This Isn't a Bubble . . . That's Coming

September 7, 2020

You need four things for a proper bubble. One that can befitting of the other ones and can take its proper place in the pantheon of other manias and subsequent crashes. Charle Kindleberger and Robert Aliber’s treatise on the subject Manias, Panics and Crashes tells us so.

What are the four?

#1 - An Exogenous Event

The first is an exogenous event, a shock to the financial system. Something big, something unexpected. It can be a war or conflict, or it can be a new breakthrough, a technological marvel that sparks the imagination (like the internet), or it can even be . . . a pandemic. As Kindleberger explains, these events are “ . . . sufficiently large and pervasive, the economic outlook and the anticipated opportunities would improve in at least one important sector of the economy. Business firms and individuals would borrow to take advantage of the increase in the anticipated profits associated with a wide range of investments.”

We think COVID qualifies as a gobbler of a Black Swan, material enough to shake our economic Etch-a-Sketch. What was an accelerating migration to online e-commerce suddenly became an avalanche as we sheltered in place and worked from home. As Shopify’s Chief Product Officer Craig Miller said “It almost became 2030 overnight.”

Any company or industry that didn’t already have an online presence, or at least not a robust one, suddenly had to pivot. E-commerce platforms that were complementary to your physical retail experience now had to lead for companies to survive. As Shopify’s CEO Tobi Lutke states “Some of the things we anticipating as being important over the next coming years became super important basically overnight . . . .” In short, technology, and more importantly the ability to access customers, obtain and analyze customer information and transact online/deliver offline have become invaluable going forward. What was ancillary to your business is now your business. So check there.

