Peloton's Q1 2024 Review: Incrementally More Colorful

November 3, 2023

As we roll through quarterly reports, we wanted to take a quick look at Peloton, a company we wrote about a few weeks ago.

No we know, the lagging economy, consumer weakness, and general macro-malaise means that a purveyor of high-end home exercise equipment must be a disastrous place to invest your money, but for the various reasons we listed in our original write-up here . . .

We Bought a Peloton, then Bought 3 Million More.

There’s something there. That’s usually the hunch that I get when a stock piques my interest. Most days are spent reading the news, parsing data, and turning over investment ideas, but once in awhile something strikes me as potentially interesting. Recently?

. . . we thought it was a decent bet. After looking over the company’s Q1 2024 results, we still believe that to be true.

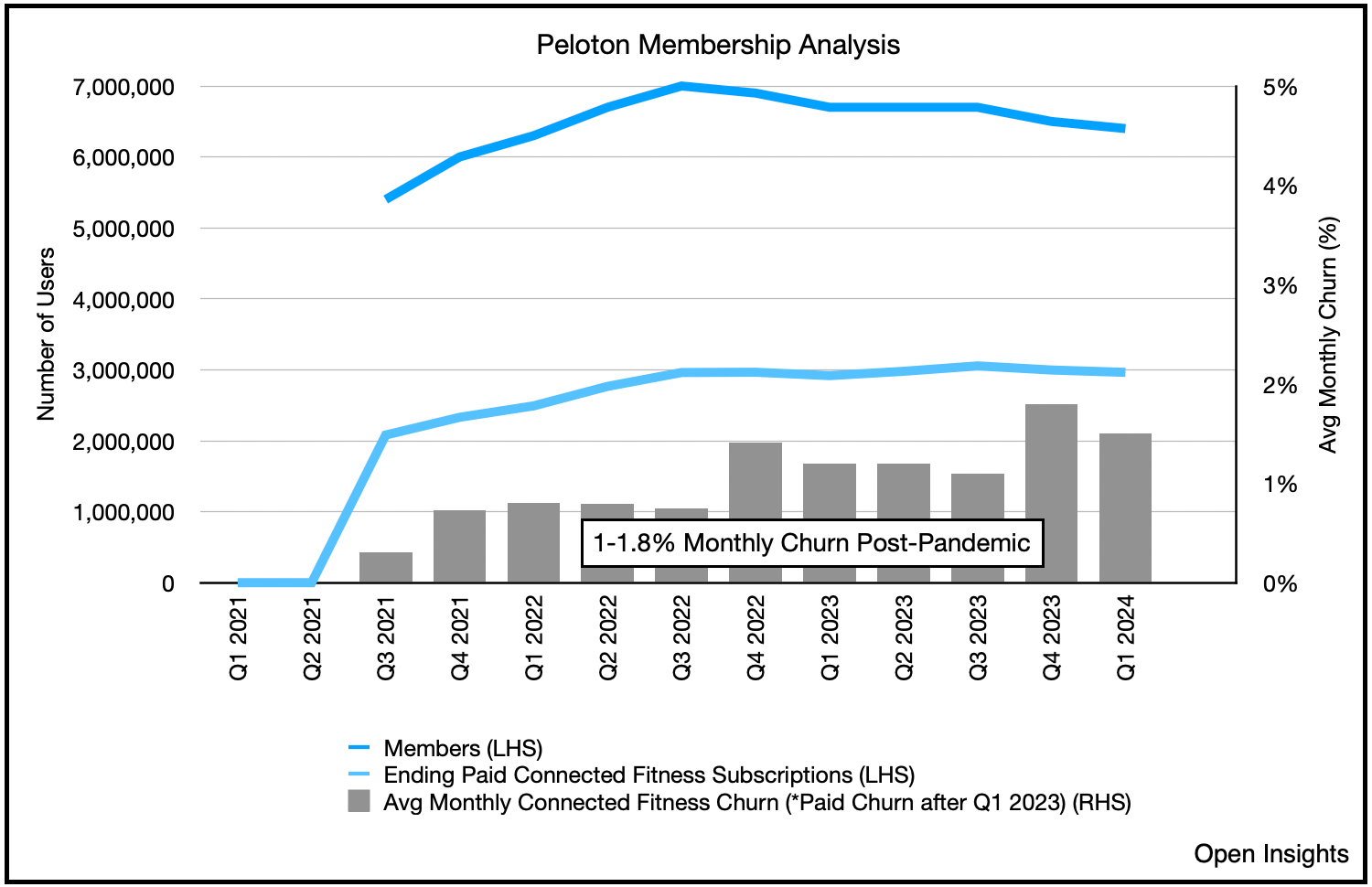

The market’s looking for growth here, or at least for the company to demonstrate an ability to grow. That growth, however, is difficult to see as cash flows are still negative, and overall subscriber rates haven’t inflected much higher. For the most part, subscriber numbers have stabilized, and churn rates continue to hover below 2%, dipping from 1.8% in Q4 023 to 1.5% this past quarter.

