Welcome to Iran's Hurt Locker

March 13, 2026

We need an offramp.

We’re trying to desperately find one, but the consequences are all unpalatable. Declare victory and walk away? Strengthen the enemy long-term. Give up? Never. Deploy the full power and might of the US armed forces? Embrace the tar baby. There are no good choices right now.

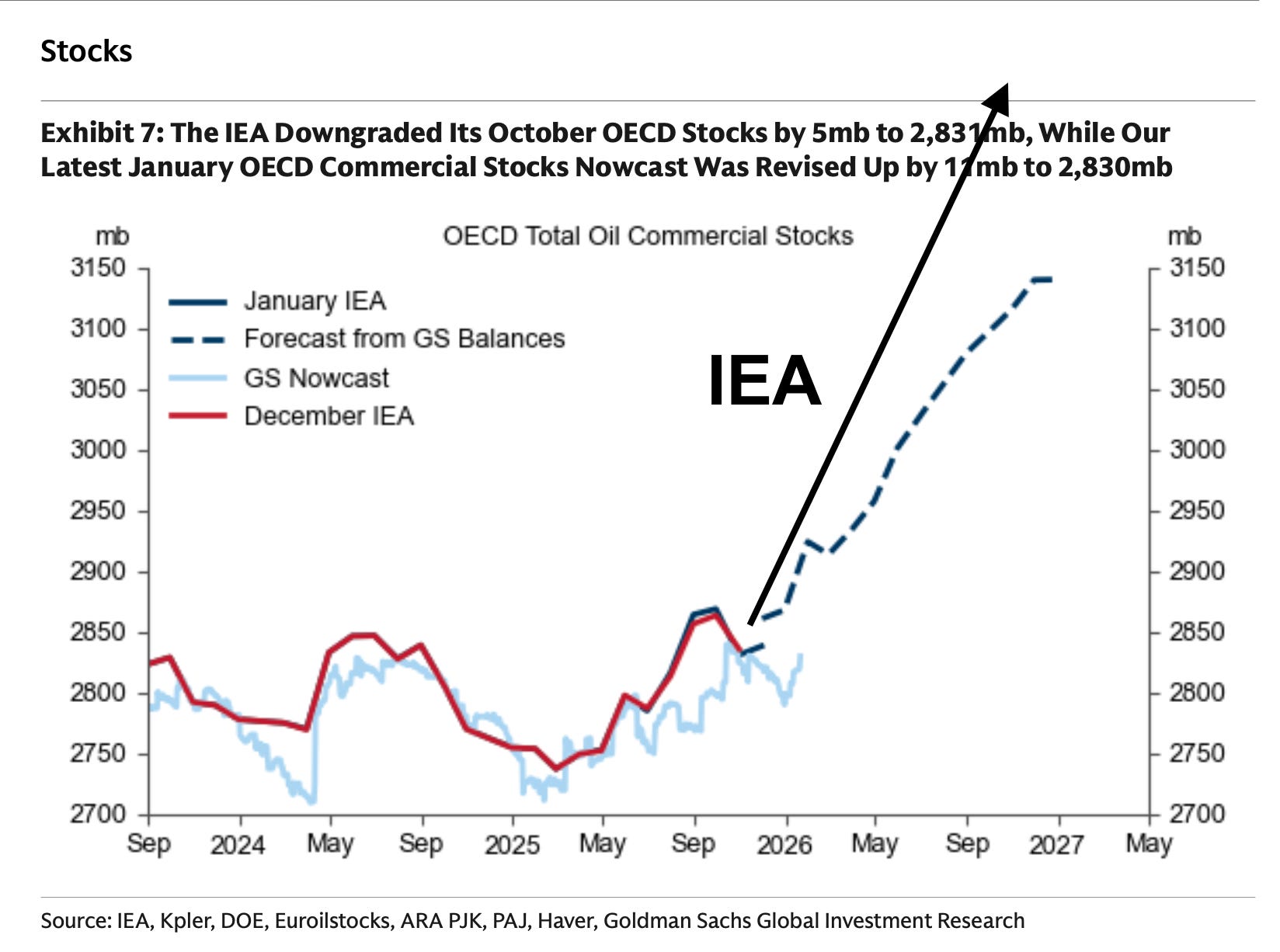

This was one of the worst strategic blunders, made on the basis of hubris, supported by faulty information. For months, the investment community and government agencies were peddling analyses that we were witnessing one of the greatest global glut in oil ever. JP Morgan, Goldman Sachs, the IEA.

