prime Minister also means the threats of environment regulations and other pressures on the energy sector should subside. In H2, we anticipate an uplift/rerating as the Canadian elections kick into full swing later this year and the conservatives take power (they are leading in the polls) if the tariff threat abates.

On a longer-term scale, we think MEG will eventually be taken out when a larger producer (e.g., Suncor, etc.) plays capital arbitrage and acquires the producer with a portion of stock/debt, bumping up its own FCF to make the transaction accretive. MEG as a standalone entity makes little sense. What it comes down to is price, and MEG is looking for is a higher one. We’ve heard in the $40-50s, which makes sense given their plans for production increases. In the meantime, MEG will self-cannibalize, using FCF to repurchase shares. Steady as she goes.

Parting Thoughts

“I didn’t come this far, to only get this far.”

It’s a well worn sentiment. You hear it all the time in the PTON workouts. Many have said it, even more have repeated it. It’s said to bolster self-belief, determination, and the motivation to continue. It’s about making good decisions, enough of them so that they can compound on one another. We see a world increasingly devoid of sensibility, common sense, and sound judgment, one where the fine line of civility and what’s decent have shifted notably. Questionable behavior is being rewarded, and decisions made with little regard for consequences are yielding handsome returns. It’s happening financially, politically, socially, and economically. We keep erasing the lines of what’s sensible, only to redraw them in areas we previously thought were unfathomable.

How did we get here? How did we get to a place where the President can release an “official” meme coin that is suddenly worth $40B the day before inauguration? Who or what is buying it willingly to enrich its promoters? What of Fartcoin, Dogecoin, or the Hawk Tuah coin? The last of which quickly hit a market capitalization of $500M before immediately plunging 95% to $25M in an afternoon after the grifters cashed out. Today it’s “worth” $28K.

Now that’s a rug pull.

A sheep skin rug that is. Whether the rug pull comes from the grifters themselves, or the trend chasing Wall Street croupier, it doesn’t matter, the sheep always gets fleeced. Frankly, this cohort of sheep have never seen it before, and the snippet they saw during COVID, in the first run of crypto, meme stonks, and SPACs when government money rained from the sky was a mere taste of the mountain of absurdity we’re about to see. What delineated between the nonsensical and real has long past. The truly egregious things these days induce only a chuckle, but that very apathy speaks to our level of desensitization and cynicism.

THAT IS NOT A GOOD THING.

The grift that used to occur in isolated areas of the market is now in full view, fully embraced by everyone as the sign of the times. Meme coins are just a byproduct of that shift, a world where excess liquidity and rampant speculation collide. The oncoming adoption of these things by institutional managers doesn’t just give it validity, it simply means that big money have agreed to ride the wave. So as we ride into 2025 with a new administration, one bent on enriching themselves in their last turn at the controls, investors of all ilk are giddy with anticipation.

Maybe we’re old, calcified in our intransigence. Maybe though . . . the grift is real.

What is the real measure of a person these days? What is a company or thing really worth? Perhaps we are stodgy, still clinging to the belief that cash flows matter, and for individuals, what you do and how you do things matter. Today, all that matters is #winning. How that win is achieved doesn’t. Winning is right, and winning is righteous. Everyone else can “have fun staying poor.” Forget self-reflection, genuflection at the alter of what’s working and those who are winning are the order of the day. That’s the game that’s being played, and if you aren’t playing it, then pox on you and your investors. Fair enough. In this game you are your performance, and we certainly aren’t on the right side of history . . . right now.

Right now. That’s the key isn’t it? Things though can change in an instant.

Addy: Auntie Gloria, have you ever heard of this singer?

My daughter posed that question at a group dinner, a teenager seated at a table full of adults by default. It wasn’t loud, but for her parents it reverberated. She’d often stay silent at gatherings of late, unengaged, either because of ennui or self-doubt, any notion of socializing with adults seemed anathema. Yet that phrase, said unprompted and with genuine interest, suddenly showed a different side of her development. It’s hard for teens to talk to adults, it take serious self-confidence to treat those older than you as just people. That one sentence though led to others, and soon enough a conversation. Things change quickly. Flip a switch and a person can grow quickly. In many ways, languishing investments are like that. PTON’s stock doubles simply because some rational executives decided to finally stop wasting money. Oil prices rise simply because inventories draw. We can still imagine a world where things still make sense, one where actions result in consequences and fundamentals do matter. We know it’s hard to imagine otherwise in the midst of this seemingly incessant grind, but we can and will. The market can keep its coins because we didn’t come this far, to only get this far.

So we’ll get after it.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

Thanks for the write up. If i may be so bold, do you have an opinion on Strathcona ?

"Currently the market assigns no value to OXY’s green endeavours"

> The reason is that their previous 'Century' CCS was a failure.

While both plants are categorised as CCS, they use different carbon capture technologies. Stratos is using Direct Air Capture (DAC) while Century is pulling carbon from a specific source of emissions.

Century was also built into a natural gas processing plant to suck in the CO2 it spews before it escapes into the air. This carbon capture process is cheaper, uses simpler tech and is more established than the DAC used in Stratos.

Though Oxy benefited from the direct application of Century, with the captured CO2 used by the oil firm in producing more oil, the older CCS plant failed to deliver expected results:

https://carboncredits.com/occidental-petroleum-quietly-abandons-biggest-carbon-capture-plant/