Yeah . . . there is no Recession.

February 26, 2023

I just stepped off a Disney cruise.

Okay really I just survived one. This guy.

In your face, 24/7. Even in all his glory it’s alot to behold. Then there’s the hidden Mickeys.

Planted all over the ship and imprinting themselves subconsciously in your mind. Well, more like the minds of your impressionable young children, who will one day replicate this experience for their children with their inflation adjusted dollars.

We went with 17 families, a smorgasbord of kids, adults, grandparents, you name it. +100 people in tow and took up almost an entire deck. Spent a whole week laughing, swimming, joking, frolicking, eating like it’s going out of style and just having fun. After experiencing that, I can say unequivocally two things.

First . . . do it. Travel. Travel with friends. Travel with interesting and fun people that can make you laugh out loud even when it’s 2am at night after a week of long nights. Travel with people who will spark joy in your life. Travel so you can see your kids laugh and smile as they take over a ship, and then an island. Just travel and truly enjoy yourself.

Second?

There is no recession. Let’s ponder that for a bit.

As I sat in the ship’s lobby, waiting with monk-like patience to download the latest inflation data (PCE), and enjoying that bit of quiet solitude before the ship awakens to the sounds of stampeding feet, it dawned on me that I didn’t even need the data. I just needed to look around.

There is no recession.

Certainly those who sail on a Disney cruise are a self-selecting group, a skewed demographic. Typically more affluent. Families with children ages 4-11 with grandparents in tow. Many are professionals or self-employed business owners who are thriving in this economy. Makes sense given the price point for the trips. Many also didn’t bat an eyelash at $15 adult drinks and $40 stuffed animals. $10 bucket of popcorn? Give me two . . . but the refills are $1? . . . “two” the man said again.

There is no recession.

What do you do? How do you do it? How’s it going? Three questions. I’d keep asking them, and keep getting pretty positive answers. Yes, things are getting more expensive, but everything’s pretty good.

There is no recession.

So as the news trickled in, coming in bursts as waking children started hogging the bandwidth, a picture emerged.

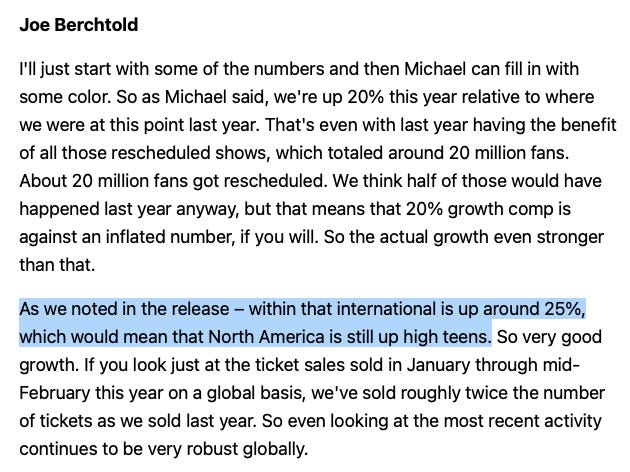

The broad brush-stroke was painted by . . . Live Nation. For those who don’t know, Live Nation is a tickets broker. Want to experience the grandeur of a Taylor Swift, Beyoncé, BTS, or U2 concert? Live Nation will sell you one. Here’s a response to a question from Stephen Laszczyk of Goldman Sachs wondering about the 20% YOY global growth in ticket sales this year.

Live Nation’s CFO fields the response first, followed by its CEO.

What’s interesting about the above is that this is a global phenomenon. If you wanted a more “discretionary” type of indicator, it’s hard to wave off Live Nation’s flashing red light. Concert ticket sales are nothing if not discretionary, and global demand ex-US is running 25% higher.

The US is coming up at a “slow-pokey” 15% (and yes that’s sarcasm), but remember, that’s a YOY +15% vs. last year’s “boom time” recovery. Really this shouldn’t come as a surprise. It’s what we’ve been saying, but also what the data’s been showing. Spending on services continue to rise, while spending on goods moderate.

We’re steadily and surely beginning to spend our way back to historical levels, but we’re not there yet. Nevertheless, just think about this chart we showed last week.

Still about $1T of excess savings, an amount that’s largely in the hands of a higher income group, whose appetite for services is ramping. Services, mind you, is people. To AI and ChatGpt’s chagrin, you need people to provide services, and people means higher wages in an environment where job openings outnumber the unemployed by 2 to 1.

Almost every category has been flat to higher in terms of job openings, so the work is out there, it’s just the labor pool that’s not.

So although average hourly wages have been declining in YOY % terms, we believe they’ll begin to climb again as we shift our consumer dry powder to that thing we crave . . . experiences . . . which means labor intensive services.

Said another way, wage inflation may get increasingly sticky as we go through this year and redeploy our $1T in savings. What’s even scarier? That’s just looking at US consumer demand here. Can you imagine if tourism actually begins to pick up globally and foreigners start to travel? It’s not unlike what we wrote in this article all the way back in December of 2020. Zombies? They’re coming.

