The Oil Market . . . in a Nutshell

December 8, 2022

Brent prices have fallen over $10/barrel from $88/barrel to $77 . . . in only 3 days. This isn’t about fundamentals. At least that’s what we’re thinking. It’s unlikely because how do you have money managers coalesce around the idea that the economy will nose dive so quickly and materially as to warrant an oil price sell-off like we’ve seen.

The market’s efficient, but THAT efficient? Doubtful. So we began searching. Reaching out to all manner of contacts; wonderful industry folks who we’ve befriended these past few years. Some have shared that they heard a rumor (Bridgewater exiting their oil positions), others have shared it’s a technical issue (seasonally low liquidity coupled with high volatility means selling begets more selling), and even more have said it’s behavioral (energy investors who have outperformed this year have decided to take their balls and go home).

It’s something we alluded to here . . .

Interestingly, the Bridgewater rumor from multiple sources was preceded by (or was it followed by, as one can never really tell) this . . .

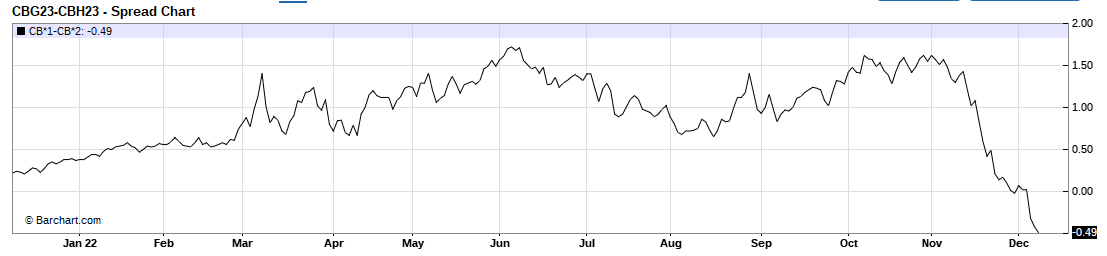

No, no, you fools. Tis’ not Bridgewater, that’s water under the bridge. It’s the reawakening of the hibernating energy bears. After rerunning their forecasts, the market is anticipating an inventory build in Q1 2023. As financial conditions tighten and rates rise, the economy is slowing and energy demand is trending negative. The chances of a recession has ratcheted higher. You can see it in the collapsing physical market; the deteriorating refinery margins and crude contango.

The physical market is screaming weakness in the real-time data, so fundamentally it’s bad.

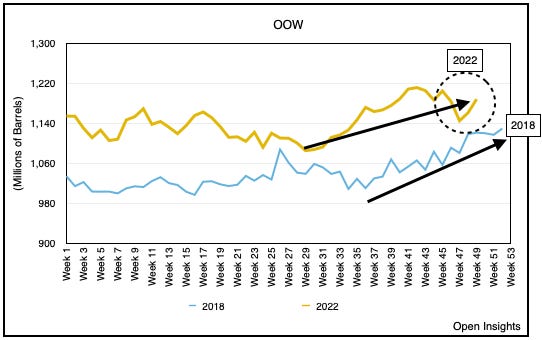

Is it though? Because that other set of contemporaneous data (inventories) seem kinda flat. Tally up all the crude, oil on water has trended higher, but once landed, land storage is absorbing it.

Doesn’t matter because this is 2018 all over again . . . when a deluge of Trump induced Saudi quid pro quo softened the physical market. Coupled with a Fed “we’re a long way from neutral” shock, the oil market promptly surrendered into the year end. As it was then, it is now.

Replay 2018

Fair enough, instead of the Saudis, we have the Russian understudy filling-in for this year’s rendition of the Nutcracker. Certainly oil on water appears higher as Russia redirects its barrels and stuffs the channel before the embargo/price cap snap into place) . . .

Yet, this is 2022 vs. 2018, and if we look at the picture holistically. Hmmm.

Furthermore, unlike 2018 when US / China relationships were leading up to a trade war, China today is instead preparing to exit its self-imposed COVID lockdown, which should drive higher energy consumption moving forward. You’d think that’d help, but alas no.

Sound of Silence

What’s equally fascinating is the silence from OPEC+. Curious because only a few months ago, a fall from +$100/barrel to $83 warranted a 2M bpd nominal cut (~1M bpd in reality) after OPEC+’s de facto leader Prince Abdulaziz bin Salman uttered these words about “volatility” . . .

Heck, this is a man who wants to make those who bet against oil “ouch like hell,” but mums the word at $77 eh? I wonder if it has anything to do with this . . .

Nah it couldn’t be, right? Oil prices crashing ahead of a 4 day China/Saudi Arabia summit designed to weaken the West’s ties with the Kingdom. Incredulously, all of this was preceded by a broad Chinese announcement that COVID restrictions were lifting (which ostensibly should’ve spiked oil prices), but didn’t. Maybe, just maybe, the Chinese aren’t that incompetent in planning its grand reemergence after-all?

See you’re doing it again, looking for a shadow in the corner where there are none. Need more string for your wall diagrams?

Still . . . if you can make shorts “ouch like hell,” isn’t the inverse of that statement also possible some how/some way? Throw in the fact that we know Chinese buying has been muted . . . okay enough.

The silence though is . . . deafening. Oh wait, we did hear this . . .

Awesome.

So what is it? Is it falling demand? Deteriorating fundamentals? Technical selling? Market management? Behavioral? Fund positioning? Seasonality?

We’re not sure. That’t the truth.

We’re not entirely certain. We have doubts it’s a fundamental issue (i.e., everyone woke up on Monday and decided, yes, the world is collapsing? Tough to believe). Could it be an analog of 2018? Sure, entirely possible. Could it be Saudi management ahead of a critical meeting? Possible, but also conspiratorial and we hate those lines of reasonings. Could it be technical? Most definitely.

Sometimes, the catalyst matters less than the reaction. Whether it’s one of the largest, most sophisticated hedge funds blowing out of their energy positions, or something more mercurial, the volatility and timing of the sell-off means everyone’s going to risk-off into year end. Especially if you’ve killed it this year.

We’ve moved up the Christmas party to this week folks, see you next year.

That’s what our contacts are saying and it’s broad based and across multiple fronts (e.g., hedge funds, traders, portfolio managers, pods, industry folks). Sentiment, liquidity, and volatility are all tied at the hip, and if one goes off the cliff, they all go off the cliff. So be careful and cautious out there into year end. There’s no need for bravery right now in the face of uncertainty.

While none of the above materially alters our view that the market is in a longer-term structural deficit. Note, however, the key words . . . “longer-term.” There’s little asymmetry in the risk/reward in the short-term. You can’t fight the market here, as it’s too uncertain and can be too forceful. So for us, we’ll simply bob along with the volatility and keep observing, watching for signs of a turn.

Unfortunately, for the time being, we keep watching reruns of . . . the Nutcracker.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

Thank you for your insights!

Comedic prose, structual message. Good stuff/