Today is Independence Day, Tomorrow is Something Else Entirely

July 3, 2026

Happy July 4th everyone.

May you celebrate safely and happily with all your friends and family. Except for the oil bulls. No oil bulls must suffer with the shame and ignominy of being . . . well energy bulls.

No fireworks for you since oil’s continued its slide as the Strait of Hormuz “normalizes.”

Given the bevy of information, and the holiday season this weekend, we know you’ve little patience and time to wade through it all. So to shortcut that process . . . let’s proceed under the guise that each picture is worth a thousand words. Here’s a few important pictures for you.

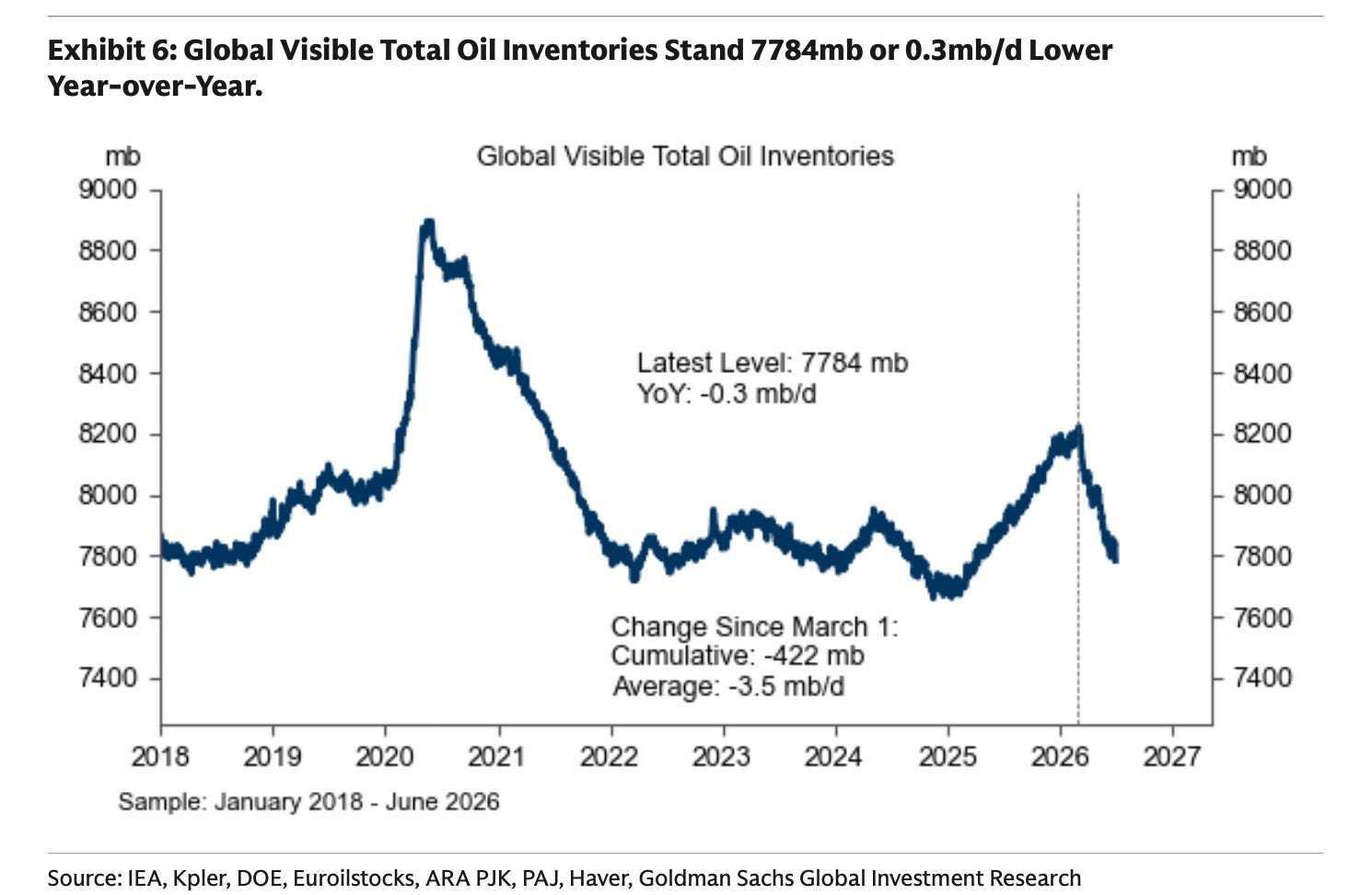

As the SoH normalizes, this is what visible inventories look like. Remember visible is only a partial snapshot of what we can obviously see, and so you’re missing tertiary and secondary reserves out there which is about 40% of the “stuff” out there.

Not much eh? Give or take 400M barrels have flowed out of the world’s coffers, which pales in comparison to what we’d expect given the nearly 10-12M bpd production outage over the past 100 days. You’d expect to see about 1.2B barrels lost, but that hasn’t been the case as seasonality (i.e., builds tend to occur during the lower demand winter/spring season), prior oversupply (we were oversupplied prior to the war), and China’s ability to dramatically reduce imports and dip into product stocks (which aren’t visible), have greatly mitigated the draws we can see today.

Fair enough, but if we were to “add-back” and factor in the various items above, our “gut feel,” sorry “estimate” is that we still ended up drawing somewhere around 700-800M barrels effectively.

