Trapped in a Vortex of $#!T

April 1, 2022

In the midst of writing our weekly missive and our fund’s quarterly letter, we were hoping that the last few days of March would prove to be quiet and calm, or at least not fraught with so much volatility as to induce any handwringing (or rewriting!). Unfortunately, that’s not meant to be.

So in stepped the White House on Wednesday night, when headlines after the market closed blared that the President is set to announce a 180M barrel release of oil from the US’ Strategic Petroleum Reserve (“SPR”). This of course follows the IEA’s own coordinated release in early March immediately after the onset of the Ukraine invasion, and an earlier US release in November of last year.

180M barrels though, that ain’t a small figure. Purportedly at a rate of 1M bpd for 6 months. The figures somewhat of a mirage though. The reality is that the SPR has never drawn down at that rate. At its peak, the SPR has drawn about 4M barrels per week, so nearly half of the 7M bpd reported and that’s during emergencies. Pipeline size, pressure, crude viscosity, midstream operators or customers’ ability to take the crude, etc. all play a role, and when taken together, 1M bpd seems a stretch.

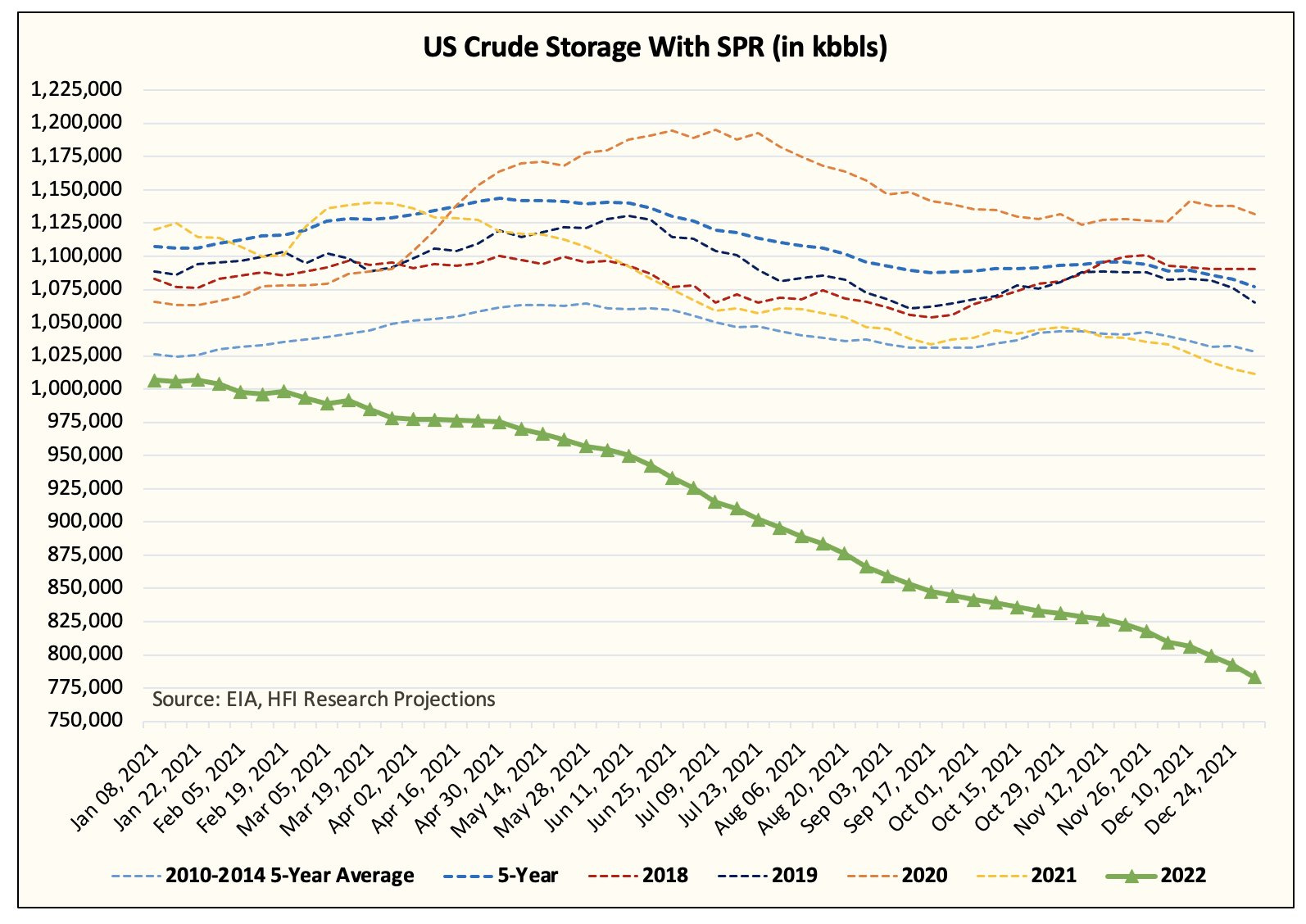

Okay so a slower rate of withdrawal right? Likely, but let’s assume it’s full bore and for 180M. By the end of the sale, we’ll see US crude inventories look something like this:

That my friends is an assured path to +$150/barrel oil in 2023. What’s stunning about it is that the US then plans to repurchase the oil to replenish the SPR at a later.

This restocking will increase demand for oil at the later date. Given oil prices are currently steeply backwardated (i.e., oil for delivery in the near term is priced much higher than oil to be delivered in the future), the White House is effectively conducting its own “Operation Twist” for oil.

If you recall, after the Great Financial Crisis the Federal Reserve attempted to lower long-term interest rates (to stimulate the economy), and thus sold near-term bonds to purchase long-term ones. In effect “flattening” the curve. They’re essentially rerunning the playbook here and lowering the current economic pain of oil prices today, but lifting oil prices in the future to incentivize producers to increase production.