That’s a negative 1.5% to be sure, but it’s not inconsistent from what we’ve historically seen for paid connected fitness subscribers (i.e., those who’ve purchased a bike, rower, and/or treadmill). One piece of news that’s particularly heartening to hear is that subscribers are actually spending more time on the platform. Content and user engagement is up by 6% YOY. As Barry noted “[m]embers are engaging with longer classes, and on average, they are taking more class types than they did a year ago.” This bodes well for stabilizing churn, especially after the COVID pandemic, and really speaks to Peloton’s customer captivity. The more they use it, the longer they seem to use it for.

In contrast, App subscriptions, of which there are three tiers (Free, App One ($12.99/month), and App+ ($24/month)) experience a higher 13% churn rate. Paid App subscribers fell YOY by almost 80K to 763K, which forced the company to refocus marketing dollars on capturing paid subscribers (instead of canvasing for subscribers overall (free and paid)). As Barry described it . . .

The bad news is we were less successful at engaging and retaining free users and converting them to paying memberships than we expected.

We did two things in response. First, we shifted our marketing spend to focus on our paid App. That shift worked well and is driving a higher mix of premium priced App+ subscribers than we were expecting. Second, we redoubled our efforts to remove onboarding friction in our App to support new users in finding their first Peloton classes. This will be a long term work in process.

It’s TBD whether this initiative will be successful.

Growth Initiatives Announced in the Quarter

As for future growth plans, the company announced several partnerships during the quarter, and some new initiatives:

Partnership with lululemon that began on November 1 (lululemon Studio Members will have access to Peloton content, and next spring, Peloton will become the exclusive content provider for lululemon Studio). Companies will also offer co-branded apparel;

Partnership with the NBA/WNBA (ability to stream NBA/WNBA games onto the bike and themed content);

Partnership with Liverpool Football Club in the English Premier League;

Partnership with the University of Michigan;

International growth;

Reintroduction of the Tread+ (a $5,995 piece of equipment that’s already sitting in Peloton’s inventory).

The University of Michigan partnership is particularly interesting as it allows the company to tap into the college ecosystem. Here’s Barry McCarthy, Peloton’s CEO, on the plans . . .

I think it might be helpful to explain what the different components of a university deal might include. I’ll use Michigan as an example. First off, let's acknowledge that a university represents a vast ecosystem that includes students, student athletes, faculty, staff, alumni, and fans. We want to reach everybody in that ecosystem. Our co-branded Bike is one way we’re trying to engage these audiences. But in addition, we will be introducing the Peloton App to both students and faculty. At Michigan, we are working with select student athletes to help us drive reach and relevance across the Michigan ecosystem. We also plan to experiment with a Bike rental offering tailored to student needs, recognizing the academic calendar requires movement into and out of student housing at the end of their school year. We’re also going to sell our Peloton hardware to campus recreation centers, athletic facilities, off-campus housing, and hotels around campus. Expect to hear more about our college and sports partnership strategy as FY24 unfolds.

For students and alumni, they can even order a University of Michigan Peloton Bike+. Expect additional schools to be added soon.

