TACO Supreme Served at the Strait of Hormuz

June 13, 2026

Alright alright.

Ladies and gentlemen we have a deal!

Greatest meal deal ever. It’s like a Tacos Supreme Combo.

3 luscious Taco Supremes plus an ‘Murica sized big gulp of sugary carbonated water to help all that medicine go down. Mary Poppins couldn’t be prouder.

Eventually . . . and inevitably, we figured he’d cave. He had to. He had no leverage. He literally backed the USS Boxer, and its Marine Expeditionary Unit, away from Asia a few weeks ago, which was a pretty big signal that he didn’t have the stomach to escalate the situation. In turn, Iran had to translate its military leverage into a diplomatic one, and it has. Could it or should it have waited until the markets dislocated, and the global economy came to a grinding halt? Debatable. Moreover, Iran has to be suffering economically as well since their oil flows have plummeted because of the US oil blockade. Regardless, I for one am glad they didn’t. So instead, they relented a bit and signed (or will sign, or will sign shortly after Trump’s birthday tomorrow) a Memorandum of Understanding (“MOU”).

The MOU has six general points:

Lifts the blockades on the Strait of Hormuz (“SoH”) within 30 days. Iran will clear the mines, and not collect tolls, whereas the US will remove its blockade. Iran has claimed it will charge service fees to facilitate transit so that outcome is still in the air. We think that’s likely. They’ll get something, but something that’s palatably worded for the world. Facilitation fee, support fee, or security fee, something. It’s all about optics.

Iran commits to never pursuing a nuclear weapon. It will agree to either a 15 or 20 year halt to uranium enrichment and dismantling of its nuclear sites. The parties will negotiate the technical details of the monitoring over the next 60 days. Most likely, they’ll end up in a state where they keep the uranium on their soil from which they can enrich the uranium in small concealable batches (as if inspectors will prevent them from developing a nuclear weapon, which they’re infinitely more motivated to obtain).

Hostilities against all Iranian proxies (Hezbollah, Houthis, etc.) will cease. Israel has claimed it’s not part of the MOU, but we think the US has enough sway over Israel that even if there are violations here, they’ll be small and both parties (Iran and the US have incentives to overlook it).

Missile program - Iran will keep this. Don’t expect much movement here.

Compensation - Iran has asked for $270B in reparations for war damages, and the US will likely grant the release of $24B held in banks worldwide. They’ll release those funds as conditions are met, but expect a “sign on bonus” for Iran. They’ve asked for it, and they’ll get it.

Sanctions - oil and gas sanctions on Iran will be lifted immediately. So Iran should be able to start recovering economically.

So framed another way. This is a 60 day ceasefire that reopens the SoH for 60 days while the parties sit and negotiate the specifics of the nuclear deal. Don’t read that as a threat or chance that we’ll go back to war.

President Trump has shown zero appetite for that, and wants to immediately restore the SoH.

Most likely, the US will end this entire endeavor with an IRGC in a strengthened position. It’ll get sanctions lifted, billions in cash, retain its missile program, and exercise de facto control over the SoH. As sanctions lift, they’ll rearm, refortify, and upgrade their weapons package. I fear that’s the longer-term scenario. This is an emboldened and empowered entity, and the US an unfortunately embarrassed one. Iranian drones and ballistic missiles have shown that the emperor has no clothes, and with that, it’s stripped the US of its cloak of perceived military invincibility. The lesson that quantity has a quality of its own has been retaught, and that a continuous barrage of cheap munitions can economically and strategically hobble your foes.

Impacts on Oil

Putting on our investor hat though, what this allows us to do is to reframe the oil trade. What the administration has orchestrated in the past few months has been nothing short of phenomenal. It’s kept energy prices rangebound and arguably under control as it’s weaponized the volatility of the paper markets. We’ve known all along that the paper market is >30x the size of the physical one, and in the short-run that can push physical price indicators aside. Trump’s team has successfully eviscerated investors’ appetite/ability to take bullish positions in the front of the curve. Given the volatility that each tweet engenders, holding positions became untenable. In fact, the risk/reward eventually favored shorting the oil market, and that’s what investors did.

Combine bottomed out sentiment . . .

With high short-positioning . . .