Oil producers like to see a higher futures price before committing to drilling more because it takes time to ramp up, and it’s nice to know that there’s some certainty the additional capital committed will be worth it. For at least a day after the announcement it seems to be working. The front of the curve became less backwardated, as front fell and back rose . . . well slightly.

Yet, we doubt this will really bring about a deluge of production. This is a structural shortage, years in the making. Producers are on a firm trajectory to repay debt and return capital to long-suffering shareholders who’ve survived years of low oil prices. Management teams are also no longer incentivized to grow production since their compensation structures have deemphasized material growth. If either of those reasons weren’t enough, throw in service and material cost inflation, labor shortages, oil price volatility, fewer Tier 1 drilling locations and general conservatism after two near bankruptcies (i.e., during the oil price crash of 2015 and COVID), and we know there’s little appetite to materially increase production despite the government’s efforts.

Hence, it leaves us with this dirty truth . . .

There’s very little our politicians can do to alleviate the pain of higher oil prices. More pointedly, politicians, regardless of party, are likely the most ill-equipped and least incentivized group to deal with an inflationary environment caused in part by structural shortages.

“Show me the incentive and I will show you the outcome.” - Charlie Munger

Their first instincts are political. How do we keep our constituents happy? How do we lower oil prices so we can get reelected? Dealing with a structural shortage requires us to curtail demand, a definite strike to constituent happiness. Conversely, drilling more alienates certain voter groups that support you. The Democrats currently in power are backed by constituents who place a high priority on fighting climate change, so rescinding regulations to allow for more drilling would be anathema.

Thus, almost every politician that’s in a democratically elected system will end up subsidizing their electorate. Not just in the US, but everywhere. Politician will race to outprint each other. They will rain down money on their voters in the hopes of forestalling the impact of higher energy prices. While it hasn’t happened at the US federal level, it’s already happening worldwide. Just take a look.

