The Last Question: No Easy Answers for Energy Investors

December 16, 2023

You better be good.

That’s what I’m thinking before it starts. It’s my second go-around this time, the first being a few years ago in front of my daughter’s third grade class. Now it’s my son’s turn.

I apparently did well enough back then to be invited back. Though that’s a low bar with kids.

“Everyone this is Mason’s dad, he’ll be teaching you about the stock market today . . . .”

Oh boy.

62 little eyeballs, 31 fidgety butts . . . one hour.

You better be amusing old man.

My son chuckles nervously.

Here we go . . .

“In order to understand stocks, you have to understand business. A business is any activity to make a profit. What’s an activity?” Tiny sausage fingers shoot into the sky.

Horrifically wrong answers rain down, hurting my brain, but I persevere like the trooper I am.

“Well . . . it can be an idea . . . that you then make . . . that you then sell. So think it, make it, sell it. So what’re the activities? Think it, make it, sell it!”

They repeat the mantra. Think it! Make it! Sell it! Think it! Make it! Sell it! . . . yes, yessssss, repeat the words.

Our cult is working!

They chant in unison, and with enough fervor to summon the market gods while my altar boy of a son hands out chocolate covered coins as rewards for their enthusiasm. Little dopamine hits rain from the sky. Pavlov would’ve been proud.

“It can be any one of those three, or any combination of two of them, or all of them. Out of the three activities, ideas are the most powerful.”

Then I show them this and ask, “what’s this and how' does it make you feel?”

Again sausage fingers reach for the skies! It’s three mountains! WRONG! Those are three tiny triangles! WRONG!! I need to go to the bathroom! TMI!!! I’m yelling maniacally with clenched fists, so that each criticism lands like an angry boot, crushing their budding confidence grown in a nursery filled with participation trophies. I’m intellectually dunking on third graders . . . and it feels soooo gooooooood.

“What if though . . . what if I replaced the three triangles . . . with circles. How do you feel now?”

BOOOOOM!!! Minds blown. Like edamame shooting out of their ears, some practically jump off the rug with glee as the intellectual property cattle prods their dopamine centers. I SEEEEE the Mouse. I WANTS the Mouse. I NEEEDS the Mouse.

It’s game on after that. With their eyes wide open, I can read their minds. This old man might just know a thing or two, I shall listen, but only IF . . . he continues to AMUSE ME!

My son’s chuckling now, more in disbelief that this is actually working, and in total relief that my dad jokes actually work on real life people.

We talk about intellectual property, we talk about marketing and advertising, and we talk about manufacturing in China, India and Bangladesh. We talk about all these things and we talk about profits. We talk about the market and why things seem to go up and down, and we talk about competition.

More slides with animations, some sprinkling of jokes, and questions. So so so many questions. Surprisingly, many insights as well. This really is a precocious class.

We laugh, we cry, and we cringe for 50 minutes. It’s great.

The hour’s almost gone now and they’re getting fidgety. You try sitting criss-cross applesauce for an hour. I glance at the teacher, and she says it’s almost time to wrap-it-up, and as we do, a hand goes up.

Back row. “Yes?”

“So I was wondering . . . what stock should I buy?”

There it is.

There’s the question.

What’s fascinating about that question isn’t that the question was actually asked, it was that the question came out last.

For 8 year olds, that’s the last question that’s asked. For adults? It’s the first.

It’s often asked aggressively and passive aggressively. Oh you run a hedge fund? So what’s a good stock to buy? What do you own? What’re you buying? What’re you looking at these days? What looks good? What’re you seeing that the market isn’t? How are your views differentiated? See anything interesting????

I get that question all the time. It’s an occupational hazard. It’s to be expected because it’s the easiest thing to ask, and people always want to know. There’s nothing wrong with the question per se, but investments and portfolios typically express a view. If done right, it should be the distillation of a macro view to the micro. From global economy/macro liquidity, to a sector, to a specific business, to a stock. To some extent, it’s all interrelated. Yet, investors often skip ahead to the answer. It eschews any of the context, perspective, or questions posed that preceded it.