. . . and eventually once the headlines flipped to a favorable peace deal, the bottom softened for oil prices.

So $80-85/barrel it is for now.

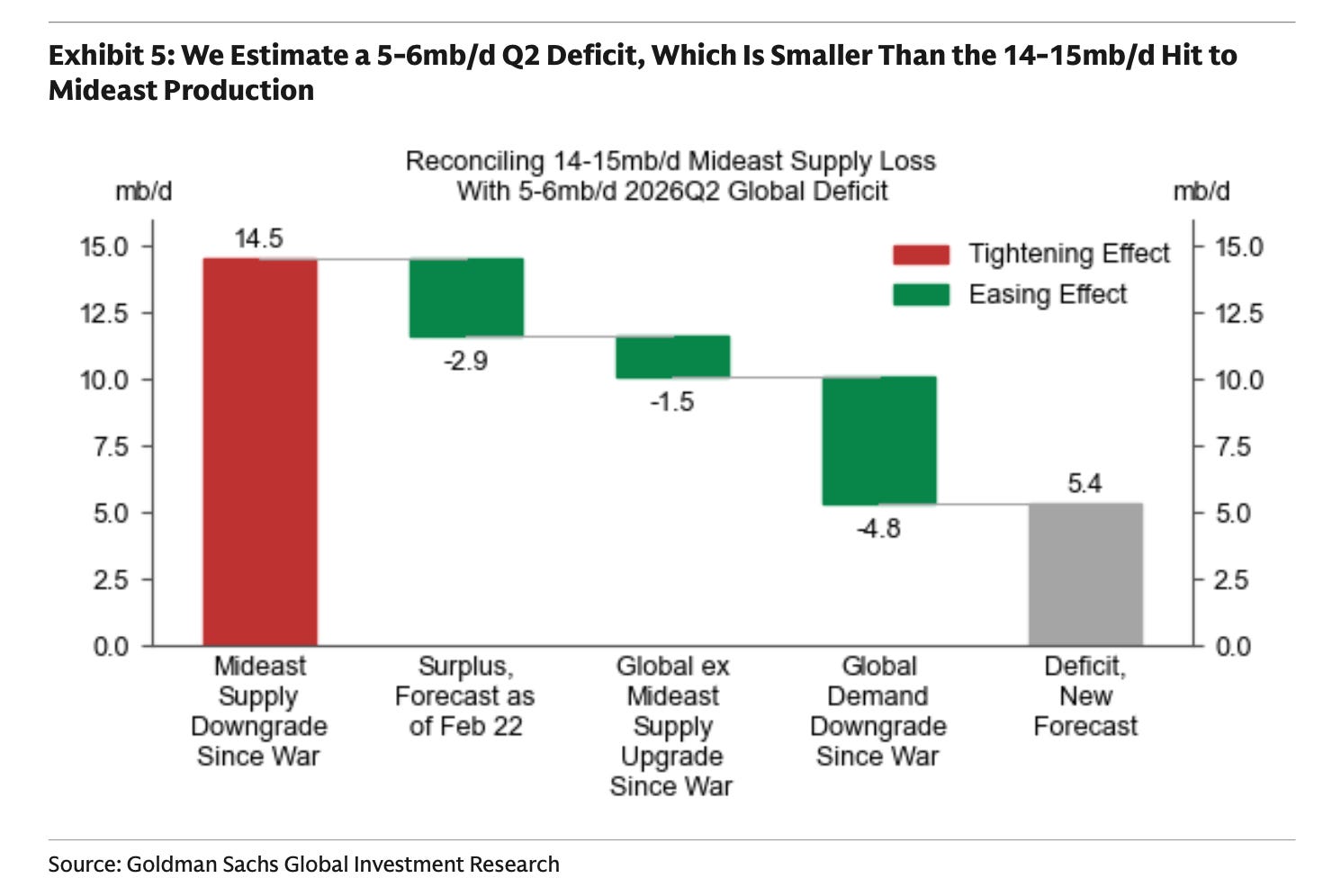

Lower Chinese imports coupled with reduced demand has mitigated the otherwise enormous 14-15M bpd supply loss. As of now, it appears that the collective voluntary measures have reduced visible global draws in Q2 to ~5-6M bpd (note the key word “visible”).