Now the market obviously doesn’t believe that. Oil prices have cratered in the past few weeks and round-tripped the entire war based on the assessment that draws weren’t that severe, the SoH has normalized, and that some demand destruction has to be permanently baked into models going forward. We highly doubt any of that, but then again, we’re the bag holders for the time being.

Invert all of that, and you then must come to the conclusion that the world has been overproducing 10% of its entire energy supplies for far too long. We easily kept storage levels too high, production too flush, and wastefully tied-up working capital. That would seem a bit counterintuitive in a commodity space governed by razor-thin margins and little price stability. Over time, and we write that with a pound of salt, people are rational. Sectors, businesses and yes, even people, are rational. They don’t deploy and tie-up capital just to do so. We clearly didn’t “overproduce” 10% (i.e., 10-12M bpd of oil) of something that we didn’t need. In fact, just the opposite, we thirsted for it, and the truth is, despite how vague, opaque, and unclear the oil data is, we can assuredly say, we drew.

We drew heavily, we drew intensely, and we drew recklessly.

Yet, the price is right though isn’t it? That view is always determined by the lens you view it. Short, medium, or long-term. Here’s a great article describing that view, and it’s one we’d agree with. In the short-run, it may be right. Restoring some semblance of flows from the SoH means stuck traffic in the strait immediately escapes. It’s a prison break, and 60 day prison breaks are by nature unruly.

The exit is fast and furious. We’re suddenly draining the Persian Gulf of stored oil tankers, as as crews and boats trapped for 3 months make a run for freedom. Can you blame them? Sure, one or two will get plunked and damaged by Iranian tantrums, but for the most part, the ships and their cargos are freed.