Nearly everyone.

The IEA anticipated a 2.3M bpd build in 2026. Goldman came in below that at 0.8M bpd.

This narrative was so pervasive it stuck. So armed with wrong assumptions, and fresh off the back of a successful Venezuelan regime change, Gaza takeover, Hezbollah decapitation, and global economic arm-twisting, we ventured forth to pursue regime change in Iran. Quick and easy right? This my friends is the very definition of FAFO.

So here we are today, one where oil prices are ticking higher as the war, err excursion, no wait excursion to prevent a war plays out. Whatever this was/is, it’s a bad trip. The US can and has easily achieved some tactical victories, but strategery-wise? Not so much.

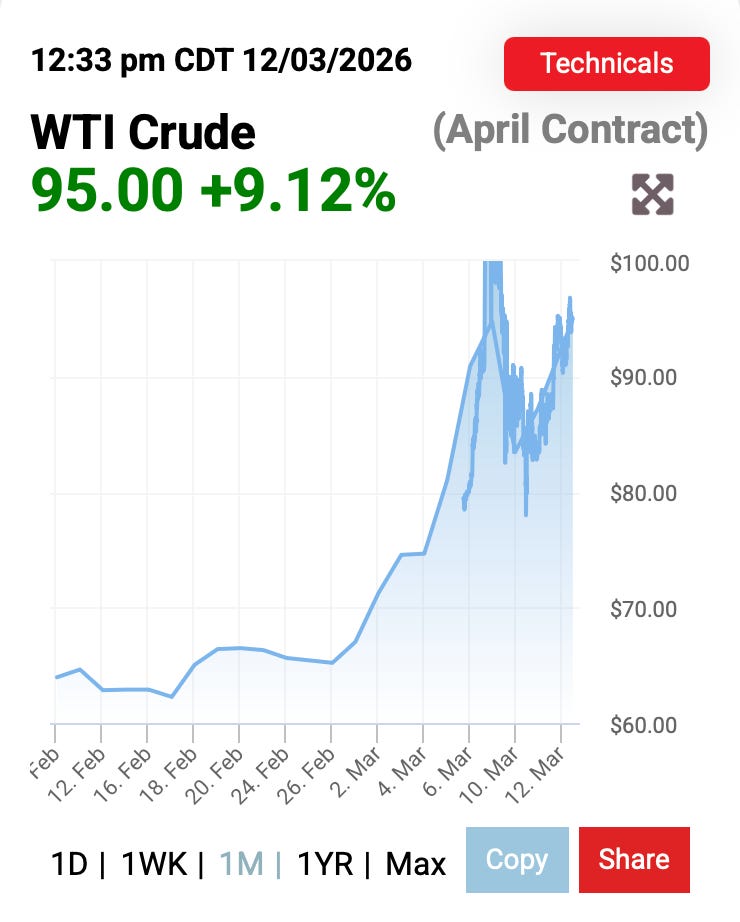

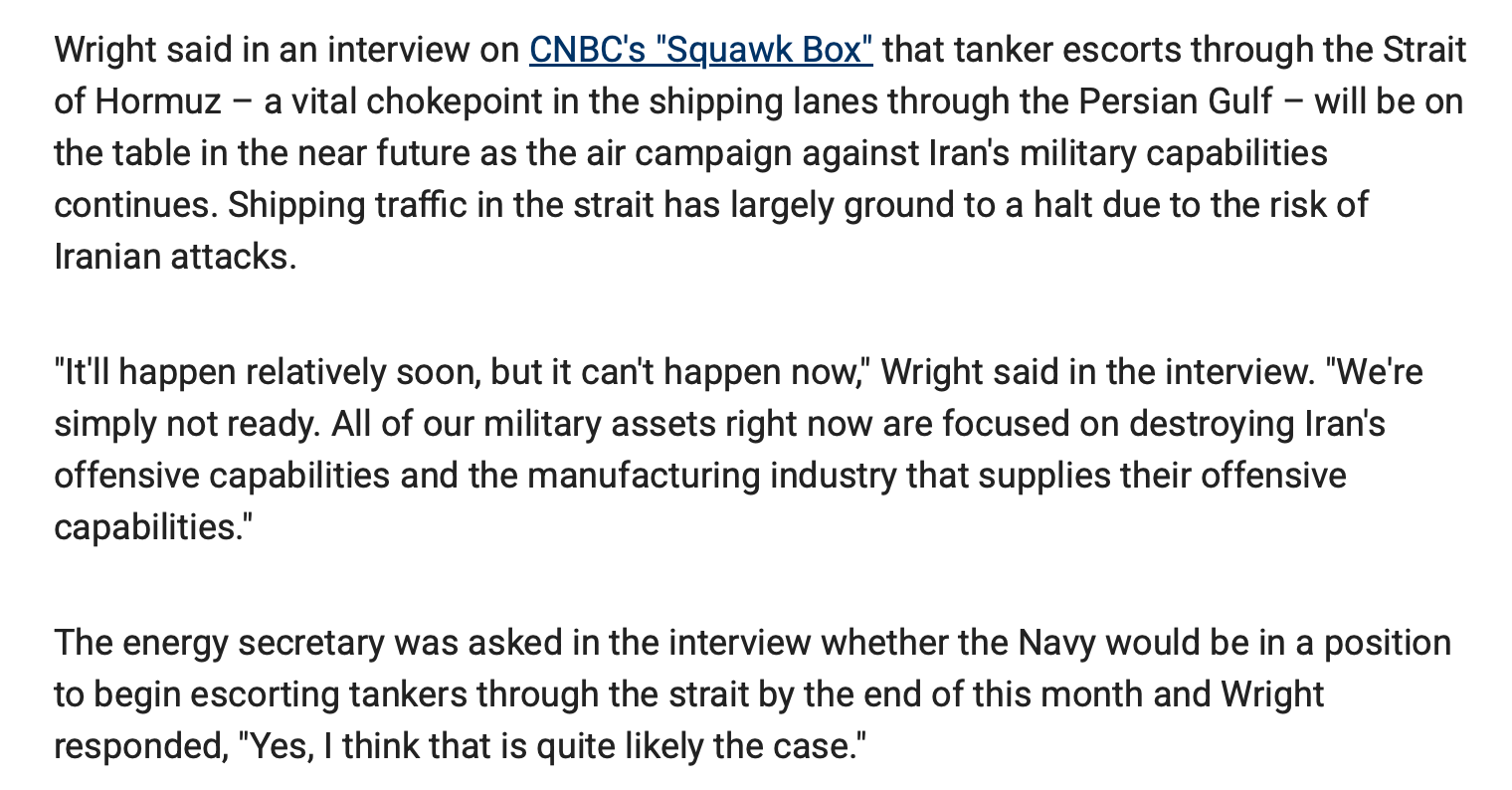

Since we last wrote, oil prices have climbed from $85/barrel to $120/barrel, only to have fallen back to the current $95/barrel level after President Trump shared that this will be a “short” war, and that Iran’s military capabilities are being materially degraded.

Fair enough, the market immediately sent oil plummeting to $80/barrel. In addition, the IEA in coordination with various countries decided to release 400M barrels of oil from their strategic petroleum reserves (“SPR”). In the US’ case, 173M barrels, to be available next week (for refiners to bid), and to be delivered over 200 days. Since SPRs in every country can’t deliver more than 3M bpd combined, we’re not sure how that fully offsets the nearly 15M bpd currently lost.

Even as these salves were prescribed to ease the market’s discomfort, Iran began mining the Strait of Hormuz and attacking ships anchored in the Persian Gulf or attempting to run the blockade. The escalation quickly eroded the market’s confidence that all is well, and that all of this will be completed in short order. Accordingly, oil prices have risen again.

Financial Impacts

The broader market though, has largely shrugged off this whole episode. For the most part, it’s flat. Sure there’s significant volatility, but here’s the performance of the indices since the beginning of the our excursion on February 28 to March 13:

S&P 500 -2.5%

Nasdaq -1.1%

Russell 2000 -4.8%

Other than the Russell 2000, the broader market has largely shrugged off these attacks despite the disruption to oil, petrochemicals, fertilizer, noble gases (e.g., helium in semiconductor industry), etc. Arguably, the US is better positioned to weather the energy supply shortfalls, but with its just-in-time supply chain, eventually the inflationary costs will rebound as manufacturers worldwide struggle with shortages and higher energy prices. The supply chain can hold-out for a brief pause, but as the days roll-on the damage gets increasingly exponential and calcified.

