Visible Oil Inventories Start to Draw

April 24, 2026

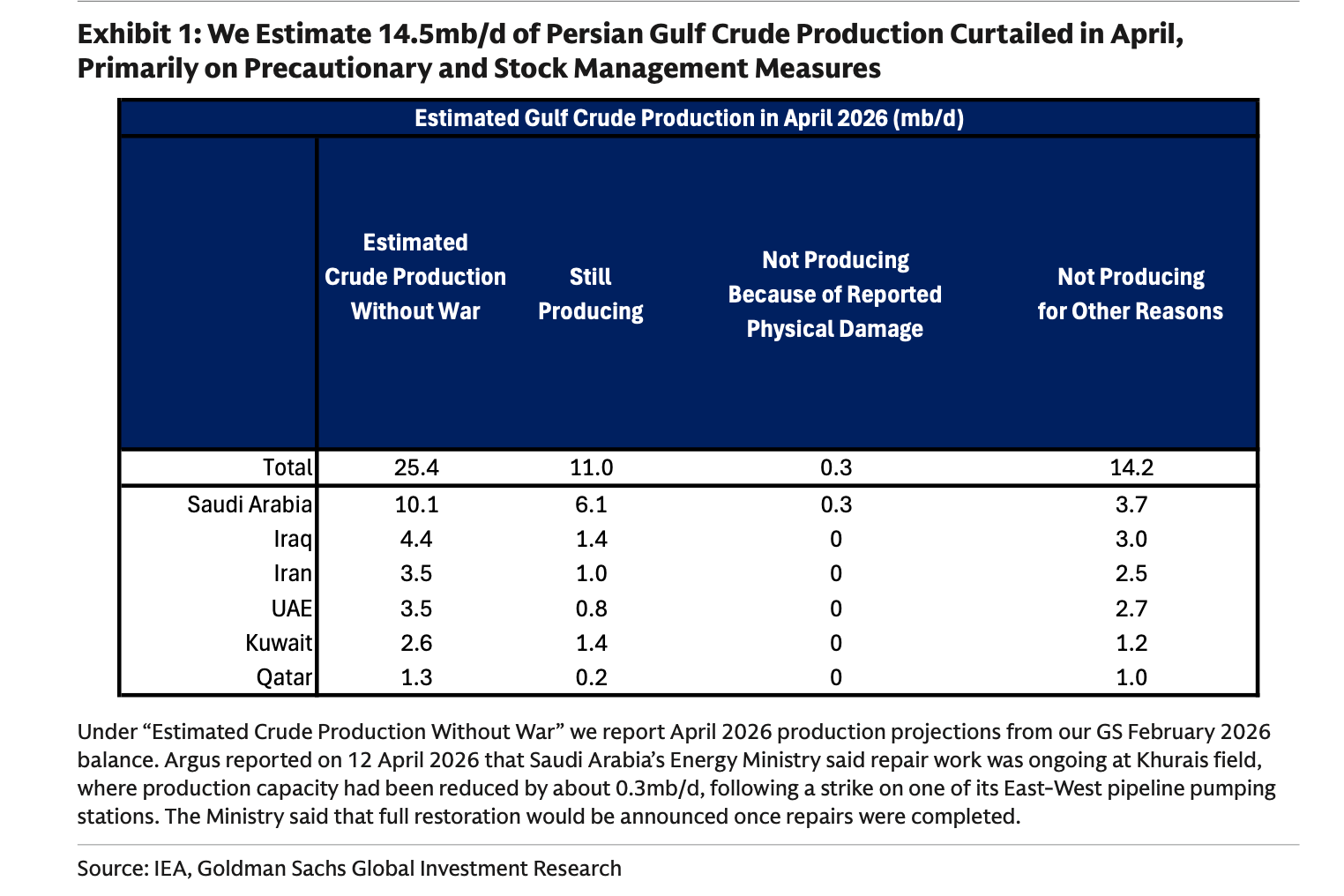

14.5M bpd.

That’s Goldman’s estimate of production shut-ins for the Middle East. We had pegged it around 11-12M bpd, so a smidge higher we suppose.