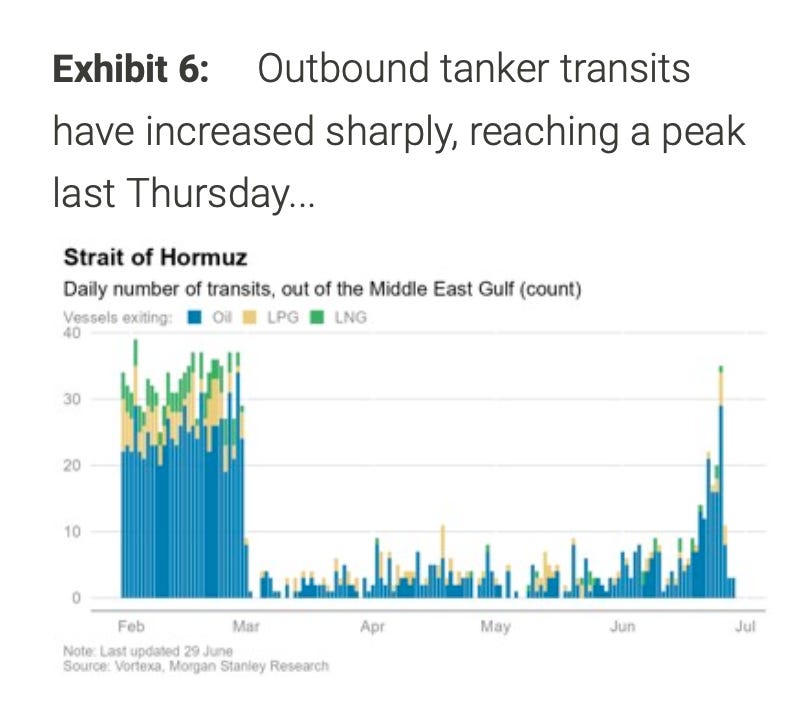

Outbound tankers surged . . .

Inventories drained . . . as did oil prices . . .

You dump that much crude that quickly, and you can saturate the market. It’s inventory transfer though. Shifting barrels from the East pocket (i.e., the Persian Gulf) to the West pocket (outside of the Persian Gulf). Still they’re barrels that’re available for global consumption.