We think the market’s overly complacent here. The buoyant stock indices mean the market is predicting a rosier future, one where energy prices might come out of this whole debacle actually lower.

Is that possible? Maybe. Maybe if the US cowls Iran . . . but man-o-man, that sure seems doubtful right now.

What we do know is that each day the market fails to fall, it further grants Trump carte blanche to continue his attacks unabated. In turn, the longer the attacks continue, the greater the harm done to oil supplies and oil prices in the future.

That’s the calculus. It’s the US vs. Iran vs. the stock market/global economy. Who will capitulate first?

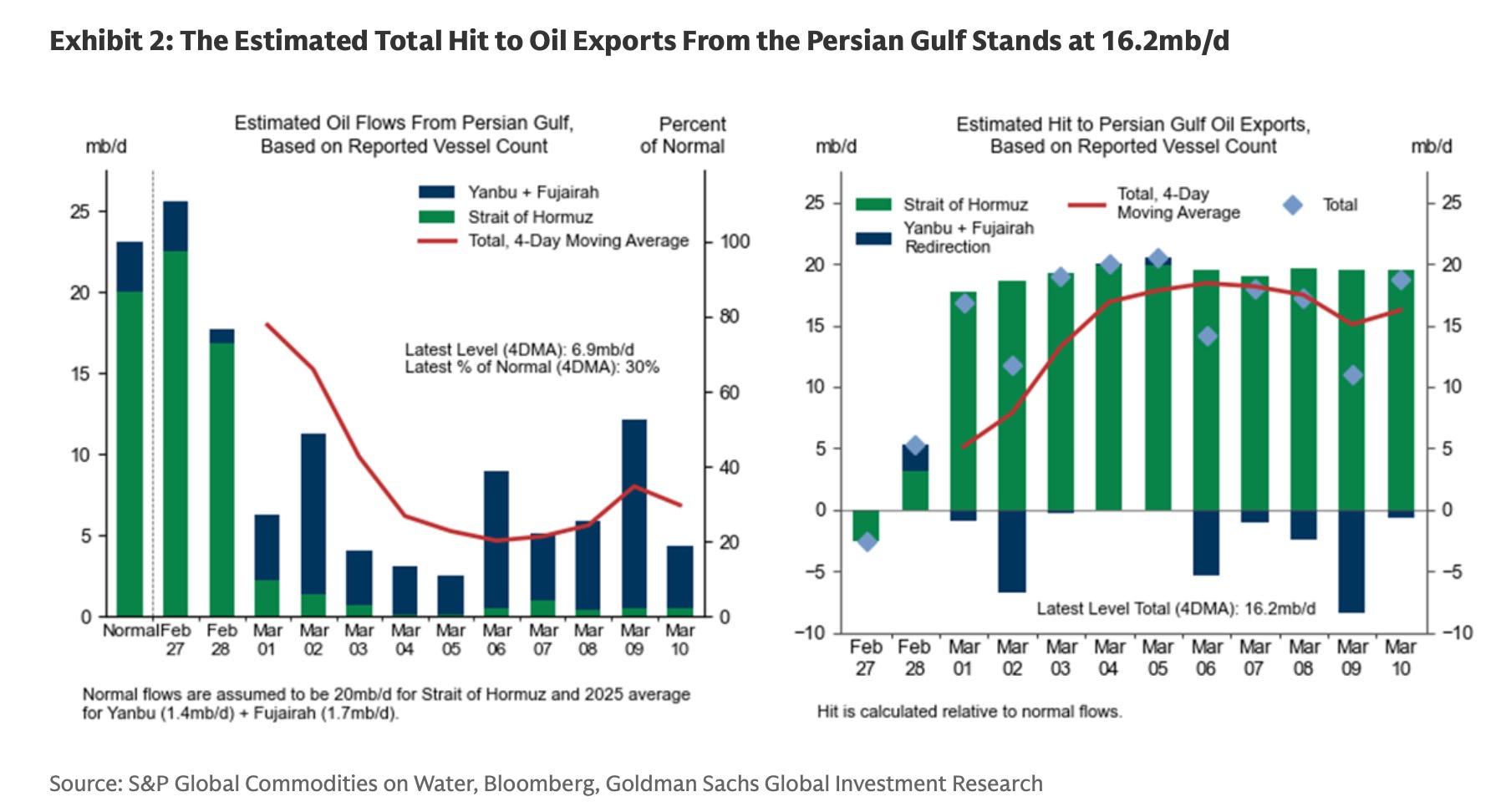

So let’s level-set again. Oil exports out of the Strait of Hormuz runs about 20M bpd. ~150 vessels of all types (i.e., petroleum, container, agriculture, etc.) traverse this 22 mile channel. It’s shallow, so the crossing corridor is only about 3-4 miles. Surrounded by mountains, Iran has numerous places to launch drones both in the air (UAVs) and water (USVs) to disrupt the flow of traffic. Tack on mines too (buoyant, rising, CAPTOR (torpedo launching)), all deployed from fishing trawlers, or dhows (junk trading vessels). There’s thousands of those, so deconflicting the area will be difficult.

Plus, it only takes one hit to ratchet up the economic costs. One drone getting through, or one mine causing damage means the whole market gets repriced. Even a minor disruption can be material. If 150 vessels a day transited the SoH, what happens when only 130 do? Isn’t 20 still a material disruption?

From purely an oil perspective, let’s do some math on what’s actually happening. 20M bpd of oil flows through the straight. A few hundred thousand to about a million barrels are still flowing as Iranian exports to China continue. The Saudis have also reversed a pipeline that runs East/West and can potentially redirect 5-7M bpd there, so the disruption is around 14-16M bpd.