The reason I bring all of this up is because of our energy investments. Many commentators today seem to be jumping ahead. For them, prices are the answer, they’re the be-all-end-all. The popular notion? The recent fall in oil prices is attributable to the impending recession. In fact, the collapse in prices could mean we’re already in a recession.

So quickly? How did we suddenly deteriorate so rapidly in 2 weeks as to account for the recent collapse in crude prices?

Don’t argue, the prices tell us everything, and spreads and front month prices are collapsing. So it must be weak.

Okayyy . . . .

Silence! Prices are lecturing!

It’s not just the recession, but there’s also the notion that China’s reopening will fail and they’ll U-turn on their abandonment of Zero-Covid Policy (“ZCP”). Possible? Sure, but again very unlikely. Imagine the social unrest if the central government backpedals on something the populace actually wants, and some even demonstrated for. The Overton window has already shifted, and the population will accept higher confirmed cases and death tolls in exchange for economic advancement. It’s a tradeoff, and one they’re willing to make after 3 years of nothing. Here’s China’s mouthpiece if you’ve any doubt.

Sure cases have risen dramatically, but this was always the way out. It needs to go-up to confer greater immunity, and it needs to go-up before it can finally go down. Like any COVID wave, we think this will take six weeks. Six weeks up, then six weeks down. By late January (coinciding with Chinese New Year), the Omicron wave will have abated. Movement/business activities will pick-up again. I’ve had COVID, you’ve been boosted, let’s party. 新年快樂!

In the interim, there will be weakness. More than those caused by rolling lock-downs that we’ve seen? Doubtful. Certainly flat refining cracks don’t seems to point to that. If anything it’s the old adage of “hurry up and wait,” as we wait for the recovery that should happen, could happen, or maybe will happen? Keep the faith though because we think it will. There’s a reason this is happening.

After the storm abates, a financial deluge will then occur.

Yes, that’s coming because like my son’s third grade class, we’re going to need some sugar to get everyone jacked after 3 years of ZCP. Chocolate gold coins for everyone. Sure it won’t be like the direct financial stimulus we mainlined in the West, but it’ll be something. Well, it’ll be ALOT of things, so we’ll have to wait.

Again . . . solid reasons, but . . . Silence! Prices are lecturing!

All of this is tough to see. There’s too much nuance and uncertainty to this, whereas it’s obvious what oil prices are doing today. When oil prices fall this quickly, it’s easy to skip to the answers and declare that the recession is upon us, it has/will collapse oil demand, and we are done for. Are we? The structural undersupply is worsening, inventories have drawn to low levels, public policy adverse to energy development have yet to reverse, and one of the world’s largest economies is emerging from three years of economic malaise and neglect.

None of these factors matter because “the market knows them already.” So maybe it’s probabilities then. If that’s true, how does “knowing” the factors above mean they’re less probable than the “impending recession” and doubts surrounding China’s reopening. We can at least see the data on the first set of “knowables,” and we can say assuredly, the story appears intact.