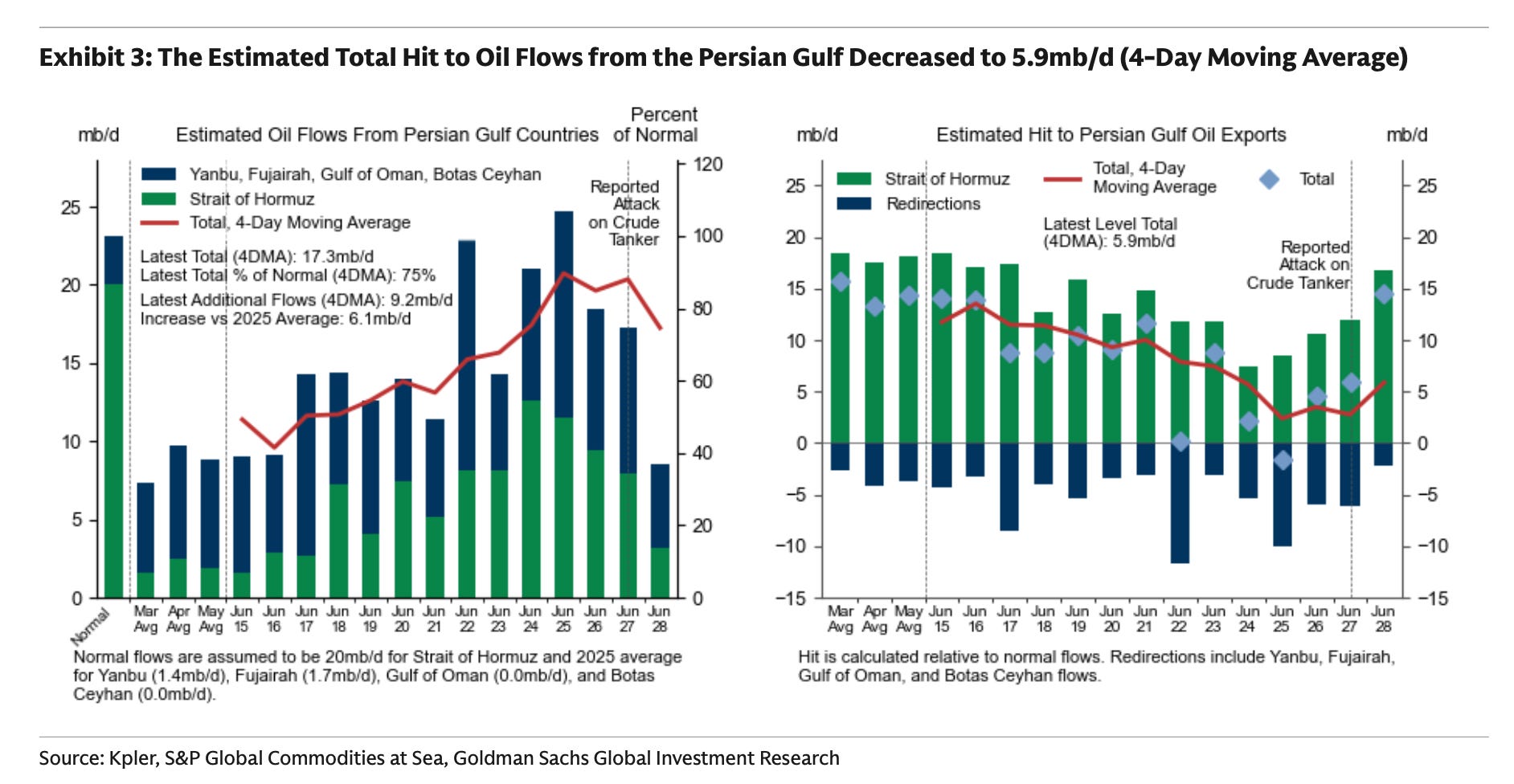

Given the rerouted oil since the war started, the SoH traffic really only needs to go back to around ~70% of pre-war levels. The rest of the oil will likely keep transiting out via the pipelines the Saudis and UAE used during the war (Yanbu and Fujairah).

For now, we’re close, averaging about 50%, throw into it the rerouted pipeline oil, exports out of the Persian Gulf are near 75%, so down about ~5-6M bpd. Considering the turmoil that’s not bad, but the key question is if it’s temporary. Much of that is tankers making the jail break, so that piece will subside.