Fitness-as-a-Service

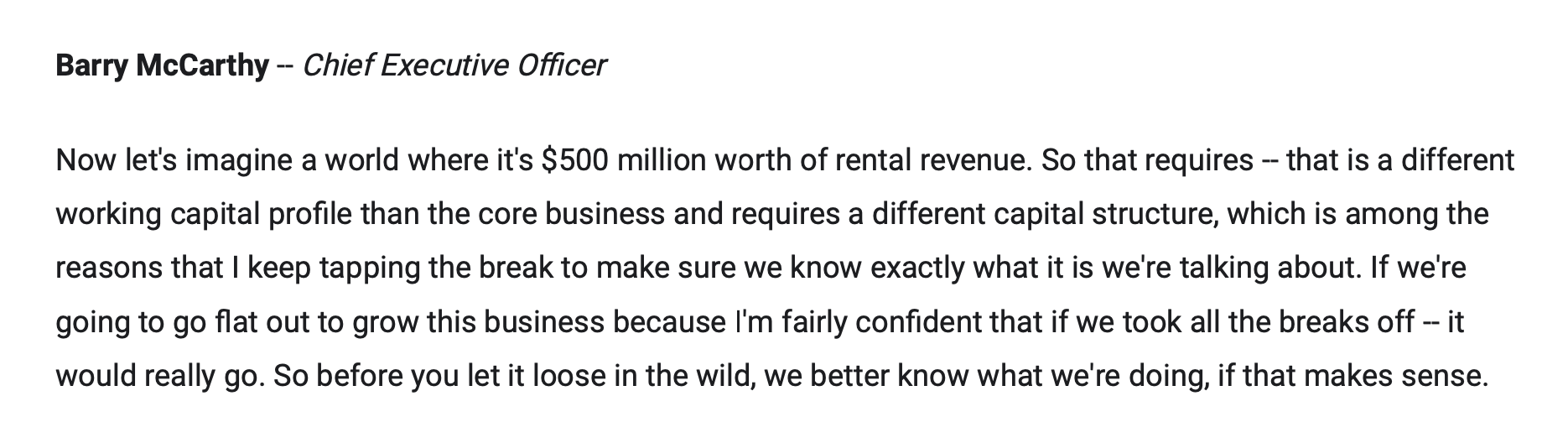

As for Peloton’s bike rental program (Fitness-as-a-Service), growth there continues steadily. It’s currently a small portion of Peloton’s business (i.e., 54K subscribers, with a 75K YE target . . . out of Peloton’s 3M subscribers), but from Barry’s comments, it appears that growth is being deliberately throttled back as growing that business line will require more inventory and higher working capital requirements. Moreover, it pivot the balance sheet away from the “asset lite” version management is trying to achieve. Possible, but only if it’s worth it. As a newer business initiative, the company is still assessing the data for churn, satisfaction, etc. So call the current plan a methodical and considered growth path (as opposed to an unbridled one). Here’s a question by Youssef Squali, an analyst from Trust Securities, that was fielded by Barry . . .

The $500M worth of rental revenue is interesting figure because at an average of say $1,200/year ($100/month), the rental program would essentially consist of 400K-450K rentals, or about 15% of total subscribers today. Such a run-rate doesn’t seem too outlandish compared to the 3M connected fitness subscribers today. At the very least it gives you a sense of the scale and opportunity set. Nonetheless, slow and steady, and keep evaluating that data to fine-tune the program.

Cash Flow

From a cash flow perspective, cash, cash equivalents and restricted cash declined about $76M from $886M to $810M, so the cash burn is real. Expect another quarter of $70-80M cash burn as the company ramps for the holidays, but thereafter Peloton should be cash flow positive for the final half of FY2024. The company expects to be break-even on cash flow for the year, or very close, which means cash, cash equivalents, and restricted cash shouldn’t decline materially from where it stands here. That’s critical because eventually, Peloton’s “free money” (i.e., the 0% convertible loan of $1B) will mature in 2026, and likely need to be refinanced in 2025. The more cash Peloton has on hand (say $800M), the smaller the inevitable note they’ll need to refinance the convertible (call it $200M at 10% interest rate). If so, a $200M “new loan” still means the business will need to shoulder $20M of additional interest expense annually post-2025. So let’s not burn that cash . . . if possible. Again, the above is predicated on the assumption that nothing really changes for the company from today to then.

We obviously think things will improve.

In the more immediate future, the reintroduction of the previously recalled Tread+ to the market will drive incremental revenue and cash flow as well.

These devices are already sitting in Peloton’s warehouses and fully paid for and ready to ship. Given their high price points, we don’t expect significant sales, but even any bump will be incremental to cash flow.

Ultimately, that’s likely the best word to describe this quarter . . . incremental. As Peloton ramps these new initiatives, we’ll be watching for any incremental growth/benefit. The company’s low churn rates gives it a steady base to build off of, and they simply need a few of these initiatives to drive higher subscriber growth and incremental revenues. Given their near break-even business, the incremental revenue should fall to the bottom line.

The executive team is still getting its bearings, but they are all very data driven in their decision making. We believe they’ll eventually figure it out. The holidays are also approaching, and this current quarter (Q2 2024) will give us a good sense as to whether the Peloton brand is as popular as before. If Peloton is really “last year’s” thing, or a “COVID-thing,” then we’ll know in the coming months. If it’s truly a resilient, high-end exercise/lifestyle brand that we suspect it is, then we’ll see the company recapture some of the growth magic.

So for now, Peloton will keep at it, and we’ll keep watching.

True progress measured one-step at a time.

Please hit the “like” button above if you enjoyed reading the article, thank you.