Stay Calm Fed, Don't Smash the Economy

July 31, 2022

We sent out our quarterly letter last week, and after doing so we were a bit busy fielding investor queries. Since our YTD performance held-up in a tumultuous market, we somewhat expected it. Answering questions, providing details, sending info, etc. It’s just the basic blocking and tackling of running a fund. Sometimes it’s a time suck (okay it’s always a time suck) and we try to minimize it because it distracts from the real value add of research and investing. Still it’s “part of the job” so we do it. Doing “it” did mean that we didn’t pay much attention to the market last week, well at least during the earlier part of the week.

Attention starved no doubt, the market decided to light fireworks after the FOMC meeting. Okay, you’ve got our attention . . . whatcha doing?

Ooooh pretty.

Year-to-date it’s also looking slightly better, as the bang-on week helped the S&P 500 and Nasdaq claw-back some of its decline. No longer down 20%, the S&P 500 has temporarily escaped the clutches of the bear and is almost near correction territory. The Nasdaq 100 is still being chased by Mr. Grizzly, but it’s so closer to safety as well.

Still, it’s all relative. Before it was all doom and gloom, and after the claw-back, well . . . it ain’t all sunshine and rainbows, but at least there’s hope. So we sit, paying rapt attention for more claw-backs, more recovery, more better, MOAR. Many investors are hoping their positions get further lifted because YTD many sectors are still down, and despite the up-draft, down is down and up is up.

So what did the Federal Reserve (“Fed”) do exactly this week besides increase the short-term fed funds rate (“FFR”) by 0.75% to spark such fireworks? Well it “pivoted.” Well not really pivoted, but just kinda . . . sorta did.

The Fed Mandates

Recall that the Fed is tasked with two Congressional mandates, promote price stability and maximum employment. Given the tight labor market conditions (i.e., low unemployment and the number of current job openings far exceeds the number of eligible workers), the Fed is fortunately only fighting an economic war on one front: price stability.

Since inflation is running at 9.1% YOY, but the labor market is healthy, the Fed can afford to tighten financial conditions to temper demand without being too concerned about employment. Here’s Chairman Powell . . . (note all quotes below are from the Fed’s Q&A presser with Chairman Jerome Powell after the meeting):

“We think there's a path for us to be able to bring inflation down while sustaining a strong labor market. As I mentioned – along with --in all likelihood, some softening in labor market conditions. So that is-- that's what we're trying to achieve, and we continue to think that there's a path to that . . . restoring price stability is just something that we have to do. There isn't an option to fail to do that. Because that is the thing that enables you to have a strong labor market over time. Without restoring price stability, you won't be able, over the medium- and longer term, to actually have a sustained period of very strong market conditions. So, of course we serve both sides of the dual mandate, but we actually see them as well aligned on this.”

Sure some of you may lose your jobs, but as my 11 year old daughter says “that’s tough cookies.” What’s important longer-term though is price stability (i.e., taming inflation).

What appears to have changed though since the last meeting is the slight pivot. The Fed’s adopted a more “data dependent” framework, which is code for “not hiking rates so aggressively.” Instead of continuing with its hawkish stance of raising rates, Chairman Powell last week seemingly dialed-back the heated verbal rhetoric.

“We anticipate that ongoing increases in the target range for the federal funds rate will be appropriate; the pace of those increases will continue to depend on the incoming data and the evolving outlook for the economy.”

He repeats the same sentiment later when he says:

“We therefore will need to be nimble in responding to incoming data and the evolving outlook.”

Not only are they “data dependent,” but the Fed also intimated that they think interest rates are just about right.

“So, I guess I'd start by saying we've been saying we would move expeditiously to get to the range of neutral. And I think we've done that now. We're at 2.25 to 2.5 and that's right in the range of what we think is neutral.”

Wait . . . what?? Neutral? Aren’t interest rates supposed to compensate investors for two things? Risk of loss and inflation. If inflation is running at 9.1% YOY, how does a FFR of 2.25-2.5% = neutral? The market didn’t care, it liked what it heard.

TOO MUCH MATH. WE NO LIKE MATH! FED CHANGE MIND, MARKET GO UP! GRRR!

Understandably, MARKET GO UP!, rallying with the tailwind of the shifting narrative. Short covering, new longs jumping in, and momentum chasing CTAs bringing the algo juice; the participants all drank the kool-aid and powered the markets higher.

It’s something we’d anticipated would happen in the coming months, a rally in the market. The market was primed to rally and the presser gave it the perfect excuse. Frankly, we had surmised that the Fed was going to maintain its hawkish stance it adopted last month into this meeting. That proved incorrect as the softening language attests. Nonetheless, the outcome was the same and the market surged.

If the Fed is traversing a spectrum on which hawkishness is on one end and easing the other, being “data dependent” is basically halfway there. Financial conditions were just beginning to tighten since the Fed’s last meeting, but it just signaled a pullback.

The market, a forward looking beast, concluded that the Fed will eventually be easing in no time to avoid a deep recession. They doubt heard Betty’s “pull-up, pull-up” chime throughout the cockpit as everyone everywhere began debating whether we are or are not in a recession. The White House even became existential about the whole word, asking . . . hey man . . . what really is a recession?

What Say We?

As for us? We actually don’t think the Fed has pivoted. We just think Chairman Powell is simply applying the lessons he learned from a few years back. Rewind four years ago. In October 2018, only 11 months into his leadership, Chairman Powell said this in a PBS interview with Judy Woodruff . . .

“Interest rates are still accommodative, but we’re gradually moving to a place where they will be neutral,” he added. “We may go past neutral, but we’re a long way from neutral at this point, probably.”