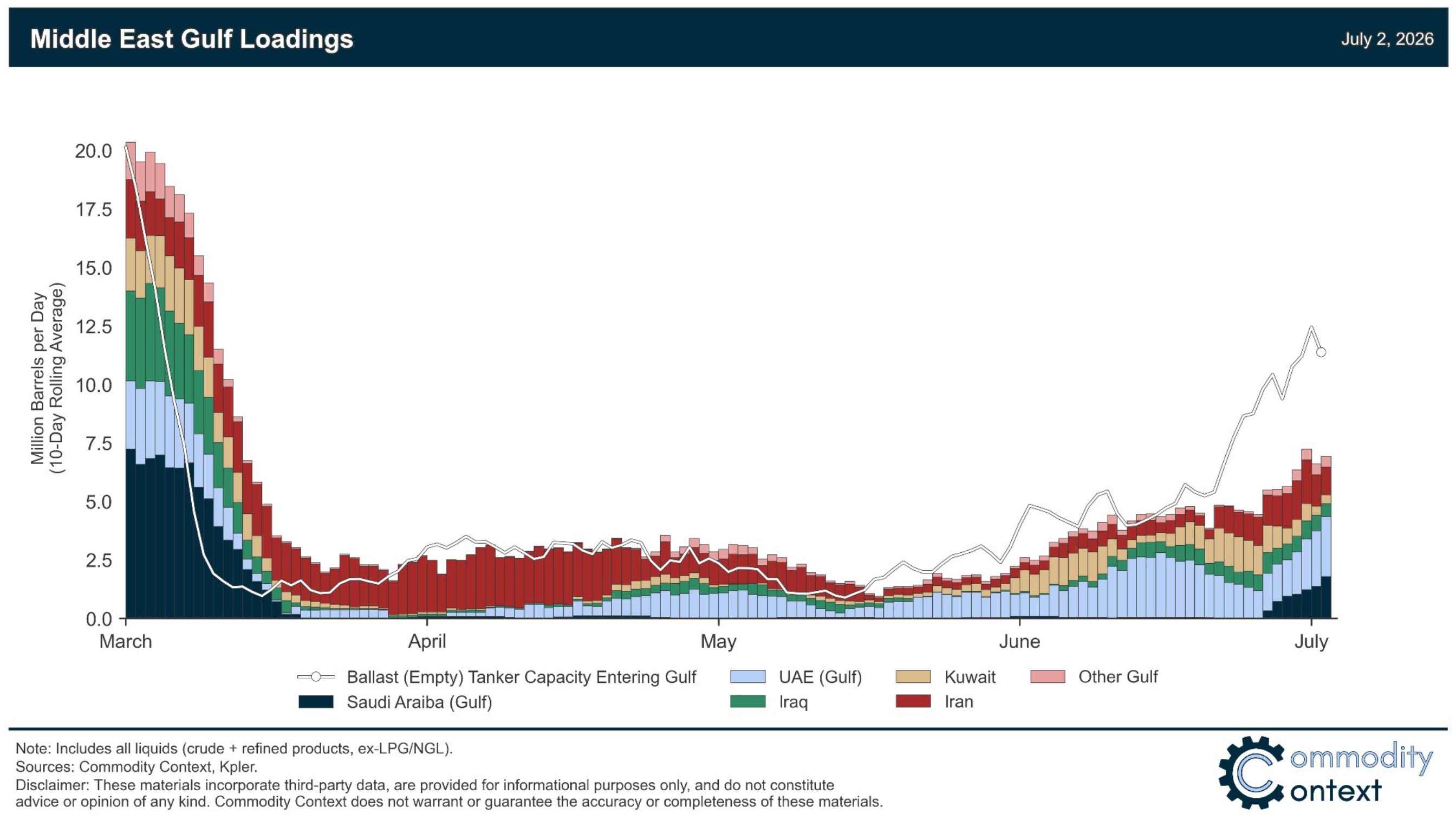

What matters is tankers moving in, draining stocks and allowing production to restart. That’s a bit up in the air as only about half of what’s needed (i.e., the amount of ships, are entering the Persian Gulf). Here’s Rory Johnston’s graph of that.

You see? A long way from normal . . . even if “normalizing.”

So basically, even if you can drain onshore inventories, and everything runs efficiently, you can only restart half the production at the current pace. We’re effectively still short about 5M bpd of production if all those tankers end up loading.