We think it’s higher as some of that is really due to seasonality, and China’s reduced imports and lower refinery runs means it likely drawn down product stocks. Still, price doesn’t lie, the price on the screen says $85/barrel, even if we think visible and less visible inventories have drawn.

So what’s next?

What’s next is the recovery.

How fast and when?

For takeaway capacity, it’s a no brainer. The Middle East (Iraq, Saudi Arabia, UAE, etc.), will quickly and furiously build/expand their alternative pipelines. Iran has proven it can weaponize the SoH at any time, so export capacity needs to be increased. UAE should be set by 2027, and the Saudis undoubtedly soon after. Will the upgraded pipelines like Yanbu and Fujairah be under threat? Sure, but they’re arguably easier to repair than prying open a strait under enemy fire.

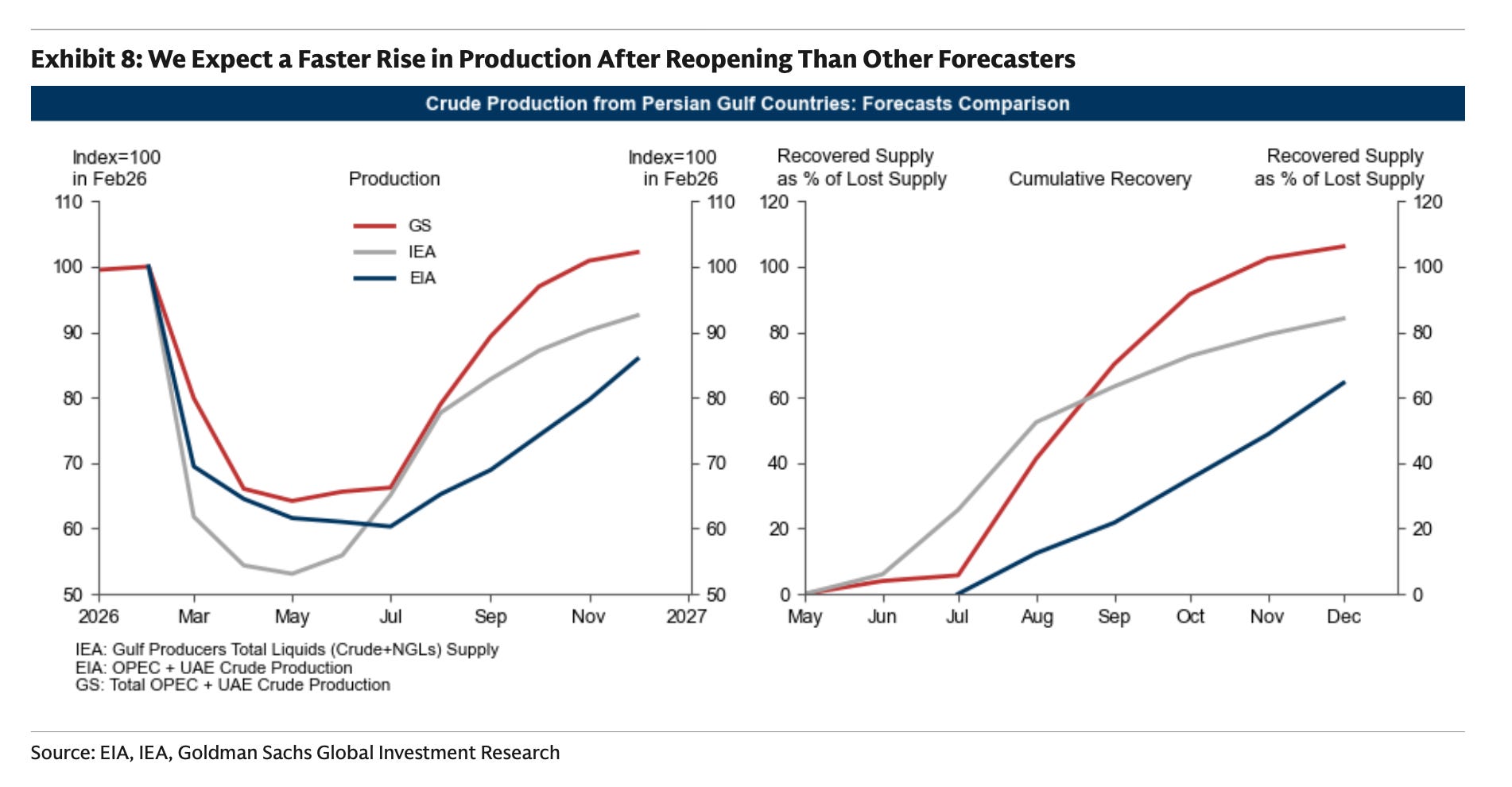

As for supply recovery, we have to assume that it’ll take about 2 months. That’s the time needed for ships to exit the Gulf, unload, and return. Only by returning can tanker ships then drain onshore storage and allow producers to restart production.

The ships currently trapped in the Persian Gulf will leave first, transferring around 100M barrels that are sitting in floating storage to hungry Asian/European customers. That immediate shot of adrenaline should help keep prices steady as we get through this busy/high demand summer season. On the flip side, demand should also recover as energy prices climb down from their highs, and summer burn increases to counteract the heat that begins in earnest. We’ll still have a net shortage, but if China maintains its posture on reduced imports, we can muddle through. Call it a visible draw of 3M bpd draw over the next 60 days. By September, we should be ~80% recovered on supplies. Thereafter, near or full recovery by year end. We think that’s a decently conservative estimate, and largely what the energy agencies and Goldman Sachs thinks.

