When the World Is Upside Down

March 18, 2021

I did my first Sirsasana yesterday. It’s a yoga handstand. One where your hands and your head are on the ground and your body’s straight in the air. Inspired by a Eva Longoria picture that my wife showed me last year (April 2020), I naively said “how hard can that be?”

A whole pandemic later, and I humbly submit this . . . Ms. Longria? She is one baaaad woman.

I bring this up not as my own version of a 26.2 bumper sticker. After all aren’t yoga poses the human equivalent of pet tricks? I bring it up because her picture was originally captioned with the words “[w]orld may be upside down, but so am I.” The picture was Instagrammed (or is it “Grammed”?) to her followers at the very beginning of the pandemic, so consider it a snapshot into her psyche at the time. Definitely not an unusual feeling as we all felt it. Top became bottom, bottom became top as a pandemic gripped the globe. Almost twelve months later now, we can maybe begin to exhale, and say the world is righting itself.

Turning Legislation on Its Head

While we may be seeing a recovery from the pandemic, we definitely saw a changing of the political landscape as Republicans “transitioned” power to the incoming Democratic majority and President Biden administration. Shortly thereafter, Democrats passed the $1.9T American Rescue Plan Act (“ARPA”). Signed by President Biden last week, the ARPA provides all manner of economic assistance, business loans, individual payments, state and local funding, education and health funding, etc. Most of the attention has been lavished on the Economic Incentive Payments (“EIP”) (i.e., stimulus checks), and those payments have started landing in bank accounts. Since the IRS directed the ACH payments to clear on March 17, we’ll begin to see an uptick in spending shortly.