#2 - The Juice

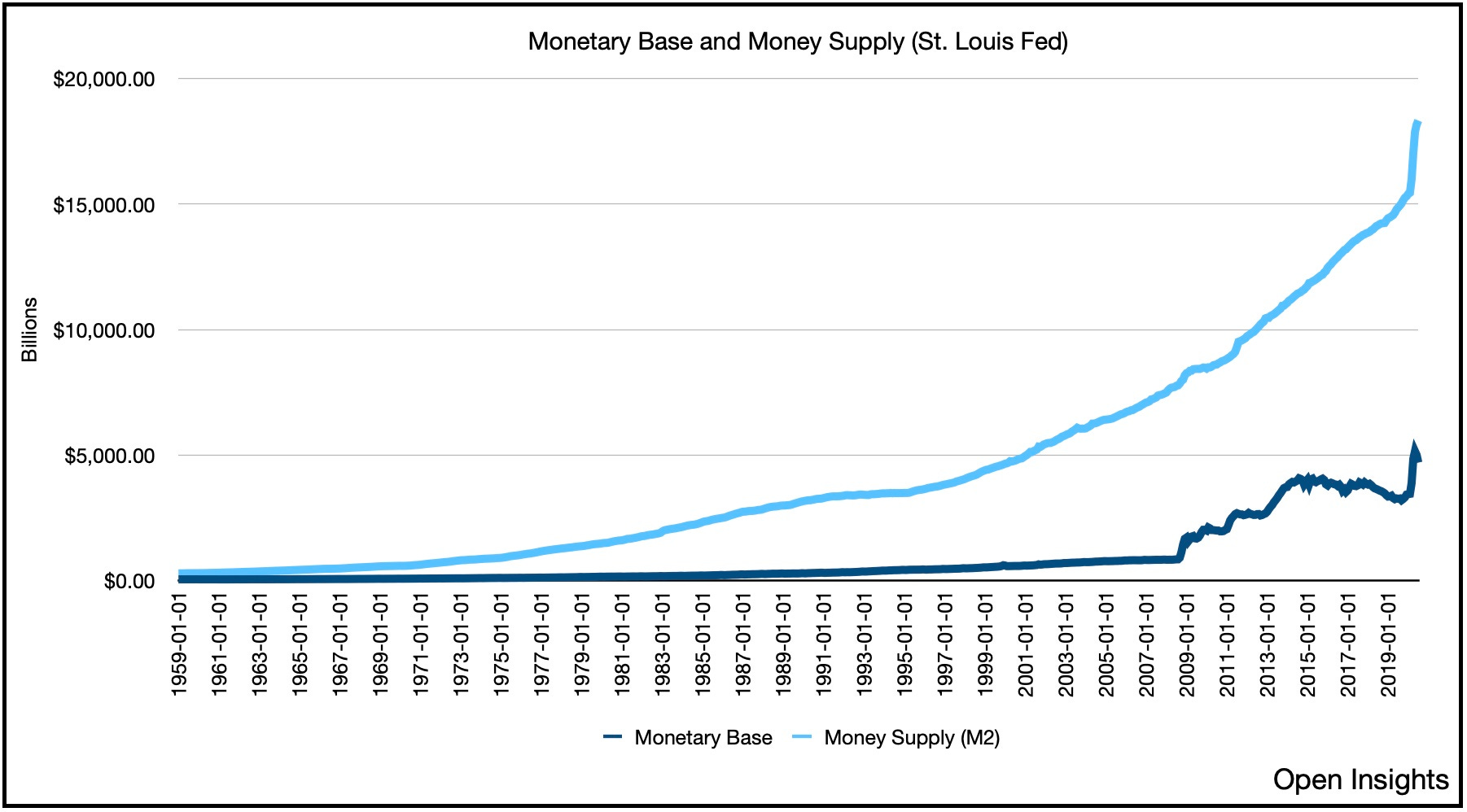

The second factor is the expansion of money and credit. That’s the juice. The fuel that allows the “investments” to fly. Now it can be either money and/or credit, but usually the credit piece is the larger component as credit dominates the marketplace. So increase the money base, money supply and relax lending requirements.

Engage in quantitative easing, which substitutes long term bonds for short-term ones and then quash short-term interest rates to zero by adopting a zero interest rate policy (“ZIRP”). So credit becomes not only ubiquitous, but cheap.

In turn, watch lending/borrowing fly as debtors refinance, issue new bonds, and increase margins. The more the merrier because credit is what divorces us from the real. It’s like buying with a credit card vs. cash. One feels more real than the other. Since credit works on faith (confirmed of course by your past history (i.e., FICO/credit)), the expansion of credit means more faith, a double-down in the belief, no, mutual trust, that asset prices can and will go higher, so it’s okay that we’re lending more since the assets you’re buying will be worth more. In turn, our security interest is also worth more. It’s a never-ending flywheel. Once divorced from reality and reliant on faith, the game is on.

#3 - The Safety Net

Now, we certainly can’t fly higher if we don’t have a safety net right? That’s the central banker, the Chairman himself. As this balloon lifts higher, don’t fight the Fed becomes fly with the Fed. It’s the third factor. The Chairman becomes our Catcher in the Rye as we start to believe that he’ll bail us out if our planned foray turns out to be Icarus-like. Why wouldn’t we think that?

When LTCM collapsed in ’94, the Fed banded together a group of financial institutions that recapitalized the firm to provide stability; an intervention for sure, but one thinly disguised so that the Fed could at least appear to be at an arm’s-length regulator in our “free market.” We’ve since dropped all pretenses as the GFC led to all manner of financial intervention and bond buying, and as of late the Fed’s now buying investment grade and junk bonds (albeit via special purpose vehicles). Let’s be honest though, does anyone doubt that the Fed wouldn’t directly buy stocks if investors climb the risk ladder and pile into equities in this ZIRP-ey world? The safety net in our minds gets elevated as we rise higher. So yet again, check this category as well.

#4 - The Charlatans

The last factor? The con artists, the charlatans. All bubbles need the hucksters, the people who promise the masses an opportunity to obtain easy riches with little to no effort. In a frothy uncertain market, they lead the charge. We’ve written before that

“[u]ncertainty creates a void that demands filling, and it’s usually filled by the loudest and most confident (if not competent) of voices. Spouted by charlatans masquerading as saviors, the methods are the same . . . exploit your fears for their benefit. Their chatter is internalized by a rapt audience, willing to suspend and eventually supplant their own independent thinking for just a momentary respite from the uncertainty. Inevitably the salve proves costly because it steals your common sense so they can take your common cents.”