“Long way from neutral” . . . yeah that wasn’t the greatest choice of words as the market (S&P 500 below) then went into a free-fall from October to December 2018, forcing the Fed to really pivot and ease up on the rate hikes. What a debacle.

We think they’re thinking about the same implications today. If everyone’s debating whether we are/are not in a recession, we’re probably in one already (or at least a little one). Come out swinging with rates are “a long way from neutral” again and you’ll likely tank the market further. Remember, before the rally this week, the broader market was already down nearly 20%, tack on another 10-15% and that’s a whole different world of hurt.

Tighten financial conditions, for sure, because we have to bring demand down from boiling to a low simmer, yet do so without crashing the economy. Act too aggressively, and we risk a market swoon that could morph into a disaster. The last thing we want is crush sentiment. The economy RUNS on sentiment.

There’s no economy without the “cons” and for better or worse, confidence fuels consumption. Personal consumption drives 2/3rds of this economy, and if the wealth effect turns south, then the “feels” vanish. Smoke the market and the consumers stars sheltering sheltering in place, spending dips, the economy flags, and companies retreat. Then it gets bad. Jobs start to disappear as employers right size positions. If that happens, the Fed will definitely find itself in a real quandary.

It’ll find itself fighting a two-front war.

How do you tame inflation (i.e., tighten financial conditions and constrain demand) AND spur higher employment? Why would employers aggressively hire when the economy slumps? They wouldn’t.

So hence “we’re at neutral” and “we’re data dependent” today.

“So, as I mentioned, we're going to be looking at all those things, activity, labor market, inflation. And we're going to be thinking about our policy stance and where does it really need to be? And I also mentioned that as this process, now that we're at neutral, as the process goes on, at some point, it will be appropriate to slow down. And we haven't made a decision when that point is, but intuitively that makes sense, right? We've been front-end loading these very large rate increases, and now we're getting closer to where we need to be. So that's how we're thinking about it.”

As an aside, the FFR in October 2018? 2.25% Inflation then? A sizzling 2.5%.

Today? 9.1%.

9.1% folks.

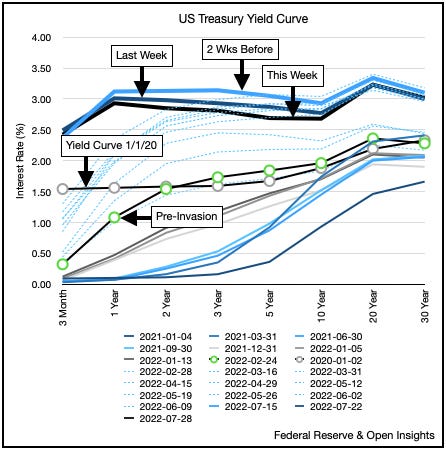

We think the Fed will probably focus on raising rates on the back-end or behind the scenes. The media and investment community tends to fixate on the FFR because it’s easier to digest headlines that “the Fed is raising rates.” What the Fed could do is accelerate the quantitative tightening (“QT”) along the curve itself. By stepping back from buying debt, it’ll force the market to absorb the debt issuances, which should drive rates higher. It’s just the beginning, and as we can see, we’re off to a very very slow start:

Nonetheless, this can be done outside the media spotlight, and can be slightly more surgical than the FFR hammer. The Fed can even let some debts mature (i.e., “run-off”) and not step-in to buy new issuances, or it can even sell the debt it currently has, flooding the market with additional instruments. More importantly, it can do so along different maturities and instruments (e.g., want the 3 year Treasury rates to spike a bit, target those instruments).

Overall, it’s a better tool to try and dial-in the plane for a soft-landing. Whether that’s successful or not? We’ll see.

For us, much of the hullabaloo over the Chairman’s “neutral” and “data dependent” speak is really akin to a captain’s announcement. It’s the reassurance from our pilot that he has this plane under control and we’re still on the approach to landing. Can he really land the price stability plane when so much of the turbulence is caused by structural shortages in commodities? We’re very skeptical. There’s just no easy answers when the issues are structural to begin with, which he admitted as much.

“The public doesn't distinguish between core and headline inflation in their thinking. So it's something we have to take into consideration in our policy making even though our tools don't really work on some aspects of this, which are the supply side issues.”

Still, they have to try right? Yeah.

“So, as I mentioned, we think it's necessary to have growth slowdown. And growth is going to be slowing down this year for a couple of reasons . . . . We actually think we need a period of growth below potential, in order to create some slack so that the supply side can catch up.”

So if your policy of raising rates and QT aren’t exactly the right tools for the job, then why deploy them in such a way as to hammer the economy severely? We still have jobs, so let’s try and keep them, and we still have an “okay” economy, so let’s not go overboard.

*Sigh*

There are no easy choices. Not at this level. At this level there’s just choices. Tradeoffs. Just a spectrum of things they can do, but each one will have consequences, unintended and otherwise.

For us, it’s too simplistic to say that the Fed doesn’t know what it’s doing. They do, or as much as they can with all the consultants and industry leaders they have on speed dial. In the end, what most Fed critics won’t tell you about monetary policy is that . . . THIS IS REALLY HARD!

So unlike most analysts, we’re rooting for our pilot to achieve the soft landing. We know this is tough and we know that the tools are imperfect at best. We’re just hoping our pilot stays calm and rational on approach. Message well, and don’t flip flop much. Play to your audience, and maybe play your audience. Just please don’t Hulk out, please don’t Hulk out, because if they do . . .

TOO HARD,

BRAIN HURT,

ME HULK,

. . . HULK SMASH!

There’s goes our soft landing.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

Excellent article