Our original assumption was that the US/Iran War would end on April 21, the day the ceasefire ended. We wrote that to be conservative, with diplomats winging their way back and forth to Islamabad, there was a chance some sort of agreement could come to fruition. Hence it was safer to assume that a miraculous agreement could be crafted to resolve the seemingly intractable issues between the US and Iran (i.e., the Strait of Hormuz (“SoH”) closure and Iran’s nuclear enrichment program).

The deadline passed uneventfully though. This week saw the ceasefire extended indefinitely and the resignation of Iran’s Head of Parliament Mohammad Bagher Ghalibaf from the negotiations team. News reports soon surfaced that Iran’s Supreme Leader Mojtaba Khamenei had reprimanded the Iranian negotiation team for the first round of discussions because they had placed the topic of nuclear enrichment on the table. Whatever the reason, the IRGC and the Ayatollah appear to be in firmer control, which should mean harder line positions prevail. So off we go, finishing up a 7th week of this campaign. We’ve likely lost ~700M barrels of oil as of April 21st, and now that it’s apparent negotiations may take more time, we’re in bonus time. Like soccer though, we’ve little clues how long the bonus time will last.

The US’ blockade of Iran’s blockade is an attempt to apply more economic pressure, but since Iran largely sells its oil to China, those vessels have been unmolested. There’s little reason for the US to anger the Chinese, especially as their own meeting is scheduled for early May. So if a majority of Iran’s oil continues to flow, we do wonder, when is a blockade not really a blockade?

