Strathcona's Acquisition of MEG, What's the Real Price?

May 31, 2025

There sure are a lot of bad takes on Twitter these days, well that and robot responses. This is especially true after Strathcona Resources (“SCR”) launched a hostile takeover bid for MEG Energy (“MEG”) a few weeks back. After 14 days, we finally received the formal bid as SCR just filed its Offer to Purchase. Let’s walk through the transaction to see what we can glean from the details, and share some of our thoughts.

In the two weeks since the announcement, SCR’s investment bankers have no doubt canvased MEG’s largest shareholders to gauge their interest in tendering at the offer price.

What’s that you ask? Well again, the current offer on the table is 0.62 shares of SCR plus $4.10/share in cash for a single share of MEG. SCR at $29.10/share today means the stock portion is worth $18.04/share. Tack on the $4.10/share in cash, and the total bid values MEG at $22.14/share. MEG shares though are trading at $24.02/share, or about $1.88/share higher (+8.5%).

What’s this mean? Well the market’s effectively saying that at $22.14/share, the answer’s a NO. The premium will have to be higher, why sell it to SCR at $22.14 when you can sell it to a willing buyer on the market for $24.02?

We’ve little doubt that the investment bankers shepherding the deal have heard the same answer from MEG’s shareholders. SCR’s initial stock and cash offer just isn’t that compelling.

Why? Here’s a few of them: 1) sure, we like SCR’s management team and its seemingly aligned interest with shareholders (they are after all a private equity fund intent on garnering high returns), but that doesn’t make up for SCR’s inferior oil sand assets, 2) we may get a better offer/outcome if another suitor bids while we’re “in play,” and the upside could arguably be higher, 3) SCR shares may not be what they’re worth once they start trading with higher liquidity, Waterous, a substantial owner of SCR, could decide to exit a large portion of SCR as liquidity rises, and/or use the shares to conduct further M&A, and 4) the pathway for MEG Energy’s stock to doubling (if it remained a standalone entity), is clearer (i.e., grow organically and buyback shares), there’s fewer execution risks.

In essence, SCR’s proposing to mash a company with Tier 1 assets (MEG) with another company with Tier 1.5/2 assets (SCR). Though the combined entity will be run by great capital allocators, the fact remains, MEG still owns the best house on the block. Some of these issues above can be mitigated if the consideration was higher (i.e., if the premium offered was high enough so that MEG shareholders would see that as a fair trade), but not at a 9.3% premium vs. the unaffected price when they announced the bid. The market certainly expects a higher bid as MEG shares are trading above the offer price.

Inevitably though, in any M&A transaction, everyone has a price, and this deal will likely get done. What is attractive about SCR is the capital allocators who effectively own it, Waterous Energy Fund (“WEF”) and specifically its founder Adam Waterous, who’s cobbled together quite the company in SCR.

So what will it take to get this deal done? Probably about $8.

Specifically, we think $8/share.

Let’s zoom out a bit and see where things stand and what we mean. Adam Waterous and his eponymous WEF owns ~79.6% of SCR, and since this is essentially a merger of equals, it’s important for WEF to retain control post-M&A.

So what do things look like if they combine these “twin brothers” (as Adam Waterous likes to refer to the two companies). Well both companies are worth about $6.3B in market cap (CAD). So a combined entity of about $12B give or take. Tack on another $730M of debt on MEG’s balance sheet and you’ll end up with about $13B of enterprise value.

As of May 5, 2025, MEG has about 257M shares outstanding (254.4M shares of common stock, and about 2.6M of restricted and performance stock). Let’s assume the RSU and PSUs will vest given the change-of-control, but they’ll be cashed out (i.e., paid in cash). If so, we’ll use the baseline 254.4M figure.

In contrast, SCR has about 214.2M shares outstanding as of May 15. As of March 31, Waterous owns about 79.6% of those shares, so give or take 170.5M shares. As part of the proposed M&A, Waterous will buy an additional 21.4M shares at $30.92/share, thereby increasing its ownership stake to 192M shares and infusing the company with $660M of cash.