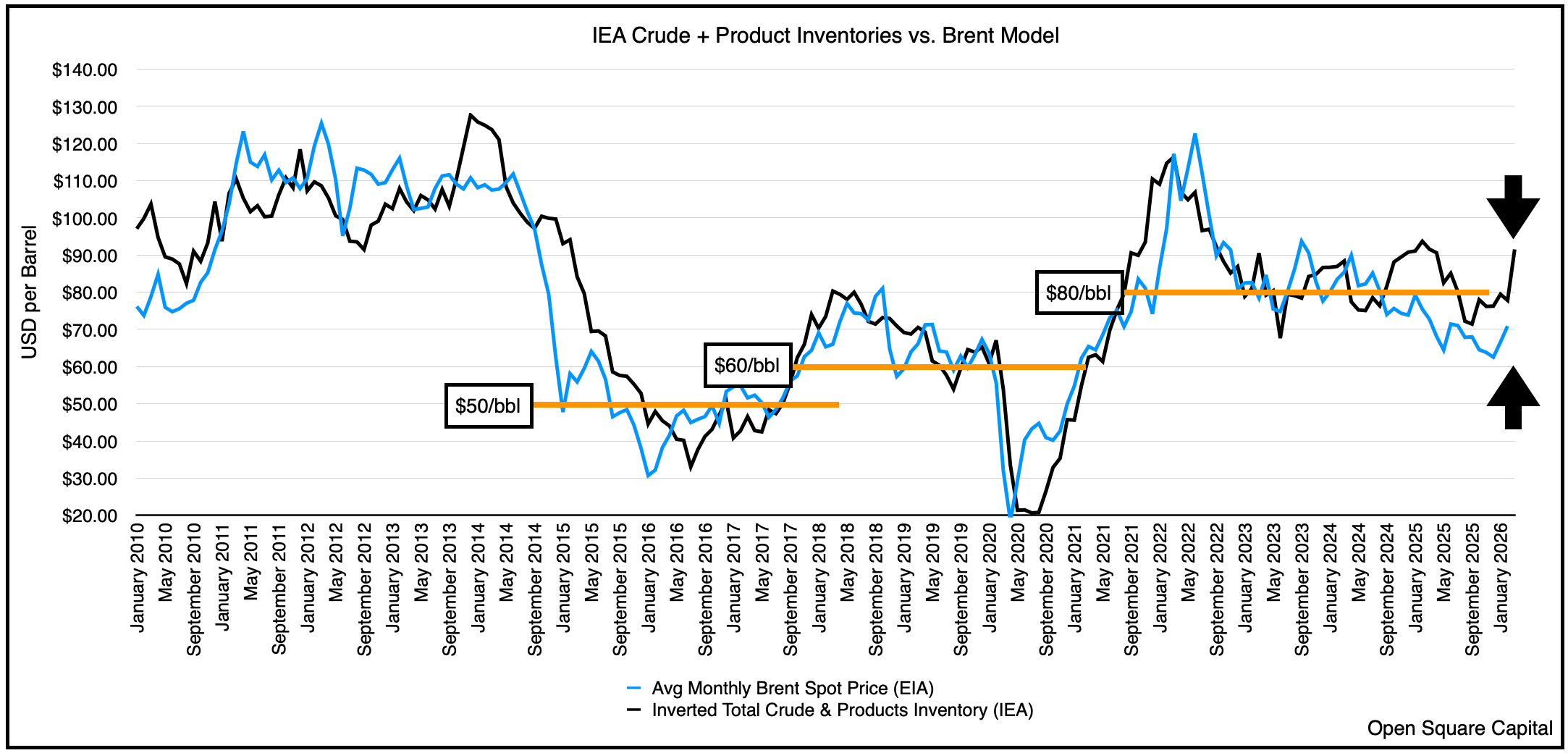

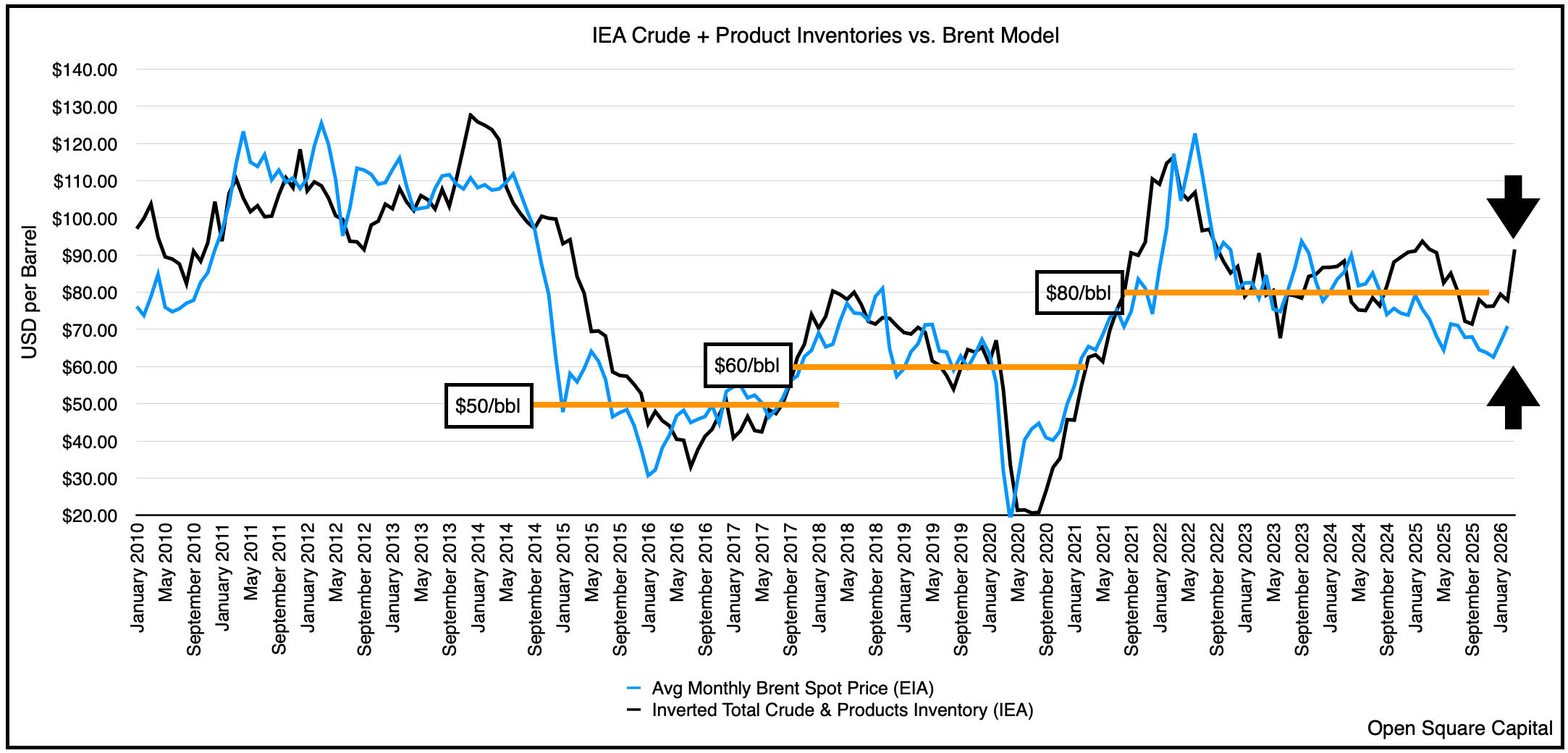

The oil isn’t entirely lost though because if the artery is plugged, producers can shunt it to storage for a limited time before they have to shut-in their fields. Unfortunately, the IEA reports that ~10M bpd of production is currently shut-in as storage tanks are getting closer to full capacity. Note that this is the most important figure because it’s the real production that’s lost. So take that 10M bpd and multiply it by the number of days, and you’ll start to see some large numbers. 100M barrels in 10 days alone, 200M in 20 days, and that’s not even factoring in the delays if/when the US and its allies can reopen the strait and how long it takes the ships to get refueled, repositioned, and sailing again. Ripple that through to inventory balances, and assuming 1/3 of that impact shows up in IEAs inventory figures, and you suddenly get a base-line of $90/bbl (i.e., the price oil should fall back to once all is said and done).

It’s the difference between a hiccup in your supply chain vs. a real supply shock. Stock-outs are what we’re worried about, and life is coming at us fast.

Prolonging the stock-out though is effectively Iran’s strategy. It’s two-fold right now,

Deterrence - make this endeavor so costly that strategically, the US, Israel and any other ally will be deterred from attacking Iran again;