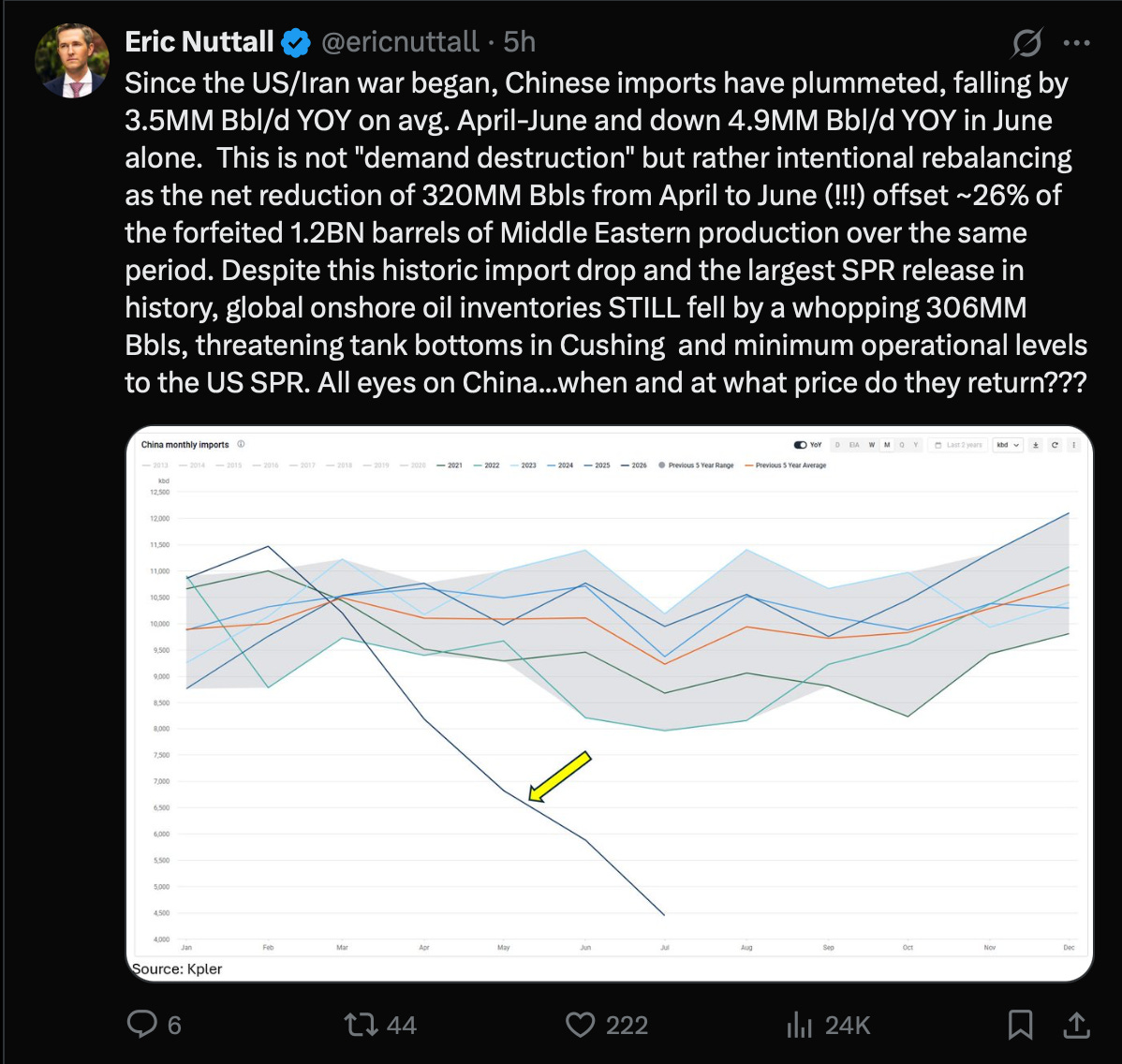

For right now though, the prison break and resulting sugar rush is enough to overstuff the market largely because the Chinese continue to flex their muscles.

By controlling product prices and limiting product exports, China’s slammed their domestic refineries. Low to negative margins means refiners stopped importing crude and curtailed refining operations. Many to minimum levels. This likely means Chinese product stocks have drawn sharply, but given that information is opaque, the market is left guessing, and discounting any draws there. This is a main reason why there’s such a disconnect in the inventory balances we see vs. the market narrative. As China has throttled crude demand by nearly 4M bpd for 100 days, that’s 400M barrels of demand decline, which really bolsters global balances. It continues to this day, and mitigates the impact of the closure.

What’s unlikely though is that China’s product stock didn’t decline. There probably was some demand destruction, but odds are product stocks fell materially. 1 for 1? Unlikely, but half? Yes, at least. China’s refining capacity runs about 14.5M bpd (EIA), and overall refinery utilization rates has dropped from almost 75% this time of year to ~65% in May. 10% is nearly 1.5M bpd, and June is most likely lower. Even state owned refineries shared in the cuts, though the independent teapots took the brunt of it.

Overall, it appears that nearly 1.5-2M bpd of utilization is offline. China exports about 400K bpd of products, and since those were stopped, and rerouted to domestic supplies, we’re probably seeing a 1-1.5M bpd decline in product inventories, along with some domestic demand destruction (though that should be minimal given product prices were capped). So 4M bpd of crude demand, assuming 1M bpd was originally used to fill SPR coffers and “extraneous,” you’re looking at 3M bpd of crude demand curtailed, and half of it results in crude draws and the other half product draws.