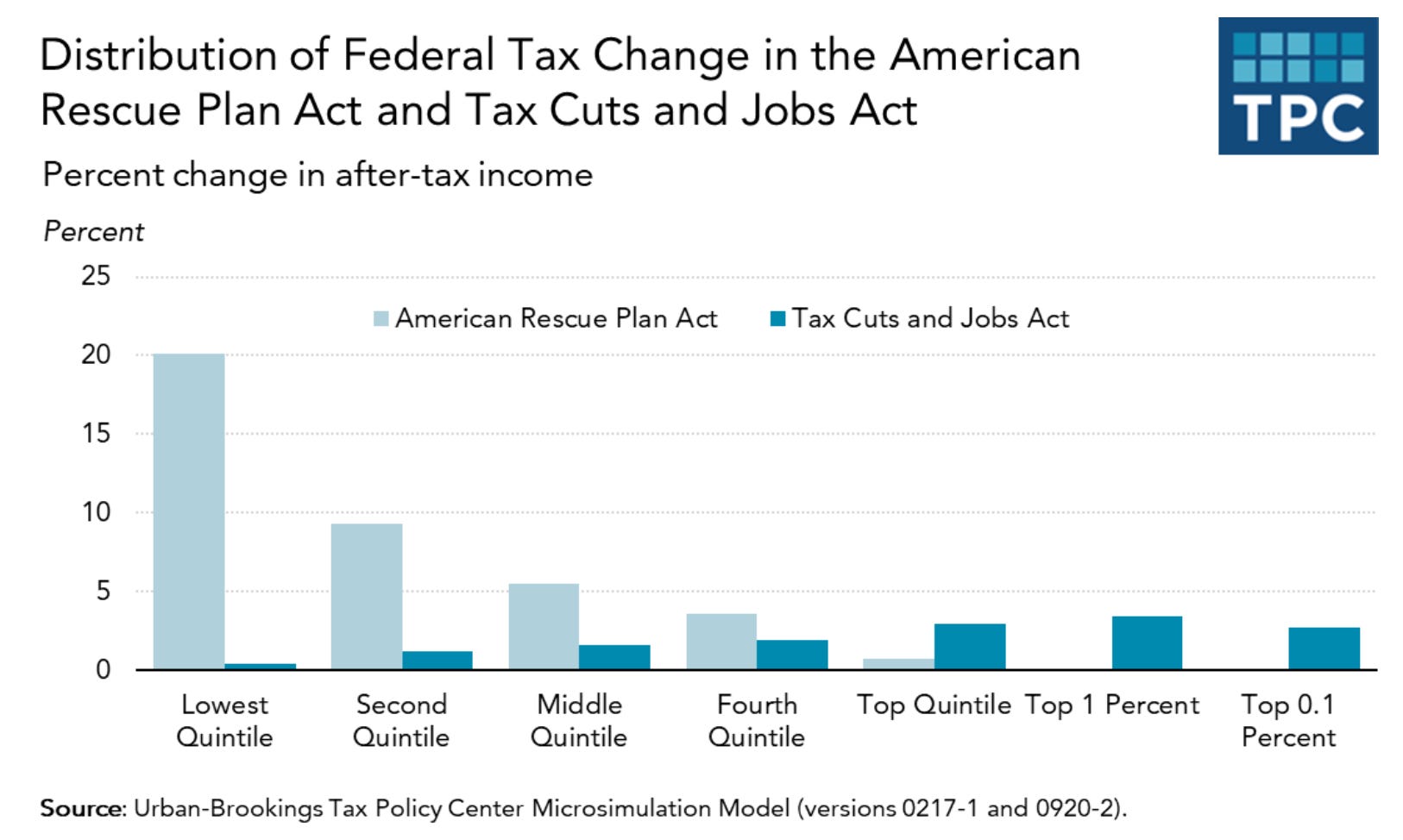

Sticking with the upside down theme though, our handstand made us think about this chart.

Beyond the EIP, what’s interesting to us about the ARPA is how it’s directed. Unlike the Tax Cuts and Jobs Act (“TCJA”) passed in 2017 (when Republicans were in control), the ARPA performed a Sirsasana of its own, distributing by far the largest portion of the benefits to the fourth, middle, second, and lowest quintile. In fact, the lowest 20% received almost twice as much as the next quintile, and collectively those in the bottom four quintiles received more than 95% of the benefits.

The payments will come in the form of direct EIPs, expanded Child Tax Credit (CTC), Earned Income Tax Credit (EITC) and Child and Dependent Care Tax Credit (CDCTC). While it’s debatable whether the bill was too large, too untargeted or too partisan, what we can definitely say is that if this pandemic affected anyone more than another, it would be those in the lower quintiles, and at the very least we are sending transfer payments to those who need it and those who will spend it.

Spendapalooza

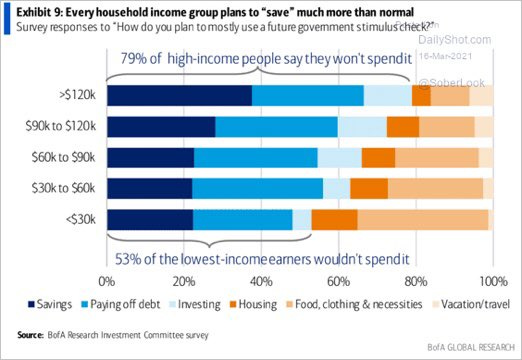

So let’s take a closer look at how they will spend some of it. Now remember, the $1,400 stimulus payments are garnering the most attention because of their directness, but really it’s only ~20% of the total $1.9T bill. Last week we cited a Deutsche Bank survey which indicated that many will invest the stimulus payments in the stock market. Fair enough, YOLO, but what about other surveys? Bank of America comes out with a slightly different one.

Let’s leave aside whether some of the respondents were financially virtue signaling and take the survey at face value. If so, a disproportionately high number of those surveyed said they will save or retire debt with their EIPs. As for the spending, most will spend the stimulus payments on food, clothing, necessities, no surprise. As we move up the income ladder, so too does the percentage of payments allocated to “vacations/travel,” which again intuitively makes sense.

Ultimately though, we believe what’s dark blue and blue (i.e., savings and paying off debt) will eventually translate to “spend.” Why? Because despite our current historically high savings rate, much of it was caused by one-time government transfer payments and our quarantined lifestyle. As the months tick by, we’ve subsequently spent them down. So eventually we will unleash the savings. What’s interesting is that we’ve yet to materially do so. Notice that even at year-end when the CARES Act impacts have largely faded, our savings rate was still 2x the norm? That’s alot of dry powder. By January, our savings rate exceeded 3x our norm (as the second EIP $400 checks landed), and it will take another step higher in March/April when ARPA payments add to the difference.

In addition to the elevated savings rate, we’ve also reduced our credit card debt, likely our costliest debt with the shortest of maturities.

While we’ve shown the two charts above before, the notion that the stimulus checks from the recently passed ARPA will “juice” the economic recovery is incomplete. We’re saying that we’ll not only spend the stimulus we’re about to receive, but also spend-down our savings and spare credit card capacity. We can think of this as “the great unwind.” While ARPA will provide an economic boost, the great unwind of the latter will be the afterburners.

Our original bet on human nature (i.e., that incentives will drive us to find a vaccine/cure for COVID quickly and allow us to recover faster than most believe) continues. What we’re betting on now is that as our social behaviors revert to pre-COVID patterns, so too will our financial behaviors. Collectively, we’re about to lever-up as we go back to our old habits of saving little and spending beyond our means. This should happen faster as YOLO + monkey see/monkey do grips the globe. We’ll all want the same items, connections and shared experiences Instagrammed daily by our friends and family as the world reopens. We’ll all want an Eva Longoria life.