A Day of Delay, Keeps Lower Prices Away

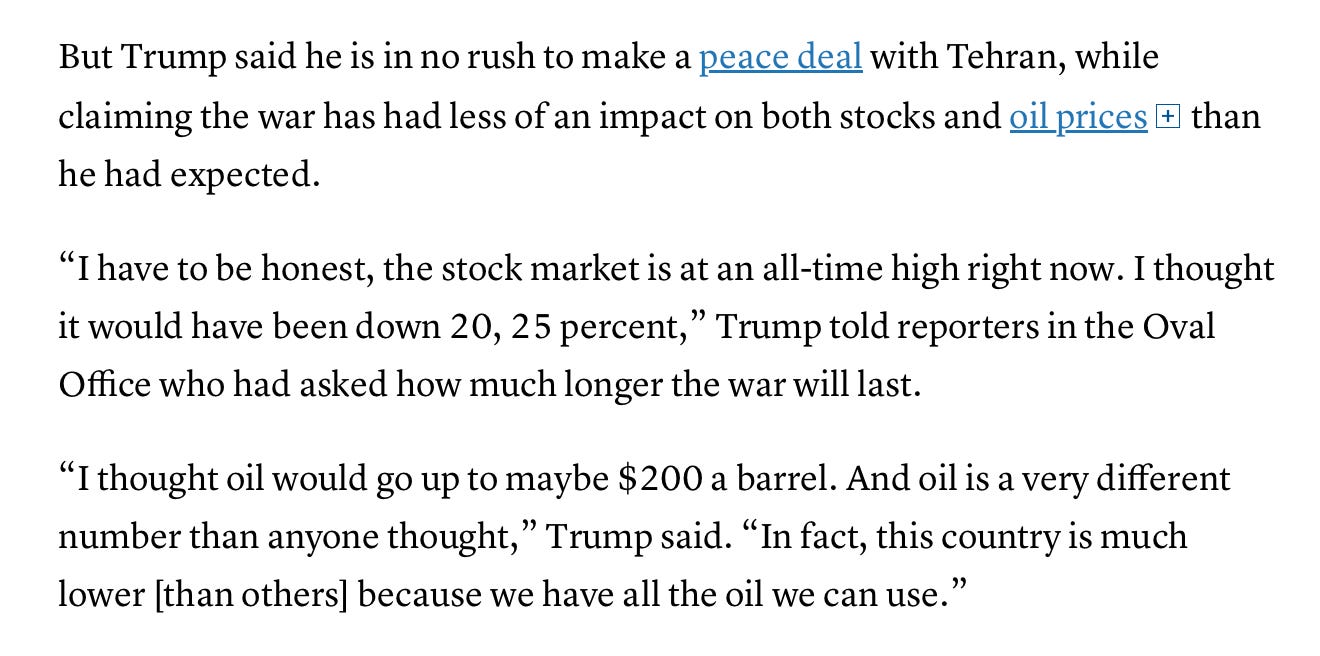

The question does remain though, how long do the combatants have to survive this? The US believes it has effectively as much time as it needs, and certainly more than Iran. The idea is that Iran’s storage will eventually hit tank tops and in a few weeks, they’ll be forced to shut down wells. In contrast, Iran sees the global economy and postulates that the higher oil prices go, and the lower the stock market moves, the weaker the US’ resolve in furthering this war. It’s obvious the US wants to TACO and that a ground offensive is unpalatable militarily, strategically, and politically. Despite the headwinds, the stock market has rallied massively in the past 19 days. Moreover, oil prices have remained below $100/barrel even as the physical market indicates tightness. In fact, the administration is actually quite pleased with the current state of events, as it gives them the perception of leverage in the ongoing negotiations. Whether it really does or not is questionable.

On Saturday, the US is sending Steve Witkoff and Jared Kushner to Islamabad to engage with the Iranians. Takes about 16 hours to get there, so figure they’ll start chatting Monday. What’s telling is that the US didn’t send Vice President JD Vance, who led the delegation last time. We think this speaks volumes, as there’s still a chasm between the two sides. Frankly, we’re not entirely sure they can bridge it, but the Iranians will be going as well, though the two are not meeting directly.

The US will certainly not give up control on the SoH to the Iranians, and accept a permanent tolling system. Granting such a concession would be viewed as a strategic loss and anger the Saudis/GCC coalition. It could also impact the sanctity of the petrodollar, as the GCC would view the US as unreliable allies.

Furthermore, the US is seeking an agreement that’s tougher than the JCPOA for nuclear enrichment, but can Iran actually swallow such a bitter pill? We don’t think so. We don’t think so because Iran actually thinks it’s winning militarily (note: they are). Not in the conventional sense, but from the strategic one. They still control the SoH even with a devastated air force and navy. Drones and mines are sufficient these days, and Iran has been effective in employing them.

The paper market and the stock market have been entirely dismissive of the supply outage. No thanks in part to the jawboning that’s created extreme volatility and higher margin requirements, which then dampen the risk appetite of traders. So oil languishes below $100/barrel, and it gives the generalists betting on technology, semiconductors, and AI, that all is well, and all will be well . . . because just look at the stock prices, we’re making money.

If so, then neither side has felt enough pain yet to force a compromise. Instead of malleability, we’re looking at recalcitrance and a prolonged period of negotiations.

So Monday it is . . . for the next round. April 27th. 6 days after April 21st. Multiply that by 14.5M bpd and we’ve just lost another ~87M barrels. For every week the SoH remains closed we’re looking at 100M barrels of crude never produced. That figure’s permanent, and it is real. Now the real drawdown in inventories will be less because of demand destruction (we think around 4M bpd) coupled with SPR drawdowns (3M bpd) will soften the impact, but SPR drawdowns are inventory reductions, just in a different pocket than commercial stocks. In the end, both pockets are on the same pants, and them pants sure be getting tighter.

In Totality

We’ve seen the tally anywhere between 700-900M bpd lost (not including the 200M bpd likely to be lost when the SoH starts to reopen because tankers are mispositioned and production restarts need to ramp). We’re also not factoring in any complications to restarting oil fields that have been laid dormant for a month, or refineries and infrastructure that need to be repaired.

This is fine.

This is fine right? No . . . fine is furthest from the truth. Asia’s cupboard is threadbare, and Europe is running dry. As US inventories drain in the coming weeks (because of the export demand as everyone pulls barrels away), prices will creep higher. Those that have not will buy from those who have, eventually pricing out the other have nots.