Quite impressive really, but when will China return to the crude buffet? Will it be soon? We’re not sure, but we don’t think so before the 60 day MOU wraps-up. China knows everyone’s waiting for them, but if they step back into the market now, they likely spike prices fairly quickly. Sure there’s some Iranian and sanctioned barrels currently to be had, but that’s temporary. They’re better off by burning some inventory, artificially suppressing prices for a bit, and letting the West suffer with higher produce prices. Stay patient and wait to see what happens to the negotiations. If they go poorly, and war resumes, China can then tap into its crude reserves, which thus far has stayed in decent shape. If, however, it goes well, then prices at these levels may just last longer. There’s no reason to rush, and to spike oil prices in the interim will only incentivize the Iranians to hold out longer. We believe China will seek stability in energy costs, and prioritize trying to achieve that in the longer run. So they wait.

Which means in the meantime, we’ll see product stocks keep dwindling everywhere. It’s what we burn. We’ll see higher product crack spreads, and refiners making exorbitant cash flows. We’ll also see crude inventories keep falling. Though the SoH has returned to half its original capacity, whether that stays at that level is questionable at best, and even if it does . . . it’s still not enough.

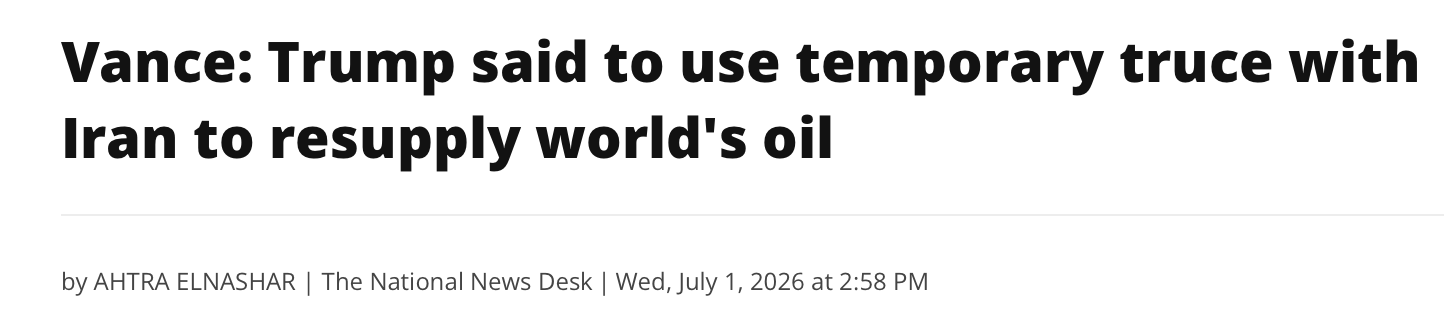

This is no longer an outage of epic proportions, it’s merely a run-of-the-mill outage of historic proportions. Don’t believe us? Listen to the administration, the very people who have actively suppressed oil prices. They’re starting to say the quiet things out loud.

““I think what the president has told us to do is use this MOU to sort of refill the world’s oil economy, to refill some stocks and then to see where the hand is," Vance said.”

Still we have a temporary reprieve. For now.

As barrels flow out of the Persian Gulf, and trade flows start to normalize a bit, this is a sugar rush. A deluge of crude because of the prison break, and China’s flexing of inventories. None of that can last though, product prices (i.e., as tracked via crack spreads) continue to notch new highs. There’s a shortage, and it’s being expressed on the product side. Inventories continue to be drawn, and though it doesn’t feel like it, it remains, and it will come back to haunt us if the MOU fails to lead to a comprehensive and lasting agreement.

Ultimately, we think it will. We think the administration is hell-bent on buying Iran’s acquiescence, and so what were third rails, or red lines will be swept away or erased. Nothing’s off the table when the alternative is war and “bedlam.” Bedlam is never good for stock prices and political survival. Having said that, the oil market is still sorely mispriced. When you destroy price discovery, there’s nothing to incentivize energy producers to commit capital and begin the restocking process. Therefore, from an inventory perspective, we continue to fall. Sure at a slower pace given the return of partial oil flow in the SoH, but don’t let the price fool you. It’s temporary, it’s a sugar rush, and it will eventually hurt. Just not today.

Today is Independence Day!

Tomorrow is something else entirely.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.