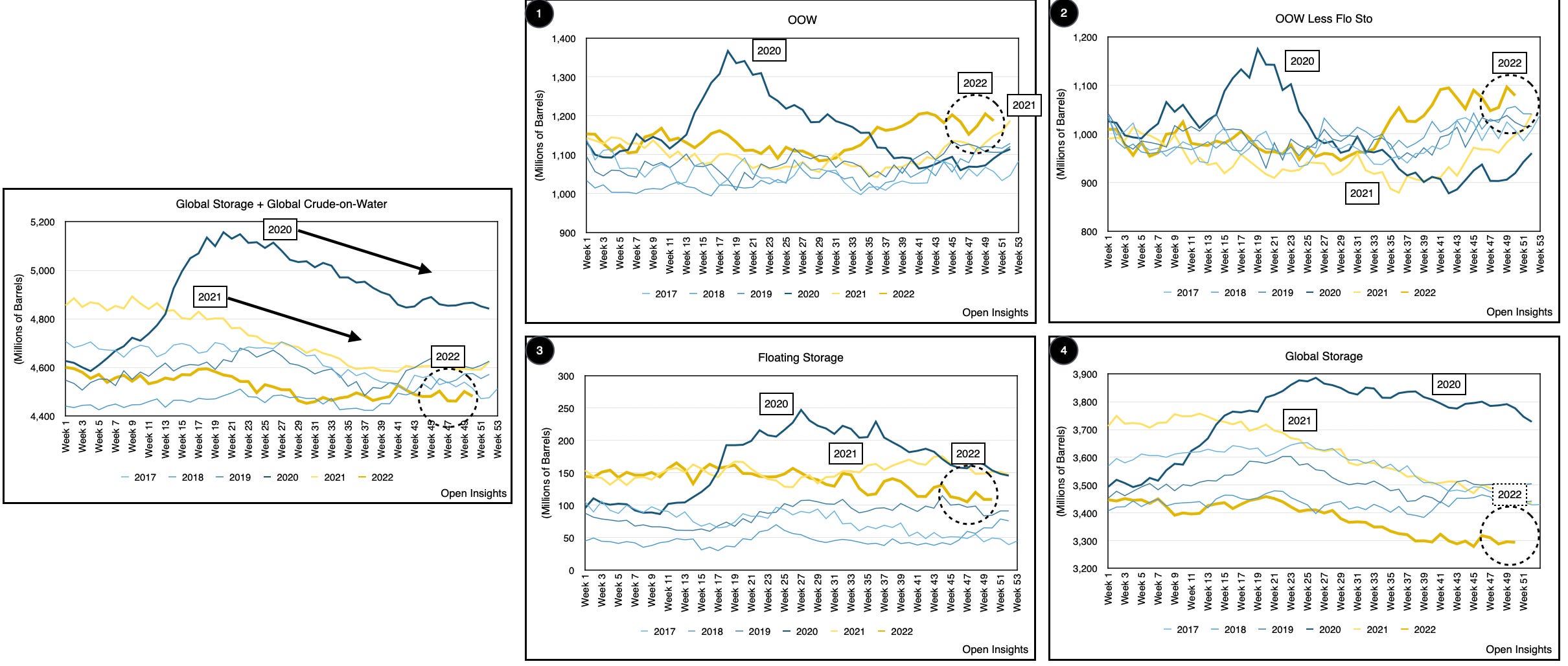

This is 2018 again, so they say. Well let’s zoom in. This is the amount of crude in the system (as of last week) vs. 2018 (orange line vs. 2018 “bubble” line).

Note the difference? Note how after week 39 in 2018, crude inventories began rising substantially into year end? This was then followed by a 2019 US/China trade war. Today, we’re instead flat and looking at a 2023 China reopening.

Silence! Prices are lecturing!

No matter. The price is the price. We are humbled enough as investors to know that you can’t fight the market (nor should you). Like Buddhist monks, we must accept what is, and not hold so firm onto what is not. If you’re long, maybe trim some positions as we wait for the world’s tail risks (Chinese demand growth / Russian exports decline) to emerge as real risks.

Maybe all of this, however, is just a matter of timing. Things will happen when they happen. Commentators are right that the physical market does look soft today and they are right that there is de-grossing and de-risking into year-end, whether to protect bonuses, or preserve capital. They are right that because oil is heavily financialized (i.e., for every 1 barrel of physical oil traded, >30 “paper barrels” are traded), it’s sometimes the market’s chew-toy for self-expression. From the price swings, we’re definitely very emo today.

We’ve cautioned for a few weeks to be careful here. Thin liquidity, a bipolar market, and a bearish economic backdrop makes for choppy waters. We’re still bullish even if our year-end oil price target was resoundingly rejected (laughably, we thought over $110/barrel by year-end). Back to the drawing board for 2023, but at least one propped-up by a hundred plus million of fewer barrels.

Despite all this, we think the factors mentioned above will matter. Eventually, what’s “known” will be fully priced in. After all, the physical disciplines the financial . . . so they say. Like third graders though, we just need to keep asking the questions, and keep in mind it could just be timing.

They don’t know any of that though. They’re just third graders listening to a presentation, and they want to skip ahead. At least it’s the last question.

“What stock should I buy?”

So I tell them.

After all, it’s elementary.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

I SEEEEE the Mouse. I WANTS the Mouse. I NEEEDS the Mouse.

Fantastic. For real, amazing.