SCR proposes to exchange 0.62 share of SCR for 1 share of MEG (and $4.10/share in cash, but we’ll address the cash later). At the end of the “share-for-share” exchange (i.e., 159.4M shares of SCR for 257M shares of MEG), SCR’s total outstanding shares will increase to about 393M shares.

So how much of SCR will WEF own? Prior to the acquisition it owned 170.5M share of SCR. Couple that with the 21.4M shares it just subscribed for, WEF will own ~192M shares in total. 192M shares divided by 393M shares outstanding (i.e., 48.8%) means WEF suddenly owns less than 50% of the newly combined SCR/MEG company.

That can’t be.

So either increase the numerator (shares they own) or shrink the denominator (outstanding stock).

They chose the latter. As part of the hostile takeover, SCR has already acquired a nearly 10% toehold in MEG shares in Q1 and the beginning of Q2. The below chart shows the dates and prices they paid for the purchase of those 23.4M MEG shares.

Do some “maths” on that info above and you get an average price of $24.10/share. Remember this number $24.10/share, we’ll come back to it.

So 23.4M shares of MEG owned by SCR. Consummate this merger and every single share will covert to 0.62 share of SCR, or 14.5M SCR shares. SCR likely cancels these shares, and so in the end, total SCR shares outstanding will fall from the 393.3M shares to about ~379M, shrinking the denominator. Let’s double-check that . . .

Yup makes sense. So post-acquisition, they’ll own 192M shares of SCR, divide that by 379M shares outstanding . . . > 50% control.

Okay the share count work out. WEF retains control and SCR gains liquidity in the public market as 190M shares (i.e., the piece WEF doesn’t own) circulates in the market allowing for greater liquidity and investor exposure. 192M shares probably means about 1-2% of it is traded on a daily basis, which is a few million shares transacted, not too shabby.

Moolah

What about the cash portion? How does that work? Well remember, as a MEG shareholder you receive 0.62M share of SCR for every share of MEG you own, but you also receive $4.10 cash for every share. 257M shares of MEG means SCR will shell out $1.05B of cash to MEG shareholders. Since it’s also a MEG shareholder (given the 10% toehold stake), $95.9M of that cash, will “round trip,” as it’s paying itself. Net/net we’re looking at a cash outlay from SCR of $958M.

Does SCR have the cash? Not so much.