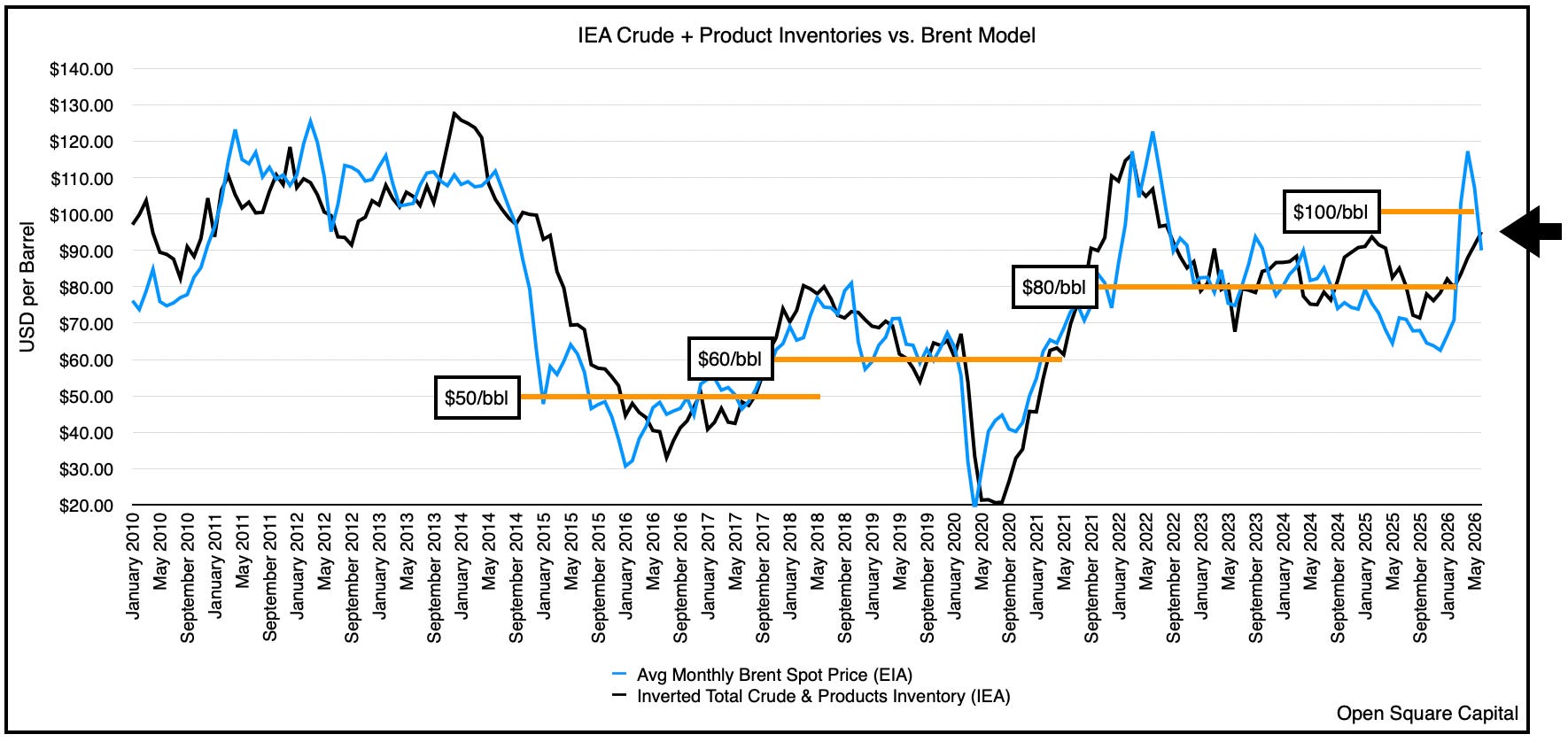

This does mean oil will continue to draw in the coming months. Largely because of the lag effect of sailing times/production restart/disruption, seasonality, and uncertainty as we muddle our way through this MOU. Fair value for oil is nearer $90-95/barrel right now (below is only looking at commercial stocks), and will nudge higher in the next few months as we recover.

The path thereafter depends on production recovery vs. demand growth.

Will there be lasting impacts to the prolonged shut-ins (we doubt it), will the SoH navigation return to pre-war levels (we also doubt that), will producers ramp production much higher in an $80-85/barrel oil environment (yes, but muted), what will the geopolitical premium be going forward (who knows), and what type of strategic petroleum reserve restocking/build will we see (definitely incremental demand)?

All of these things are still uncertain, but we’ll start modeling them as we move forward. It is safe to say that in the past 3.5 months, we’ve managed to materially drain our inventory reserves and commercial stocks, strengthen a Middle Easter foe to a previously unfathomable position, and severely degrade our perceived ability to project power and backstop/defend alias in a volatile regions.

While we’ve managed to temper oil prices in the short-run, the knock-on impacts will almost certainly reveal themselves as we emerge from the fog-of-war. Shell’s CEO has stated that we’ve globally lost ~1.2B barrels of oil in the past few months, and we think that’s about right. We’re approaching tank bottoms these days, and though we’ve managed to pull-back from the global brink with help from Chinese reserves and a minor reduction in demand, we’re going to get tight if they don’t continue with their largesse. As oil prices drift lower here in the coming days, they’ll find a floor. Once the dust settles, and short positioning clears out, don’t be surprised to see prices drift higher as we keep drawing into the summer. We still expect prices to average ~$90/barrel for the rest of the year, and we should have a better view into 2027 as we get into Q3. Suffice it to say, energy companies are still pricing in $70-75/barrel. So those should receive another uplift.