The incantations have always been the same, only the medium different. Yesteryear it was CNBC, today they’re on Instagram, Twitter and YouTube, hyping stocks and investment strategies to the struggling retail crowd. The 20 year old cliche “bro” investors who mix entertainment and analysis. The fact that their strategies work today likely has more to do with the market’s momentum than anything fundamental, but when you’re making money it’s a moot point. More importantly, it’s an easy sell when people are uncertain and desperate for income. Those experts have started to gain traction.

Who’s more pernicious though? The “experts.” Us. Those in the money management business. Those who want the bubble to keep inflating because as Chuck Prince, the ex-CEO of Citibank famously (or infamously) once quipped “[a]s long as the music is playing, you’ve got to get up and dance . . . we’re still dancing.” That comment was made in 2007 right before the 2008/2009 Great Financial Crisis. We, and by that I mean your supposedly sane, rational, and fundamentally based fund manager will pour gasoline on this bonfire.

We may name ourselves after calming colors and soothing natural landscapes, but what lies beneath all the Willow Creek, Falling Leaf, Grey Rock funds of the world isn’t tranquility, it’s capital. Capital controlled by people who will feel increasingly threatened by career risk when they lag their benchmarks for too long.

Those are just the fund managers. We’ve yet to discuss the institutional investors who manage pension funds, endowments, etc. In a ZIRP world, where government bonds are near zero and the real returns on corporate bonds are close to that, the reality is there is no alternative (TINA). TINA is real because for an entire asset class (i.e., bonds), there are little returns. Oh you have a 7% investment return target at CalPERS? The honey badger doesn’t care nor does the market. To paraphrase Howard Marks . . . you can’t eat relative returns. You need real returns, to pay out and support the millions of retirees, students, non-profits and dependents relying on you for dollars.

It’s this group that has yet to “jump in,” because when they do, they’ll bring a wave of capital. In March and April of this year, money market funds garnered over $1.1T of inflows (ICI) as the virus peaked in the US. Since then only about a quarter of the inflows have come out, which means that as the market has rallied, guess who’s been lagging and now sits on a large pile of cash? Institution investors.

So we will look past 2020 . . . we have to. COVID has ravaged not only our health, but the health of our economy. US GDP is projected to fall by 5% this year, EPS for the entire S&P 500 will likely be 25% lower than what Wall Street had forecasted at the beginning of the year. Despite all of that, the market is positive for the year. Translation: don’t fight the Fed and look towards 2021. As we approach 2021, our narrative will then shift from a wounded economy to a recovering one as the development and dissemination of multiple vaccines and treatments progress.

If so and we Nike Swoosh this economy (not even a “V”) to add 6% to our GDP, but couple it with ZIRP/QE and fiscal stimulus, will today’s 3,427 S&P 500 level seem so absurd if EPS achieves $170 next year? We don’t think so, nor do we think people will. That’s a 20x multiple, or a 5% earnings yield in a ZIRP-ey world. 10 year Treasuries that now yield 0.7%? 145x multiple. If you think that’s a bargain have at it, but in a ZIRP world, we expect equity risk premiums to fall as prices rise.

Is the market frothy in certain sectors (e.g., segments of tech/green energy)? Perhaps, but the rest or overall? Not at all, and especially not when measured against the current backdrop of an aggressive Fed, more fiscal stimulus from Congress, and the sheer amount of capital waiting on the sidelines from institutional investors. Moreover, from a valuations perspective, there is merit to the contention that COVID has forced us to reconsider the role of tech companies in the global economy going forward and revalue them to reflect their inherent competitive advantages. So no, this isn’t the final stages of the bubble many people think it is.

It’s not the retail investors who will float this bubble to the moon, it’s the “smart money” who will convince themselves that this market can/should rise higher. Before this is all over, we’ll have instances of “smart money” cheering for a 2020 version of AOL taking over Time Warner a la 1999 again. Do we have the ingredients for a bubble? Yes, but not yet the euphoria. Oh worry not though, that’s coming . . . and when it does, as that other famous Prince said . . . we’ll party like it’s 1999.

Join the Distribution List

So that concludes this letter. Well endeavor to send these out weekly, so if you would like to be added to our distribution list, please click on the subscribe button above. This is our start and it’s our invitation for you to join us and share your thoughts. Welcome to Open Insights and let the conversation begin.