The fascinating thing is that all of these subsidies will actually spur demand while doing nothing to increase supplies. We’ve little doubt that the federal government will eventually follow the same path if the SPR release fails to lower oil prices.

Arguably, President Biden’s “Operation Twist” is a good idea. It lowers oil prices today, but raises it later to spur production. We actually want that and contrary to handing out subsidies, it’s actually more conducive to helping oil companies bring new supplies online. However, will it work? No. While we believe the SPR release will temporarily restrain prices and elevate the backend, it’s not enough. 180M barrels over 6 months isn’t enough to combat a 2M bpd persistent shortage that’s going to increase as we head into the year end. It’s not enough to overcome the real world constraints faced by producers, and once the finite SPR drains, the structural shortage will reemerge to again ratchet prices higher.

We are dealing with repercussions now.

Remember the root cause of our energy shortage was the development of shale oil coinciding with the easy money available after the GFC. This unholy marriage led to capital destructive activities that oversupplied the market and sent prices reeling and many firms into bankruptcy. Years of right sizing finally allowed a few to survive, but they emerged with vastly different shareholder bases and expectations.

Overabundance also engendered apathy and the years of cheap commodity prices have led many to falsely believe that these raw materials were easy to obtain and even more dangerously, unnecessary. We’ve always said that the ESG movement was carried aloft on the back of cheap commodity prices and that it bred ignorance into how challenging these drilling activities/projects truly were. The lead time they take, and the manpower and capital they require, but people just didn’t care. We sloughed everything off to the developing world, to “emerging markets” replete with reserves and extracted by cheap labor. Countries with nonexistent or loosely enforced environmental standards, ruled by autocratic and psychopathic leaders. Out of sight, out of mind we said.

Why would we sully our hands before we open our pristine white boxes of Apple products? Never mind that manufacturing and transporting our electronic jewelry would’ve been impossible without commodities. Really, out of sight . . . out of our minds.

Years of underinvestment is now catching-up. Only now are we truly living through the repercussions. It’s a vortex of $#!t now.

We seldom curse. Little ones and a kindergarten teacher wife does that to a person, but seldom is a curse word more apropos than it is today. It’s a maelstrom where capital flight, ill-conceived green energy policies, climate change activism, short-sighted politicians, an ignorant electorate, psychopathic leaders in countries with abundant raw materials, and skittish investors all swirl and collide to create the unfolding crisis. One that will fuel levels of inflation so high as to throw the poorest countries into deeper pits of despairing poverty.

No this isn’t Trump’s fault, it’s not Biden, it’s not Obama, it’s not Bush. Take your political notions and proclivities to “blame the other guy” and throw them out the window. This is a collective failure of everyone. It’s frivolity and carelessness taken to the extreme by nearly unlimitless money printing that made us think everything and anything is possible. Sorry Virginia, not everyone can be President. Our dreams are constrained by the availability of raw materials, and for oil, at today’s prices . . . we are running out.

We’re in the last stages of our path to an energy crisis.

Wealthy nations with coddled electorates now demand action, but instead of spurring production and increasing supplies, we’ll offer half truths, a salve of subsidies, and our last remaining winter stores.

None of it will work. The weight of the structural shortage can’t be solved by money printing. We physically and collectively have to reengage this industry and commit capital, time and energy to produce the very things that power and shape our lives.

There is no other solution. Still we will procrastinate and delay that day for as long as our pockets and printers allow. We will outprint those less fortunate, outbid those less wealthy, and outfight those weaker than us for the very things we need. Just as we exported the dirty work involved in developing our resources, we’ll now export the misery of a global shortage.

We truly are . . . in a vortex of s . . . .

“We will not curse anymore.”

“We will not curse anymore.”

“We will not curse anymore . . . today.”

Please hit the “like” button below if you enjoyed reading the article, thank you.

You do the hokey pokey

And you turn yourself around

That’s what it’s all about!

Destiny is All !