Resilience - no matter what you do, this regime will survive. More importantly it can survive longer than the stock market and global economy can hold-out on such a large supply disruption.

Unfortunately for Trump and investors betting on a TACO (i.e., Trump Always Chickens Out), the timeline this time isn’t entirely in his control. For the most part, the clock is ticking, but that clock isn’t controlled by the West. The longer this lasts, the higher the economic pain, and it behooves Iran to keep testing that pain threshold. Closing the SoH, or even threatening to close it, gives them the ultimate leverage in any negotiation. Attacking oil infrastructure through the Middle East also encourages the Saudis, Kuwait, Qatar and the UAE to call on the US to bring about a ceasefire/truce on terms favorable to Iran.

Oh wait, they know that.

So for Iran, each missile launched, each drone sent, is an invitation to their hurt locker. Spread the pain and really test everyone’s resolve. The desire to exact revenge and retribution will also drive Iran’s thinking. While it has been weakened, and not immaterially, it knows that this battle is existential, and if they’re playing the trump card of closing the SoH, it better be for a larger pot.

Kinetic Affects

As the US and its allies are still marshaling naval and ground forces in the region, it will take another few weeks before a proper military escort can begin to break the blockade. In fact, likely month-end.

Tack on the repositioning of combat troops and we’re looking at least another few weeks.

Our rule of thumb is that oil prices will rise $1/bbl, conservatively, every day this excursion continues if we assume 10M bpd of shut-ins (i.e., real production lost). What we mean by that is every day the SoH is closed, equates to about $1/bbl of premium when we “return to normal.” If everything gets sorted by month end, we think this is what inventories and oil prices will look like.

Any longer than that, and we’re rebasing higher. Two caveats: first, there’s bound to be some demand destruction as oil prices climb, airfares getting expensive and road trips not taken, but the world can likely keep calm and carry on for a few weeks (so we’ve disregarded that for purposes of this exercise). Second, you’ll notice that in the chart oil prices have previously dislocated from inventories since mid-2024. That’s largely because of the calls for “inventory gluts,” etc., so tack on whatever discount to the $90/bbl fair value you think is appropriate (i.e., the discount that you think will “survive” even after this debacle). Suffice it to say if oil stuck around in the $80s after kumbaya breaks out, oil companies will print money (they need to if the world wants producers to increase production).