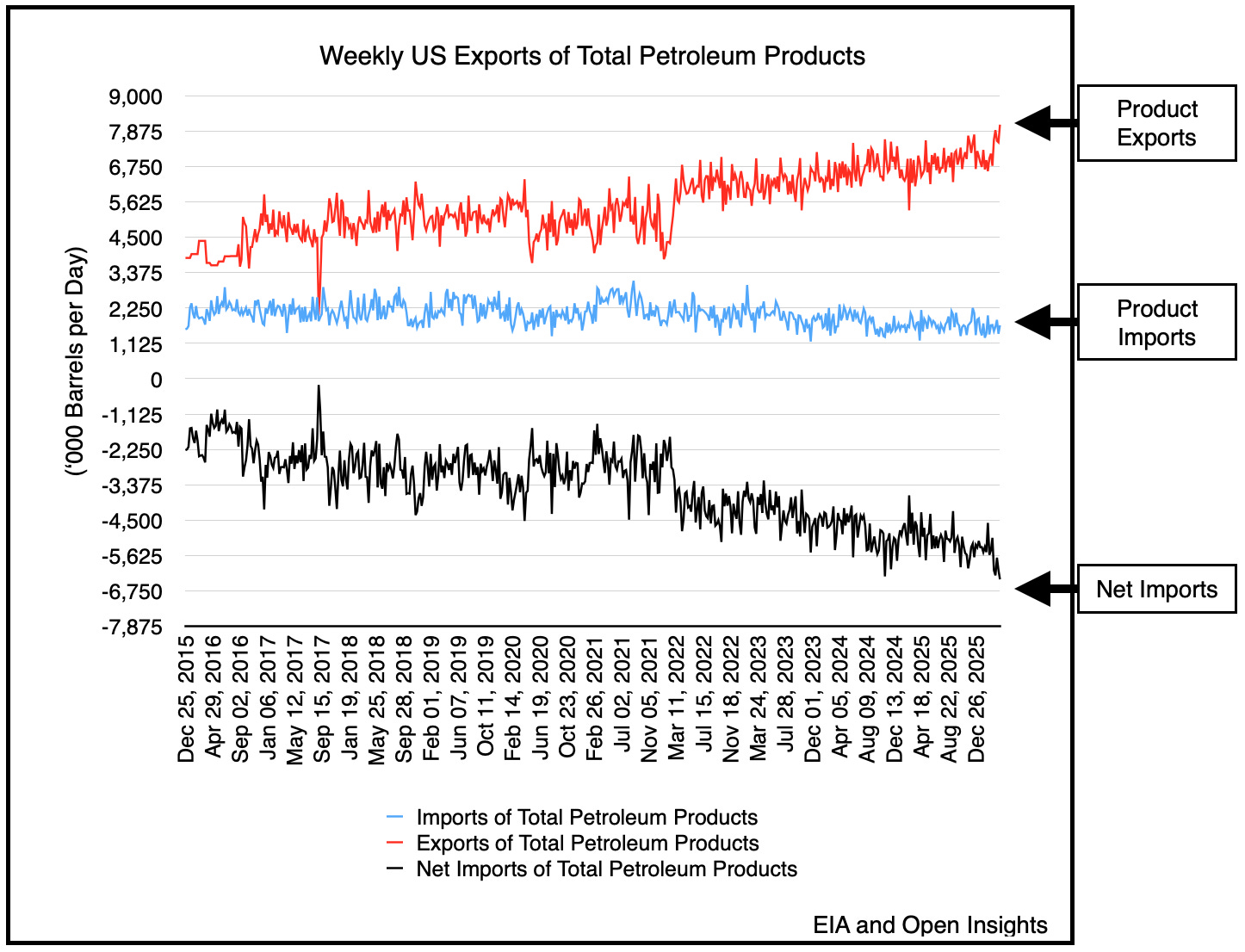

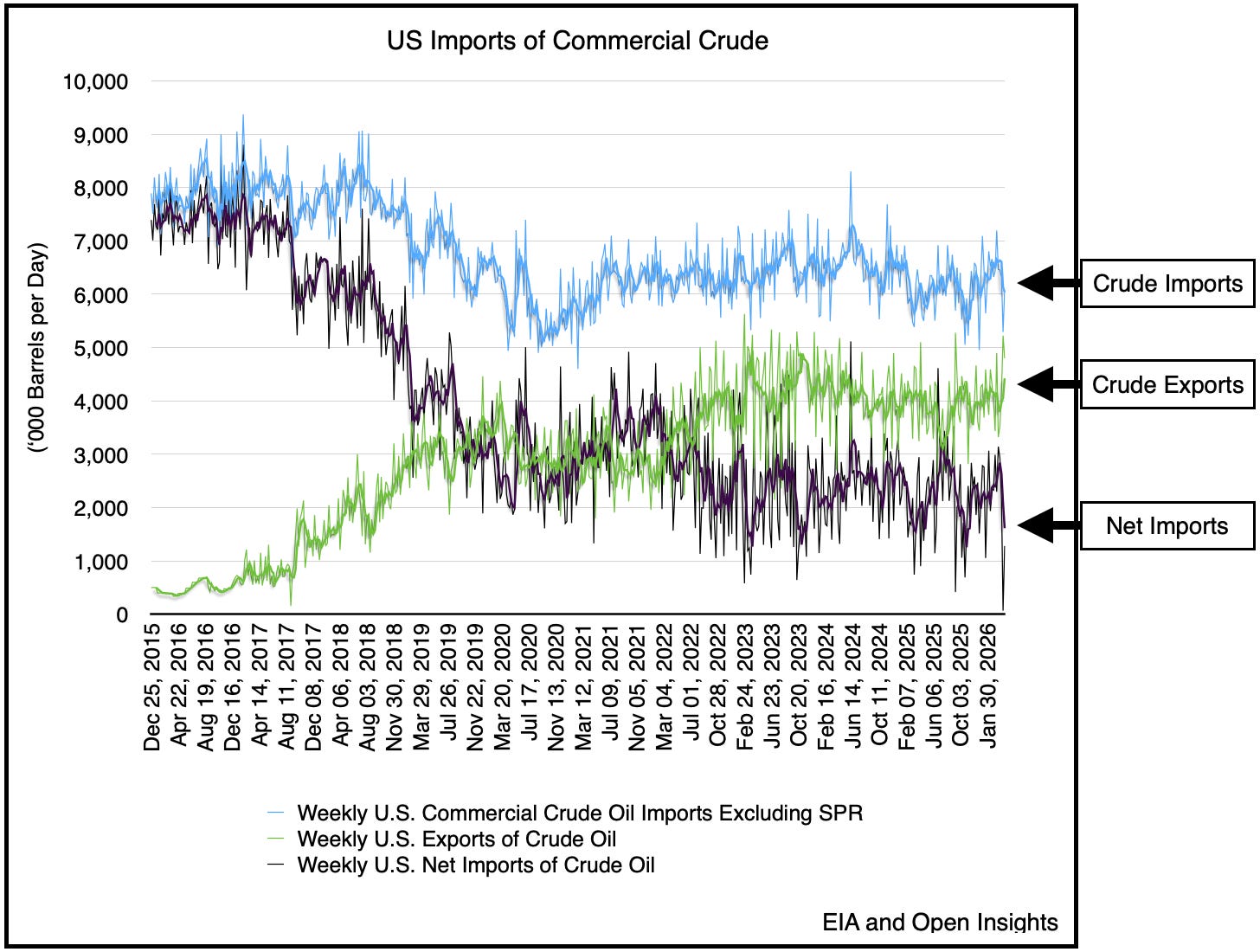

The US, the last location to drain given its distance from the Middle East has begun to see increasing draws. Product exports have recently hit an all time high.

Crude is following, as the weeklies have started moving.