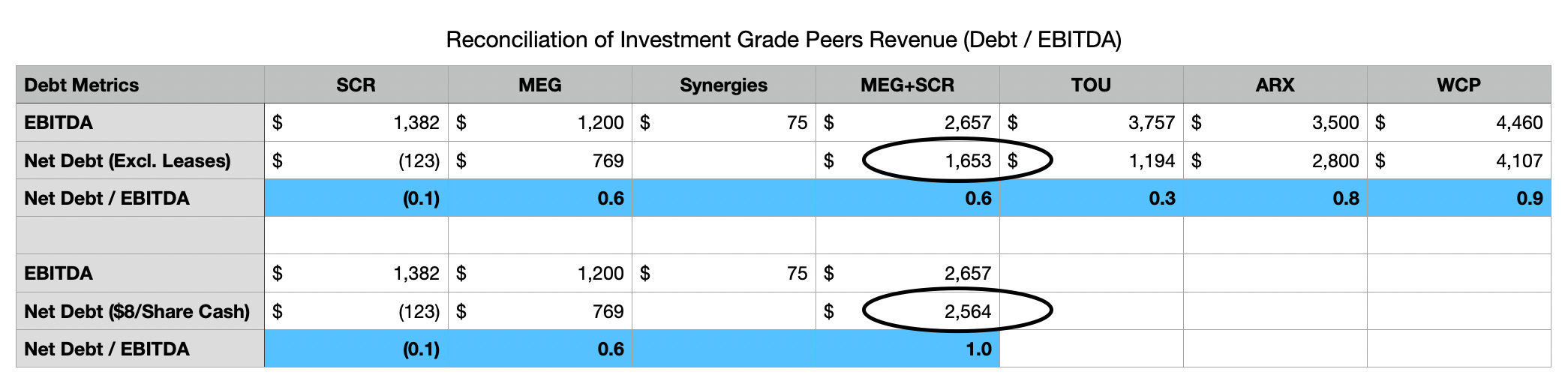

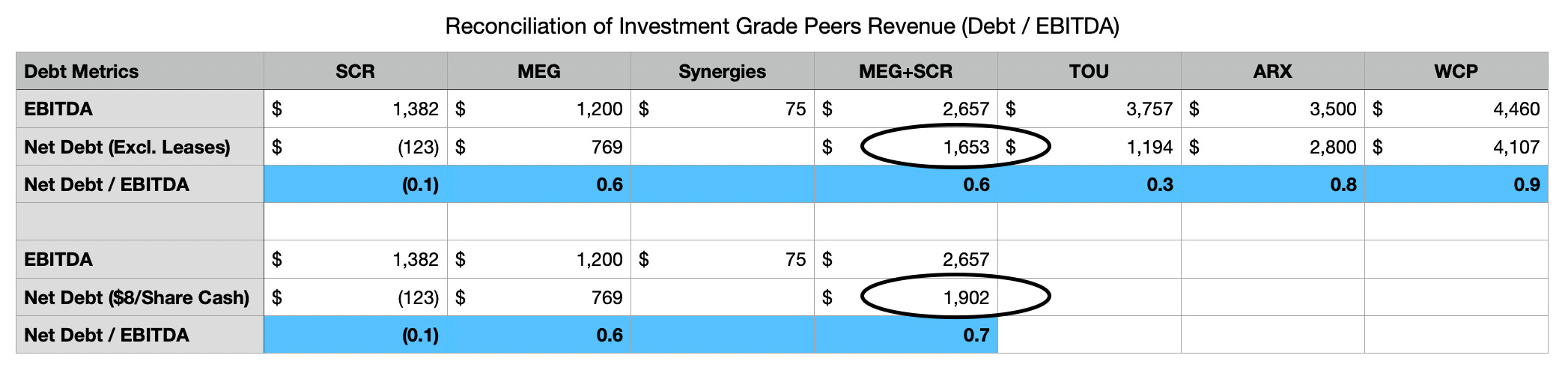

After the Montney disposition, SCR estimates it’ll have $123M of cash on hand. MEG has some debt ($769M), so the $958M will need to be borrowed. Total net debt of this combination overall? $1.653B (as SCR will borrow the $958M) if we go by March 31 figures. This $1.653B is important because it lays the groundwork for one of SCR’s reasons for effecting this merger. Synergies, and specifically debt issuance costs.

If you hit certain metrics, this combined entity gets an investment grade weighting, which equates to a 1.25-1.5% lower interest rate, or cash savings of $25M. Dig into the footnotes and you find out that what you’re looking for is effectively keeping Net Debt / EBITDA below 1x. This fits with what Adam Waterous calls “low leverage” (as he typically seeks to keep Net Debt/EBITDA around 1-2x) and the current combined entity would come in well below that at 0.6x.

Yet, here’s the thing. The calculus above raises 2 questions: 1. is the deal palatable if the cash component for MEG shares (which will be borrowed) is only $4.10/share, and 2) . . . where’s the $660M from WEF’s subscription of 21.4M SCR shares at $30.92/share?

We think the answer to the first is a resounding no, and it’s obvious why:

MEG’s current share price is trading 8-10% above where SCR is bidding;

SCR itself has already paid an average of $24.10/share for MEG shares in Q1/Q2 . . . a figure that is above its own bid price.