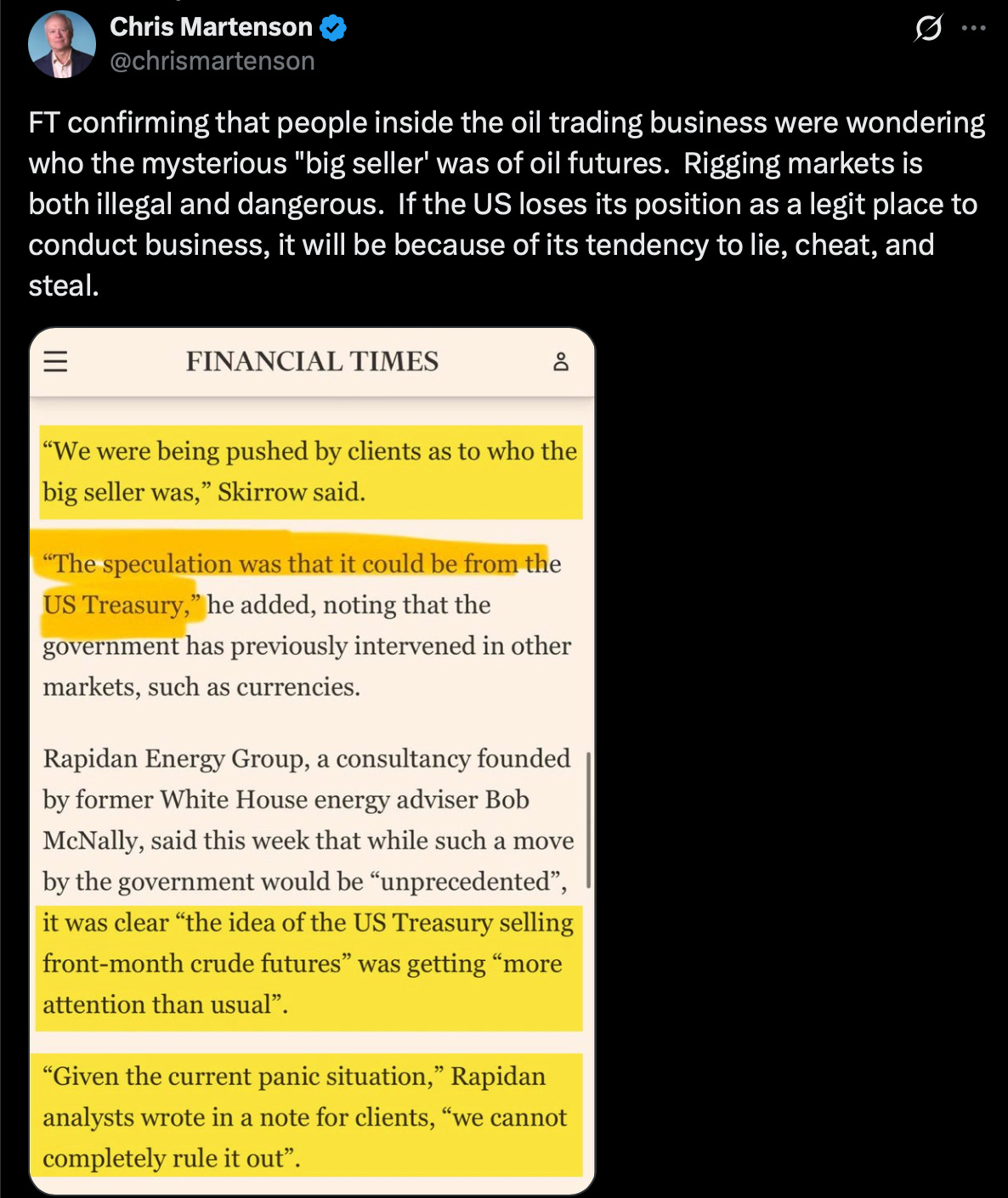

We don’t know when this will all end, it could end suddenly and oil can plummet, but what we do know is that the US is beginning to manipulate oil prices . . .

. . . and trying desperately to find a palatable political narrative . . .

All of these shifting statements and market manipulations will prevent real price discovery. It’ll deter producers from drilling and pumping more because of the potential volatility. Furthermore, it prevents the market from responding to the real shortage, and shifting enough capital to address the issue, which will inevitably exacerbate the issue.

Ultimately, selling financial paper and lowering prices via press statements can suppress oil prices for a bit, but the physical always disciplines, and the Iranians know that.

Again, this is a race against the clock, but the Iranian’s are holding the watch. The longer this lasts, the higher oil climbs.

Welcome to the hurt locker.