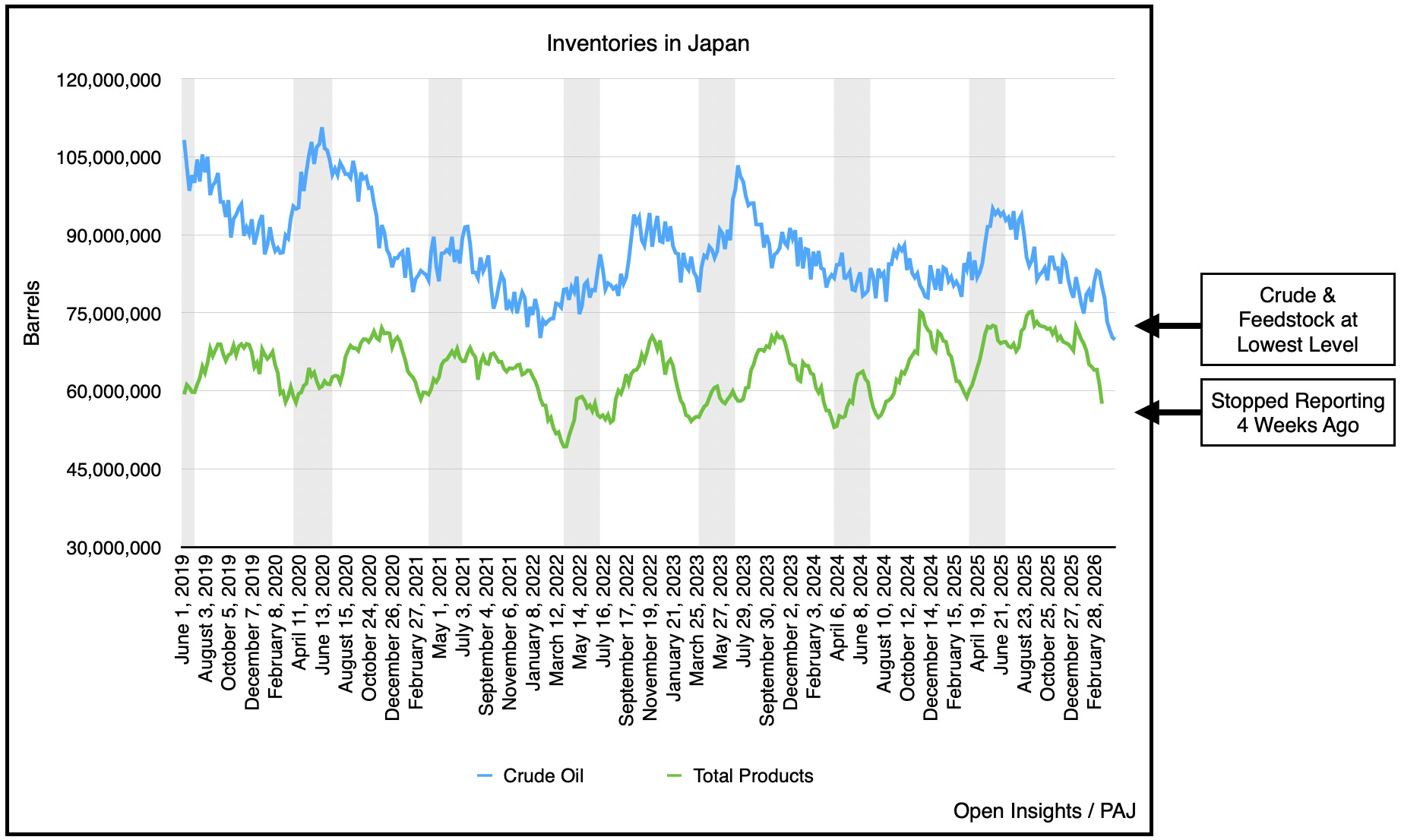

In totality, our contemporaneous OECD tracker is starting to show the divergence overall (US/Europe/Japan/Fujairah).

Remember the above includes Japan, and Japan has stopped reporting product changes, but we can guarantee it’s down by tens of millions.

Inevitably, unless massive demand destruction kicks in, our global choice is between losing a historic amount of inventories . . . or unfathomable amount.