Given these two factors, there’s likely to be a “flex” on the premium being offered, and likely why the market is trading closer to what SCR paid for those toehold shares. Interestingly, after the Offer to Purchase was sent out, the exchange value for MEG closed at $24.02/share (surprisingly close tot he $24.10/share WEF paid for it’s 10% MEG shares earlier). SCR will almost certainly have to pay-up for MEG shares to convince the remaining MEG shareholders to tender, and the flex will come from the cash portion. It can’t be more equity, since WEF is already close to the 50% majority threshold and issuing anymore shares would result in the loss of control.

So cash it is.

We don’t think an extra $2/share would do it (bringing it to $6.10/share) either. While it would effectively close the gap between the bid and the market’s current price, we’re not sure the premium will be high enough. Merger arbitragers are in the stock now, and may need to be induced to tender as well.

Let’s try $8/share. If the cash consideration were to be increased to $8/share (i.e., $3.90/share above the original $4.10/share cash offer), Net Debt of the total combined entity would increase by another ~$910M (i.e., $3.90/share * 237M MEG shares (257M MEG shares less SCR’s 10% 23.4M shares). Note for here we’re using 257M shares for MEG because the PSU/RSU need to be cashed out).

Net Debt to EBITDA would increase from 0.6x to slightly below 1x, but still remain below Adam Waterous’ preferred 1-2x ratio. Sill, that’s not the whole story. Again, what about the extra $660M from WEF’s subscription? Remember, to subscribe to an extra 21.4M SCR shares, WEF had to make a capital contribution of $660M. Factor that cash in and Net Debt falls to $1.9B.

At $1.9B, the Net Debt / EBITDA ratio consequently falls to 0.7x, below ARX and WCP’s ratios in the above examples, thereby preserving the investment grade possibility. The above also doesn’t factor in any free cash flow the companies can generate between now and the hypothetical closing, which would help lower Net Debt levels.

It’s important to remember, this likely isn’t SCR’s last rodeo. The company is almost certainly going to embark on future M&A activities, and the investment grade rating and its resulting lower cost of debt, helps in funding any future acquisitions.

For now though, the Offer to Purchase will last until September 15. Meanwhile, MEG’s management team and board of directors are busy crafting a response to the offer. It’ll be a “no,” but the negotiation can really begin in earnest. A white knight could also emerge, but we wouldn’t count on it. Frankly, we likely don’t need one if the premium moves up a bit here. Again, it’s not the management team or the assets we’re getting with SCR that’s the main issue, it’s the price for how to get there.

An $8/share cash premium (coupled with the 0.62 SCR share), means the overall premium increases from 9.3% to 27.6% (from MEG’s original unaffected price before the offer was announced on May 15). Had SCR offered that type of premium (i.e., around $26/share) when MEG was trading at $21.30, then the chances of a quick transaction would’ve been higher, but it also could’ve put the company in a bidding war situation, and having MEG get priced out of its reach. Given the potential suitors/white knights out there (e.g., Cenovus, Imperial, Suncor, etc.), SCR conservatively bid it lower (lower in fact than the 10% of shares it had already purchased), and will wait and see what transpires from here on out.

Ultimately, we do think MEG will sell, but higher than the $24.02/share we’re seeing on the screen today. Stay tuned.

Please hit the “like” button and subscribe if you enjoyed reading the article, thank you.

Interesting perspective. MEG’s been dead money—shareholders should take the SCR deal. It’s a good asset, but poorly run and inefficient. In a $60 WTI world I think a lot of MEG shareholders are unrealistic. Sure, SCR might bump the offer slightly, but there’s no white knight coming. That’s already obvious.

I don’t think we have price discovery in SCR so it’s hard to say the offer is too low. If SCR was already in the S&P/TSX Composite I would be more inclined to agree with you.

Ultimately, this offer is attractive to MEG’s biggest shareholders as they get shares in a company with almost double the equity value and can increase their positions whereas their size was limited by the size of MEG. Plus as SCR’s free float slowly expands it will result in flows into MEG resulting in multiple expansion.

Finally, SCR can roll in GFR as well which will another tier one oil sand asset, growth, a bigger float (more index impact) and an NYSE listing.