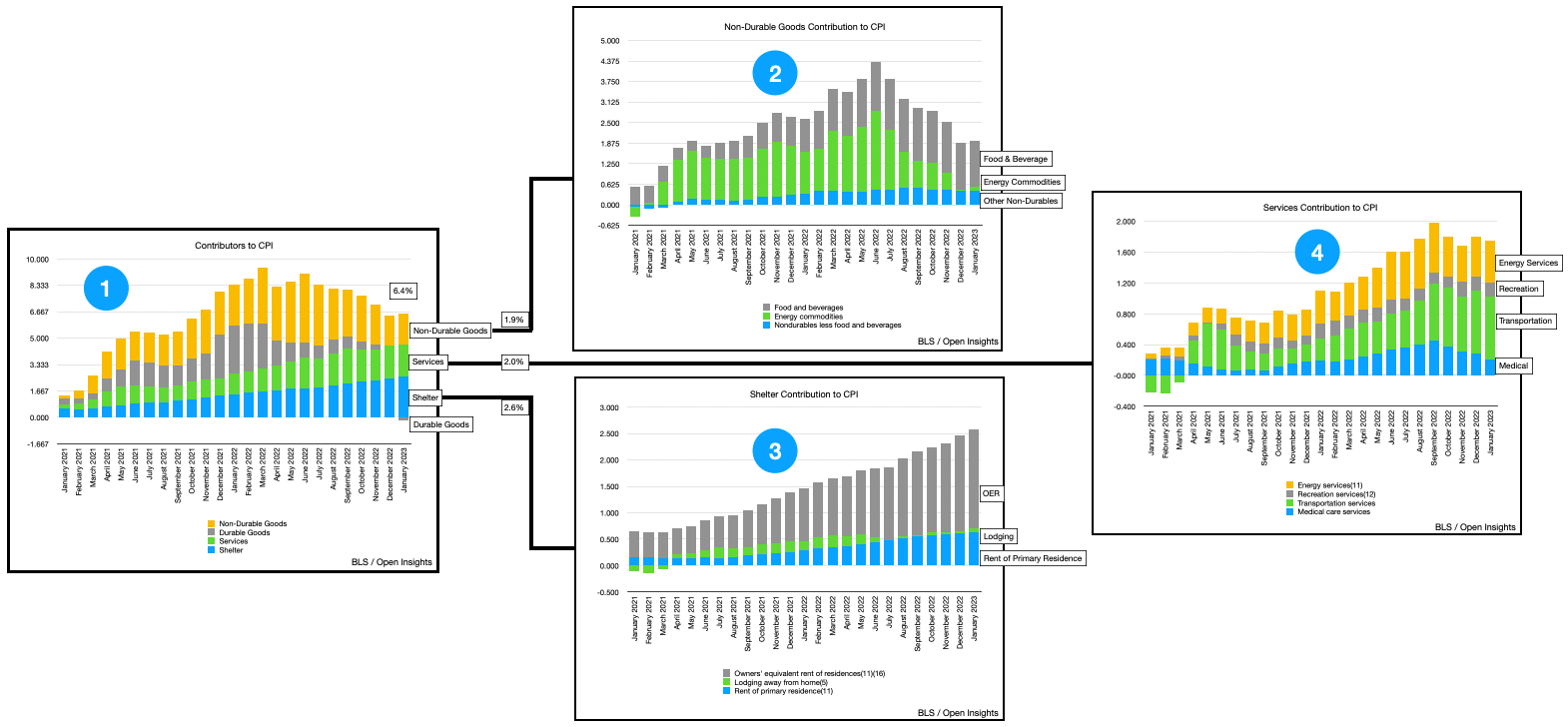

So overall we think this could portend a wage inflation spiral, which could eventually push up inflationary pressures in Services (#4) and Shelter (#3), which account for over a third of the CPI/inflation index (#1).

It’s early day though because this is still late-February. For the coming months we do see wage and shelter pressures easing off (because remember CPI is a lagging calc), and there has been weakening in those two categories in the past few months. However, if they do reaccelerate, regain momentum as we loosen our wallets, then when the CPI calcs begin picking up the real-world reacceleration sometime in H2 2023, you could see inflation also step higher. Perhaps even coinciding with energy prices, which we still think legs higher as we move through the year.

Like the ocean though, these are just the ebbs and flows of the data. The underlying economic momentum here is pretty strong, so despite the volatility in the markets, our cruise ship may just keep plowing ahead. As we get deeper into the year, however, the data likely turns, and inflationary pressures ramping higher coinciding with lower lower savings/higher debt levels, wouldn’t be great for risk assets. What we described above could be just a pathway for how that happens. Still though, it’s early, so we’ll need to sit with more monk-like patience and ponder the incoming data as it plays out.

For now, we’ll enjoy the remaining hours of this mini-vacation, and sit quietly and contentedly with the Mouse.

Repeat after me . . . there is no recession.

Please hit the “like” button and subscribe below if you enjoyed reading the article, thank you.

...... yet

Remarkable!