As we’ve done throughout this whole exercise, we’ve kept repeating the phrase “we shall see.” Just when you think something is set to happen, another entirely unexpected situation unfolds. In January it was $55-60/barrel for years to come . . . and then the market gave us triple digits. Low prices have created pervasive apathy towards energy security, and it’s bred overconfidence that we can seek regime change for a major producer without destabilizing energy prices. Well we found out. Turn the page, and we’ve decided to suppress oil prices for the greater good as inventories draw. Yet meanwhile, we expect producers to refill our emptied tanks even when the economic incentives to do so are uncertain? Hmm, the producers appear to be as skeptical as we are.

2026 is the year the US lost a war in the Middle East, and we don’t think that means energy prices will be, or should be cheaper going forward, nor do we think suppressing oil prices and introducing volatility in the oil market will lead to producers running flat out as we come out of this mess.

Again “we shall see” . . . in the meantime, enjoy your tacos on your birthday Mr. President.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

Excellent. At $80 pricing deck, it's like fishing with dynamite in the energy sector to find names with excellent return characteristics from here on out.

The transportation capacity is contracted on a monthly basis. When the waterway is closed or faces risks, the transportation company will dispatch the cargo ship to other routes. If they want to return the transportation capacity to the original route, it will take at least half a year to restore a certain amount and the prerequisite is that the conflict area has entered a substantial ceasefire.