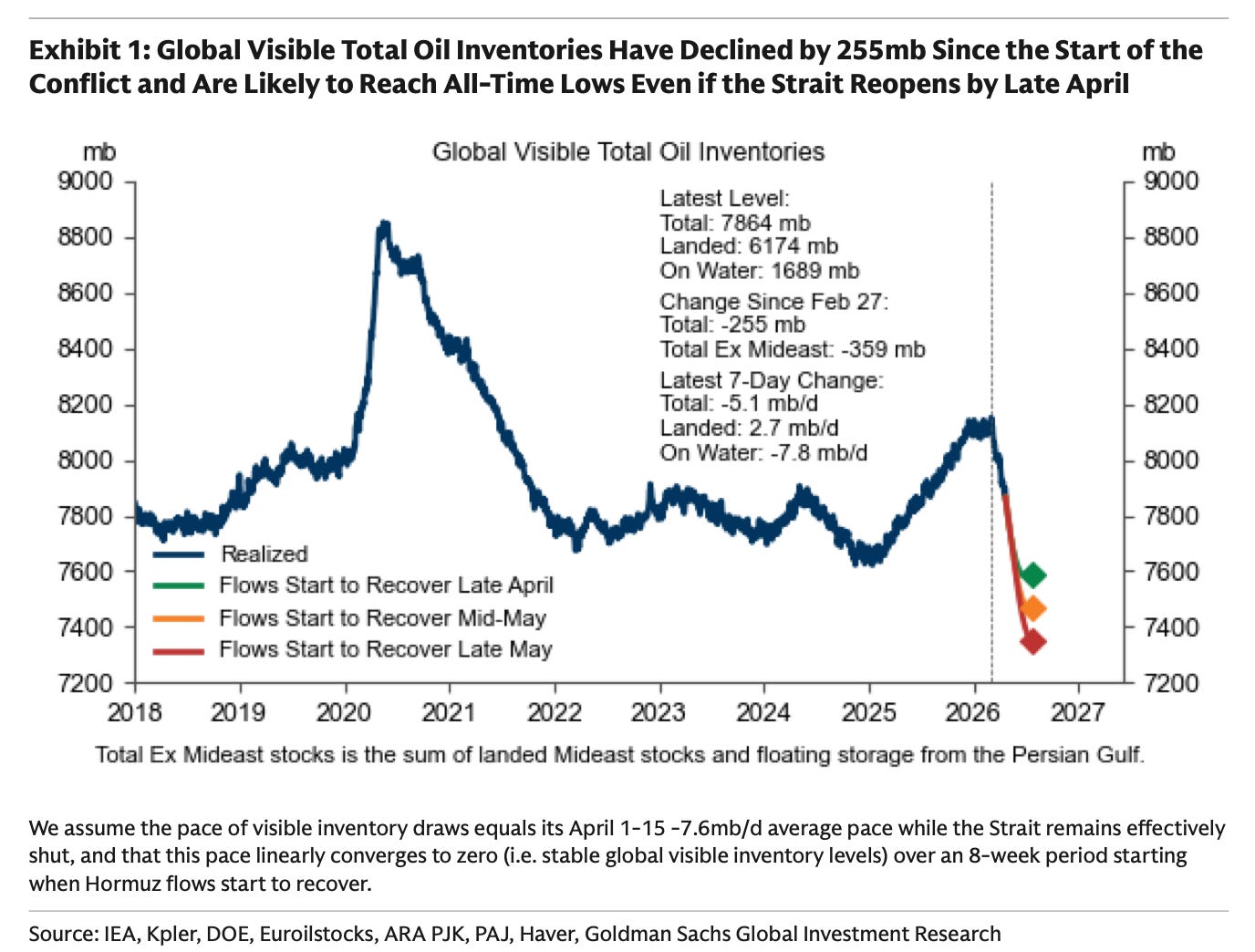

The first green dot is already set though. We’re in late April, so visible inventories will almost certainly fall to the indicated level. It’s shy of the 1B or more we think will be drawn from inventories because the above chart doesn’t fully capture the harder to see product stores. Again the safer assumption is 1B barrels lost as of now (inclusive of a 2 month ramp-up that sees the world lose 200M barrels), and every week thereafter another 100M barrels.

So at this juncture it’s really how much further do we bleed inventories down.

As the weeks play out and visible inventories start draining hard, we’ve little doubt that oil prices will recapture their highs on the front-end. Once the back-end of the curve starts to move, the E&P equities will also find a new floor. Contrary to commentators out there, we still think energy matters.

Molecules will rule over paper. While the paper market can hang on every Presidential tweet and distort what’s happening because volatility prevents market participants from seeking real price equilibrium, inevitably a stock-out will force the issue.

The haves will outbid the have nots, and you can take ours . . . for a rich price.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

I think the restart scenarios need to stop being just binary (is Hormuz ‘on’ or ‘off’). There’s a very realistic prospect that we restart partially for months with Iran restricting traffic to countries that don’t enforce US sanctions or transact in USD, for example.

"The haves will outbid the have nots, and you can take ours . . . for a rich price."

1. What's your take on Art Berman's view: https://x.com/aeberman12/status/2047369251111960963?s=20

2. Demand destruction could arrive sooner than the rich price, so the rich price may not materialize?