This of course isn’t lost on Wall Street, as almost all of the major firms have piled into the reflation trade to some extent. Evercore ISI has appropriately called for investors to “buy all the lines,” something we agree with.

We’re saying the volume and intensity of that spend is, however, still under appreciated. As we recover, we’re heading into a Goldilocks period of:

Historically low interest rates (despite what you’re seeing happen to the 10 year Treasury),

Accommodative monetary policy,

Loose fiscal policy,

High pent-up demand,

Historically high savings rate,

Lower credit card debt, and

Sun & Fun.

We’ve seldom had an instance where everyone gets to participate in a recovering economy. It’s typically an uneven one, whereby those with more have ended up with MOAR post-crises.

Lower rates, increased stimulus, quantitative easing, etc. have all historically benefited the rich, but this time it’s different because it is different. This time our political handstand and the rise of populism has led to relief packages that have turned the world “upside down” and prioritized those lower on the economic totem pole.

Swift the Backlash Will Be . . . Swift it Was

All of this can be directly traced to the political discord stemming from the 2008 Great Financial Crisis (“GFC”), which then led to the populist movement. During the GFC, we elected to save banks from insolvency, but not people. As Yoda would say, swift the backlash will be, and eventually that movement did come to affect both conservatives and liberals. Conservatives simply won control first with Trump’s election, but now the liberals get their turn at the piñata. Although the Urban-Brookings Institute’s chart above compared the ARPA package to the TCJA passed in 2017, what’s more interesting if you compare ARPA to the first COVID bill in 2020, the $2T CARES Act, which created not only the EIPs (i.e., stimulus checks), but also the PPP (Paycheck Protection Program) and the EIDL (Economic Injury Disaster Loan), all of which again focused on the individual directly or indirectly. Recall that the CARES Act was passed with Republicans in control of the White House and Congress. So ARPA at $1.9T? Same song, different singer.

Said another way, we’re agnostic about which party is in control when it comes to spending. The political message from the electorate has been clear . . . Show Me the MONEY! Congress and the White House have dutifully obliged and showered funds on companies and voters to preserve jobs, protect livelihoods, and bolster individual finances. So regardless of who is in control (Trump/Republicans or Biden/Democrats), the fiscal largesse has been the same. We the People . . . Get the Money.

Now that they have it? Now they will spend it. ALL OF IT. No, not just ARPA, but our spare savings and credit capacity. Assuming otherwise means assuming that Americans have fundamentally altered their financial habits in a year. We think that’s too great of a logical leap, and we think it’s unwise to think otherwise.

What this means is that consumption for goods and services will now go through the roof. Per Goldman Sachs, GPD +7% in 2021, +5% in 2022, then what? Spending can lead to growth, but lasting growth means the spending has to be on productive things. Unfortunately, most of this spend (CARES, HEROES, ARPA, etc.) was income replacement (again directed by populism), so the long-lasting productivity benefits will likely be minimal in the hands of individuals. Assumed GDP growth for 2023? 2%. Reversion to the mean.

What we worry about is what happens when all of it stops. Once our savings run dry and our personal credit cards tap out, where do we go then? We’ve written about inflation and their ill effects on interest rates, and eventually this is likely what will make our debt burdens unsustainable. Admittedly, despite recents moves in Treasury prices and interest rates, we’re still a long way from normalizing, so until then keep spending.

At some point though, the world will be awash in debt, on both the government’s and individual’s account. At some point, how do we not come full circle? The GFC was a solvency crisis, but while the monetary/fiscal policies prevented a depression, it inflamed populism. In turn, populism led us to solve our COVID liquidity crisis with monetary/fiscal policies that now heightens system risk. As debts build further, what of the next crisis? Doesn’t a solvency crisis seem to be in the cards? Isn’t that why our central bankers are scrambling to project confidence as they attempt to tame interest rates, while ignoring rising inflation best they can?

Maybe though we’re being premature. Let’s first get through the Goldilocks period of the next few months. Let’s worry about what happens after the recovery . . . after we recover. Still, we can’t help ourselves, it’s probably all that blood rushing to our head as we’re still in Sirsasana. The popular idea is that we keep printing and spending, and spending and printing. The popular idea is that it’s the little people’s turn to “get ours” while the “getting is good.” Maybe, but that feels a little unbalanced, it doesn’t seem . . . stable. Doesn’t overabundance undermine value while scarcity underpins it? Maybe I have been looking at it all wrong. It’s apparently the opposite. Oh well, I guess the world may be upside down, but so am I.